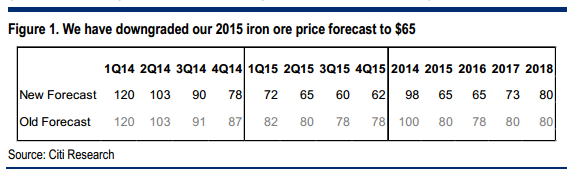

And here it is in all of its glory, the Citi iron ore smash:

We expect iron ore prices to fall into the $50s – We have downgraded our price forecasts and now expect prices to average $74 in Q1, moving down to an average of $60 in 3Q15 – briefly dipping into the $50s – with annual averages of $65 in 2015 and 2016.

The recent selloff has been driven by weak demand and deleveraging – While the first half of the year saw prices driven lower as supply increased, Q3’s selloff was driven by deteriorating demand and deleveraging of traders and Chinese mills, with prices now selling off on APEC and pollution driven steel production curtailments. We expect renewed supply growth to once again drive the market lower in 2015, combined with further demand weakness.

$60s needed for significant ex-China curtailments – We examine production profiles and sensitivity to iron ore price declines in each country or region where exports topped 10 Mt in 2013. We find only modest cutbacks are likely if iron ore remains in the $70s, with sustained prices in the $60s needed to prompt significant cutbacks. Sustained prices around $60 do appear to offer much stronger cost support, though this is dependent on further FX shifts and other variables.

Domestic Chinese iron ore production resilient, but will need to fall further – The resilience of Chinese iron ore production has been often underestimated. This year, while producers reacted to price declines of the first half, they have yet to materially react to the selloff that occurred in Q3. We expect many mines that shut over the winter to simply not restart, but the scope of such cuts is likely to be insufficient. As a result, prices will need to fall further to prompt additional closures.

Chinese steel demand is likely to weaken in 1Q15 – While APEC and pollution related measures are currently negatively impacting demand, fundamental demand trends have been slightly better in Q4. However, we expect a further deterioration in steel demand in Q1 on the back of extremely tight credit conditions in 2Q14 (typically there is a six month lag to steel demand), slowing of manufacturing export growth, and the government prioritizing reform over short-term growth.

I could not have put that better myself. And from the SMH blog, the downgrades are rolling as well:

Citi Group has slashed its iron ore price forecast for the next two years to $US65 a tonne, from about $US80, and has reduced the “fittest of the iron ore plays” FortescueMetals Group to a “neutral” from “buy”.

Citi has also slapped a “sell” on Pilbara juniors it considers to have become risky plays – Atlas Iron and Mount Gibson, from a “neutral” rating.

Atlas Iron’s share price target is now a measly 14¢. Just two years ago, the great white hope of the Pilbara had a market capitalisation of $1.9 billion.

…Fortescue is deemed “by far the fittest of the iron ore plays” and best placed to weather the price rout – thanks to its falling costs and the longevity of its assets but will be hit by lower cash flow and onerous debt repayments.

Citi has slapped a neutral on FMG and reduced the target price to $3.20 a share, from $4.50, and a buy. But analysts are confident the “third force” in the Pilbara will enjoy sufficient liquidity to meet “debt repayments”.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.