Nothing really new here expect the threatened downgrades from Moody’s:

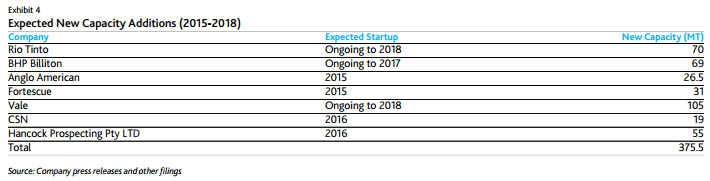

The growing oversupply in the iron ore market is damaging for the sector and poses risks to the downside. We estimate over 300 million metric tons (MT) of new and expanded production will come on-stream over the next several years. In light of expectations for muted growth in global steel production for at least into 2016, the lack of equilibrium will continue to weigh negatively on prices and operating performance of iron ore producers.

As a result, we have revised our price sensitivity for iron ore for the period through 2016 to a range of $75MT – $85MT (62% Fe). Downward rating actions for iron ore producers could result as Moody’s reassesses the impact of a protracted pricing weakness. Several key assumptions underlie the aggressive supply push by the major iron ore producers. These include a) the idea of maintaining market position given the number of projects that could be undertaken, b) that the lower costs associated with higher volumes mitigates the degree of price decline, and c) that high-cost producers will need to exit the market.

Low-cost producers such as BHP Billiton Ltd. (BHP – A1 stable), Rio Tinto (A3 stable) and Vale SA (Baa2 positive) have more tolerance to absorb some degree of lower prices in the near term than Cliffs Natural Resources Inc. (Ba1 negative), FortescueMetals Group Ltd. (Ba1 stable), and Atlas Iron Ltd. (B2 stable), but the compression of earnings and cash flow is nonetheless value destructive for the sector. We anticipate pricing pressure and low prices to continue over the next several years.

China remains a large iron ore-producing country, though its mines are higher cost and their output is of a lower iron content. However, the thesis that high-cost producers, particularly in China, will exit the market and reduce supply may take longer than expected to come to fruition. Many of the iron mines and steel companies within China are state-owned and captive supply within the steel industry could result in sustained operations despite losses.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.