by Chris Becker

It was an inauspicious start to the trading week last night as US and European stocks faltered following the mad dash on Friday nights NFP print. Bond markets were notably quiet but the action was again in currencies, with King US Dollar slipping off its throne sending all of the crosses higher.

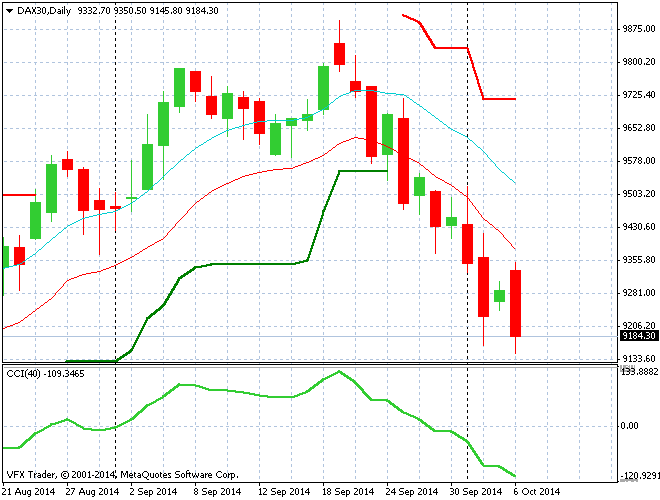

First in Europe a very mixed bag of retail and construction PMIs alongside the closely watched German factory orders print (which tanked), which I’ll cover in detail later this morning. The German DAX fell to a new low in its correction, while the FTSE also dropped but both only the latter recovered in futures trading.

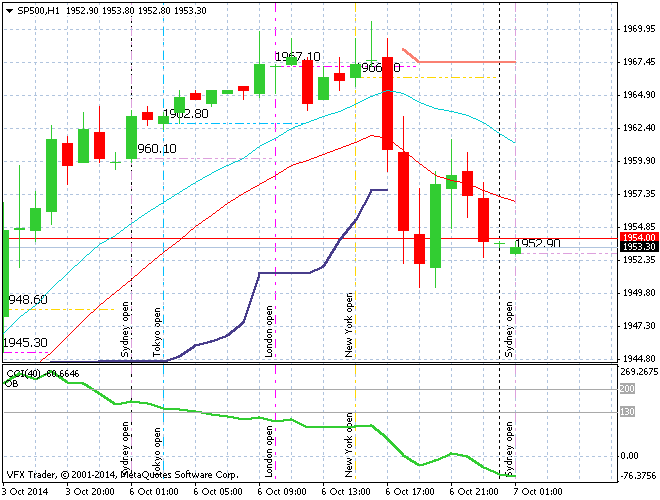

US stocks could not breach the post Friday high in early trade and reversed quickly in a zero data session, following the European bourses:

The inability of the S&P500 to close above the Friday rebound high is ominous – still not enough bulls around to make a difference yet.

The SPI Futures for the ASX200 are up 20 points, probably on the UK ADR bid on Rio Tinto (RIO) stock following merger rumours with Glencore. RIO will probably gap open higher today possibly pushing BHP up with it, so this could give the local bourse a big bounce, or at least an opportunity for shorts on longer time frames to double down.

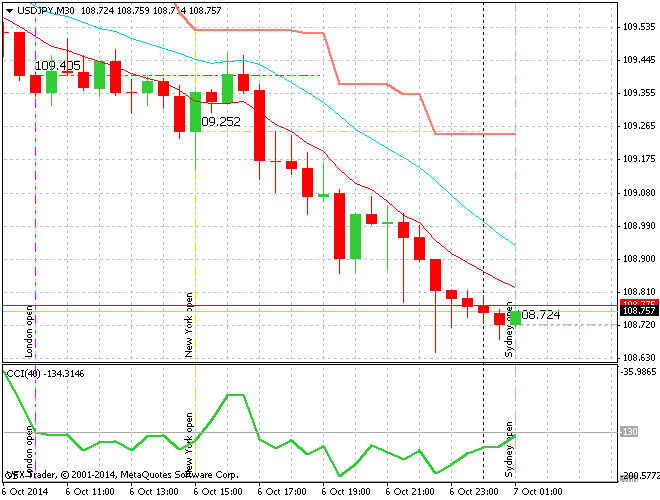

But the real work was in currencies, with the Yen appreciating strongly as the USDJPY cross feel from its 109 high to 108.75:

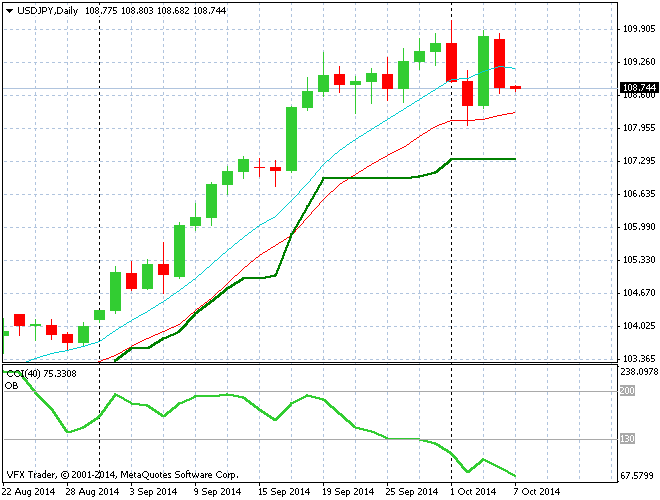

The daily chart paints a possible juncture here for the Yen with a tight range forming between 107 and 110:

This action will likely send the highly correlated Nikkei 225 into the red this morning where it remains under selling pressure unable to get above the 16000 handle.

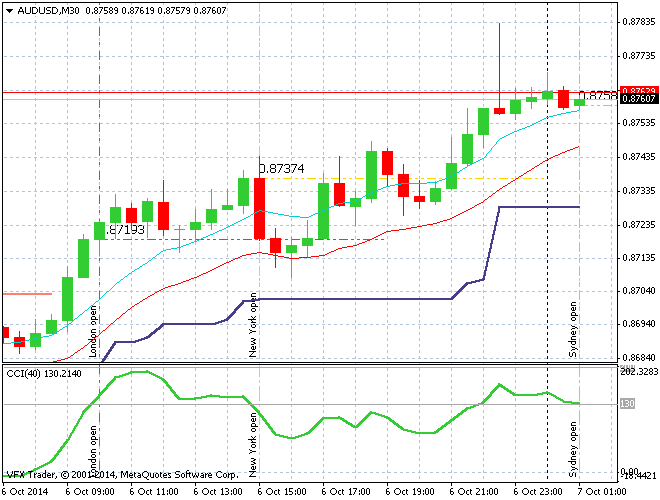

Ahead of the RBA meeting this afternoon, the Aussie battler is building on gains and from its support bottom and almost hit the 88 handle last night:

Its now slightly above the Friday pre NFP support line and could shoot much higher on rising – but wrong – expectations that the RBA may consider rate hikes next year to temper any rise in tradeable inflation due to the lower dollar. A quick look at the four hourly chart shows significant resistance at the 8825 area, so a break above that could spark a new rally, but for mind the range between 8650 and 8825 will be the norm for awhile longer.

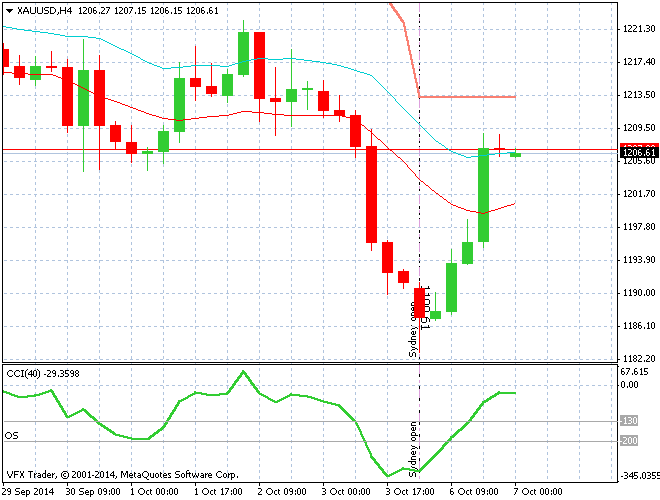

Gold finally saw some luck and rebounded nearly $20USD an ounce to just under $1208 following the USD weakness:

Silver enjoyed a similar bounce, but both precious metals still remain under enormous, if too negative sentiment pressure. I’ll have more to speak about that later today as well.

In other commodities, copper was fairly flat on the LME while agriculturals saw solid bids, mainly on the USD weakness theme.

The data prints today will be central bank focused. The RBA monthly rate decision is at 2.30 AEDT, with the BOJ releasing its monetary statement this morning and the BOE doing the same tonight.