Just six years ago, the US and a number of European nations experienced first hand the carnage of a full scale property bust. These experiences should have taught the world that debt-fueled property speculation, along with placing regulatory constraints on housing supply, is a recipe for disaster and bound to end badly.

Yet last year, the Obama Administration looked to cement the US housing recovery by re-igniting sub-prime lending – one of the factors that caused the US housing bust (along with the Global Financial Crisis) in the first place – by getting banks to lend to a wider range of borrowers by taking advantage of taxpayer-backed programs — including those offered by the Federal Housing Administration:

Housing officials are urging the Justice Department to provide assurances to banks, which have become increasingly cautious, that they will not face legal or financial recriminations if they make loans to riskier borrowers who meet government standards but later default.

Officials are also encouraging lenders to use more subjective judgment in determining whether to offer a loan and are seeking to make it easier for people who owe more than their properties are worth to refinance at today’s low interest rates, among other steps.

Obama pledged in his State of the Union address to do more to make sure more Americans can enjoy the benefits of the housing recovery…

This week, government-backed mortgage sponsors, Fannie Mae and Freddie Mac, announced that they would once again begin buying mortgages with loan-to-value ratios of 97%, effectively allowing consumers to buy a home with as little as a 3% deposit:

…the move from a 5 percent down payment could increase the ability of creditworthy but cash-strapped consumers to become homeowners and help a faltering housing market regain its traction. Both agencies at one point had accepted 3 percent down payments.

“Through these revised guidelines, we believe that the enterprises will be able to responsibly serve a targeted segment of creditworthy borrowers with lower down payment mortgages by taking into account compensating factors,” said Mel Watt, director of the Federal Housing Finance Agency, Fannie and Freddie’s overseer…

Watt’s announcement is the latest step in the federal government’s effort to continue a housing market recovery that has stagnated lately, confounding industry watchers…

Nationally, sales fell in August, and first-time buyers accounted for less than 30 percent of homebuyers, a level they have been hovering at for more than a year.

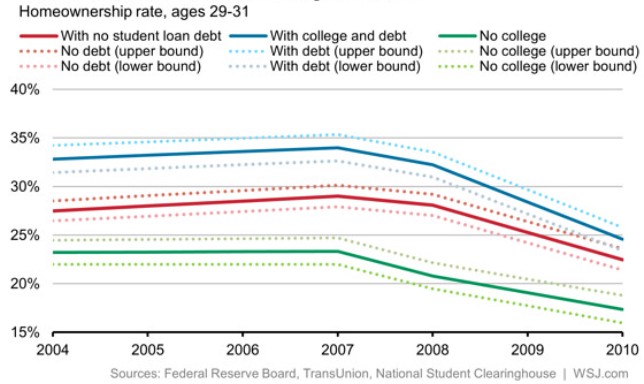

While it’s true that the bursting of the US housing bubble six years ago witnessed a massive reduction in home ownership rates, particularly amongst the traditional first-home buying demographic (see next chart).

Isn’t the definition of insanity trying the same thing (loosening credit) over an over and hoping for a different result?

unconventionaleconomist@hotmail.com