From Citi:

In the past two weeks, the US and China announced an agreement signaling stronger action to curb greenhouse gas (GHG) emissions. The International Energy Agency (IEA) issued its annual update, World Energy Outlook 2014 (WEO-2014).

China released its Energy Development Plan 2014-2020.

We consider the implications of these developments for investors in fossil fuels. Caution for coal and oil, optimism for gas – Citi’s commodities team assessed the impact of the US-China announcement, concluding that lower demand from 2015 to 2030 could be valued at ~US$1.3 trillion for oil and as much as ~US$1.6 trillion for coal. In contrast, the likely rise in gas demand could be worth ~US$1.3 trillion, compared with commonly used baseline assumptions. The key baseline used was the WEO-2013 Current Policies Scenario. See section on Commodities Research and “The New Climate Order – The US-China Breakthrough Accelerates an Altered Future For Oil, Gas and Coal”, by Anthony Yuen et al.WEO-2014 focused on a central New Policies Scenario, which is consistent with a global warming forecast of 3.6°C. The IEA plans to publish a new report in mid- 2015 ahead of the end-2015 climate change talks in Paris, which will focus more heavily on a scenario consistent with stabilizing warming at 2°C – its “450 Scenario”.

China’s Energy Plan suggests a focus on constraining coal use. Citi analysts expect new power stations to be built in northern and western China, close to domestic coal mines, suggesting that local rather than imported coal would supply them. See section on China’s Energy Development Plan 2014-2020, and Citi report by Pierre Lau “China Clean Energy Sector – Winners of PRC Energy Development Plan (2014-20)”.

Thermal Coal – expectations may ratchet gradually downwards

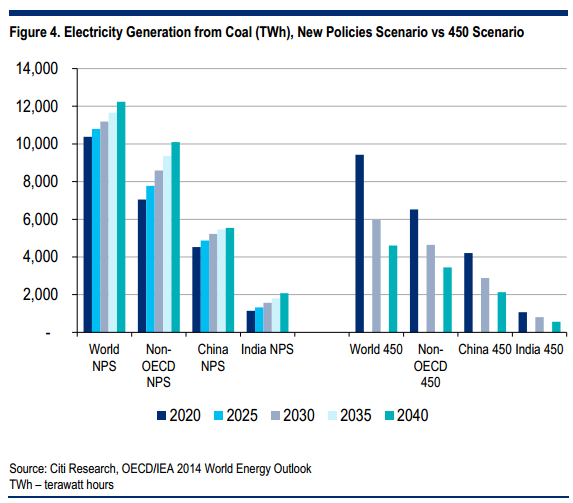

We suspect the world will move, albeit gradually, directionally towards 2°C, implying ongoing downgrades to the global thermal coal outlook. In WEO-2014, the New Policies Scenario projection for 2035 for global electricity generation from coal was downgraded by 5% compared with WEO-2013. This included downgrades of 2% for non-OECD, 1% for China and 5% for India.

In WEO-2014’s 450 Scenario the outlook for coal rapidly deteriorates (Figure 1 and Figure 4), suggesting that modest changes to climate policy could mean large impacts on thermal coal.

We suspect that central estimates are more likely to be revised downwards than upwards for thermal coal in the next WEO report.

We are skeptical about the prospect of a large scale carbon capture and storage industry, an initiative oft cited as the path to securing coal’s future in the energy mix, as discussed in our section titled Carbon Capture and Storage?.

Many coal industry players cite coal as being critical to alleviation of energy poverty in regions including sub-Saharan Africa. However, in WEO-2014’s special focus on Africa, coal appears projected to play a minor role compared with hydro, gas, renewables and mini-grid / off-grid systems. To us, it looks almost like an “everything but coal” scenario.Gas / LNG – likely benefits from fuel switching

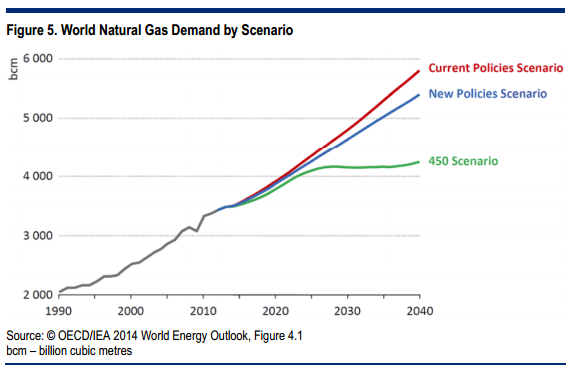

Views on the outlook for gas / LNG are more mixed. Citi’s commodities team’s projections (Figure 16) show gas benefiting from fuel switching, particularly in China, if stronger GHG measures are implemented. The IEA’s projections show gas demand rising over time in all scenarios (Figure 5), with Australia’s LNG projected to rise by 270% in the central scenario (Figure 6). However, the IEA’s gas forecasts show successively slower growth under each tougher climate change scenario.

That does not marvelous for gas, either.