What next? Two scenarios for 2015-16

We expect Chinese steel production to grow by 2% and believe that further upside from stimulus spending is highly unlikely given the shift away from investment-led growth that is unfolding across the economy. The market needs to absorb a c.110Mt surplus in 2015, roughly double the c.60Mt surplus it absorbed this year via mine closures and restocking at Chinese ports. Our price forecast assumes that mine closures continue in China as the price differential with imported ore narrows and domestic producers are fully exposed to US$80/t seaborne iron ore. Ex-China, we assume that marginal production continues to be price-sensitive and that mine closures take place in a timely manner.

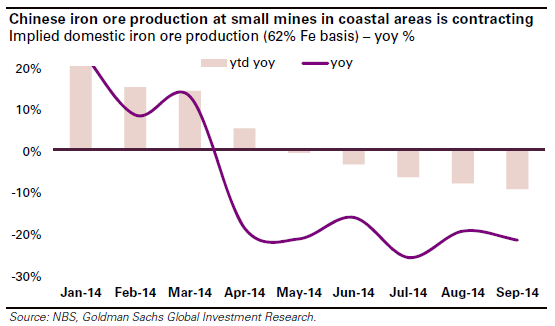

Iron ore prices could undershoot relative to our forecasts if either of those assumptions proves to be wrong. If the market continues to require a substantial discount on seaborne ore, Chinese mines would remain relatively sheltered from low import prices and further price declines would be required to balance the market. Alternatively, marginal producers (in China or overseas) may choose to delay closures as long as they can finance operating losses in the hope to eventually returning to break even via lower unit costs. In China, the capacity at risk consists mainly of small, labour-intensive mines in coastal regions that account for approximately 20% of Chinese production but the net decline in domestic supply could be smaller than expected if production in other regions is increasing. In either case, prices could undershoot relative to our $80/t forecast in a similar way to thermal and metallurgical coal, where prices have undershot by approximately 20% relative to our estimates of marginal production cost.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.