From East Asia Forum:

In 2008, to compete with BHP and Rio Tinto over shipping costs, the shipping company Vale commissioned, at a cost of over US$2 billion, a new line of ‘Very Large Ore Carriers’ (VLOCs), dubbed the ‘Valemax’. The Valemax carrier is the largest bulk carrier ever built: over twice as big as Cape-size carriers (400,000 dwt). Current shipping costs from Australia to China stand at around US$10/tonne, whereas it currently costs around US$22/tonne to ship iron ore from Brazil to China. Direct Valemax trips from Brazil to China would bring shipping costs down to aboutUS$15/tonne.

Vale had 24 out of 35 of these huge carriers built in China, and the rest in South Korea. China’s Export-Import Bank and the Bank of China even financed the project to the scale of US$1.3 billion, so Vale was confident that this step was in the interest of iron ore consumers in China and that these cargoes would be welcomed.

But, on 29 January 2012, the Chinese Ministry of Transport issued a notice specifying that cargo ships with a capacity greater than 350,000 dwt could not dock in Chinese ports, citing safety concerns. Interviews confirm that Vale was taken aback, alongside many Chinese iron ore industry insiders.

The blocking of the Valemax carriers was not the result of coordinated, state-led, revisionist behaviour. It was not a directive coming from the central government or the Chinese Iron ore and Steel Association, or even the large steel SOEs, all of whom favoured the Valemax since it would reduce the overall price of Brazilian iron ore. The opposition, and lobbying, came from Chinese ship owners/operators, led by COSCO (China Ocean Shipping Company), who stood to lose shipping business, and held enough sway with the Chinese Shipowners Association, the port authorities and the Transport Ministry to make this happen. It is testament to China’s weight in global markets that a unilateral move by one Chinese interest group could have such destabilising consequences. The blocking of the Valemax was the result of the fragmentation of China’s iron ore industry, and the highjacking of policy-making by a particular interest group, against broader national priorities.

Industry analysts have ventured that the only way out for Vale, as a concession to COSCO and other Chinese ship operators, would be for it to agree to a charter or sharing solution with the Chinese shipping companies, by transferring Valemax ships for Chinese shipowners to operate.

In December 2013, news of one such five-year ‘bareboat charter arrangement’ with Shandong Shipping Alliance was announced by Vale’s Jose Carlos Martin.

On 10 February 2014, the Chinese Ministry of Transport issued a notice reframing coastal berthing regulations. From 1 July 2014, oversized cargo ships have been allowed to dock in Chinese ports with a capacity not exceeding 250,000 dwt, as long as they match their load with the port’s capacity. Some analysts say this new regulation slowly opens the door to Valemax cargoes docking in China, while the China Shipowners Association reiterated its opposition to 400,000 dwt cargoes ever docking at Chinese ports.

Then on 12 September 2014, in a ground-breaking announcement, Vale revealed that it had reached a ‘framework agreement for strategic cooperation in iron ore shipping’ with COSCO. This is another step towards resolving the almost 3-year-old impasse between the two giants. Following the terms of the agreement, Vale will transfer 4 VLOCs to COSCO and charter them back from the shipping giant for the next 25 years. It also agreed to similar terms regarding 10 more VLOCs to be built by COSCO to transport iron ore from Brazil.

The new agreement between COSCO and Vale will presumably lead to the Chinese Ministry of Transport fully lifting the ban on the Valemax cargoes in the near future.

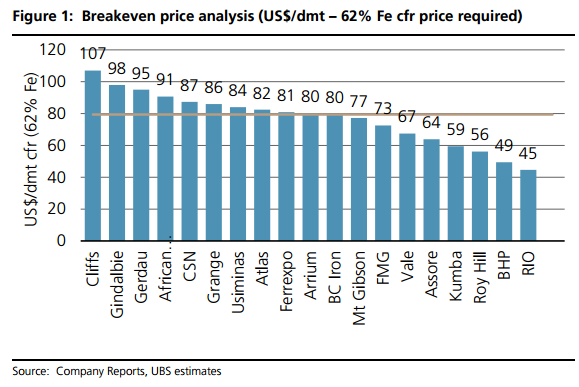

$5 per tonne is much higher than I thought. Vale just took a big leap ahead of FMG in the race down the cost curve of survival: