by Chris Becker

Its National Day holiday in China with markets closed so no iron ore price data. Instead I’ll update Houses and Holes so-called “idiocy spread” of the ASX listed iron ore miners, both senior and junior.

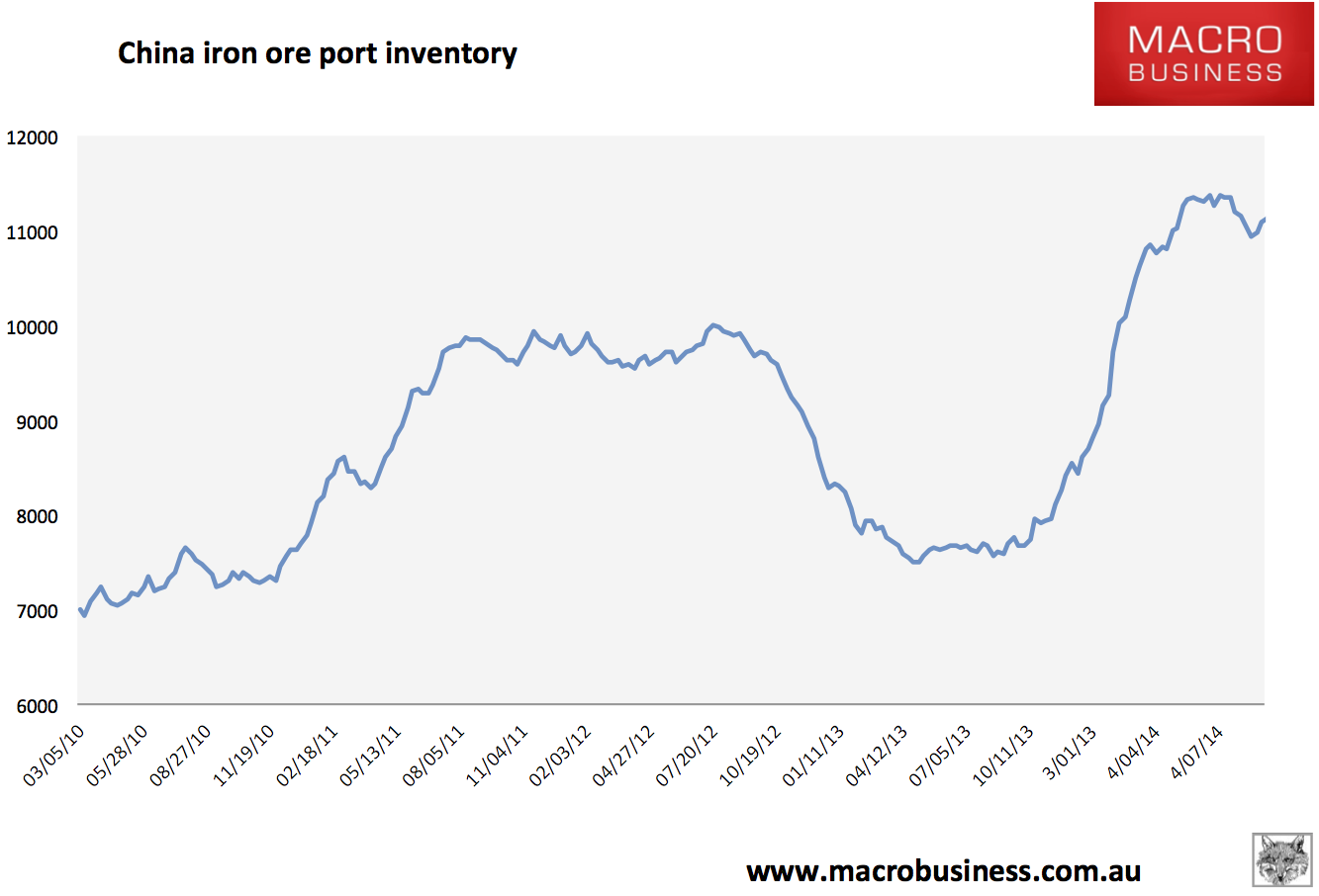

First though, a quick look at weekly Chinese port inventories which remain stable and elevated:

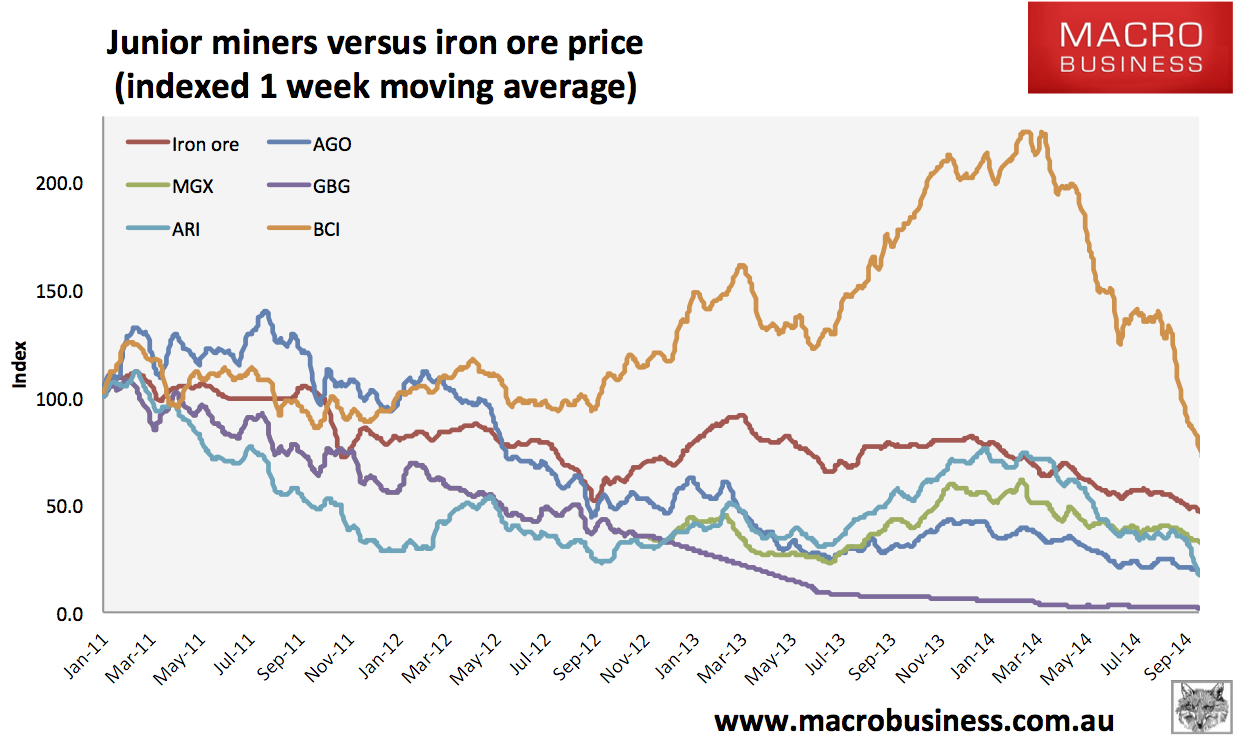

The relative performance of the junior miners vs the spot iron ore price:

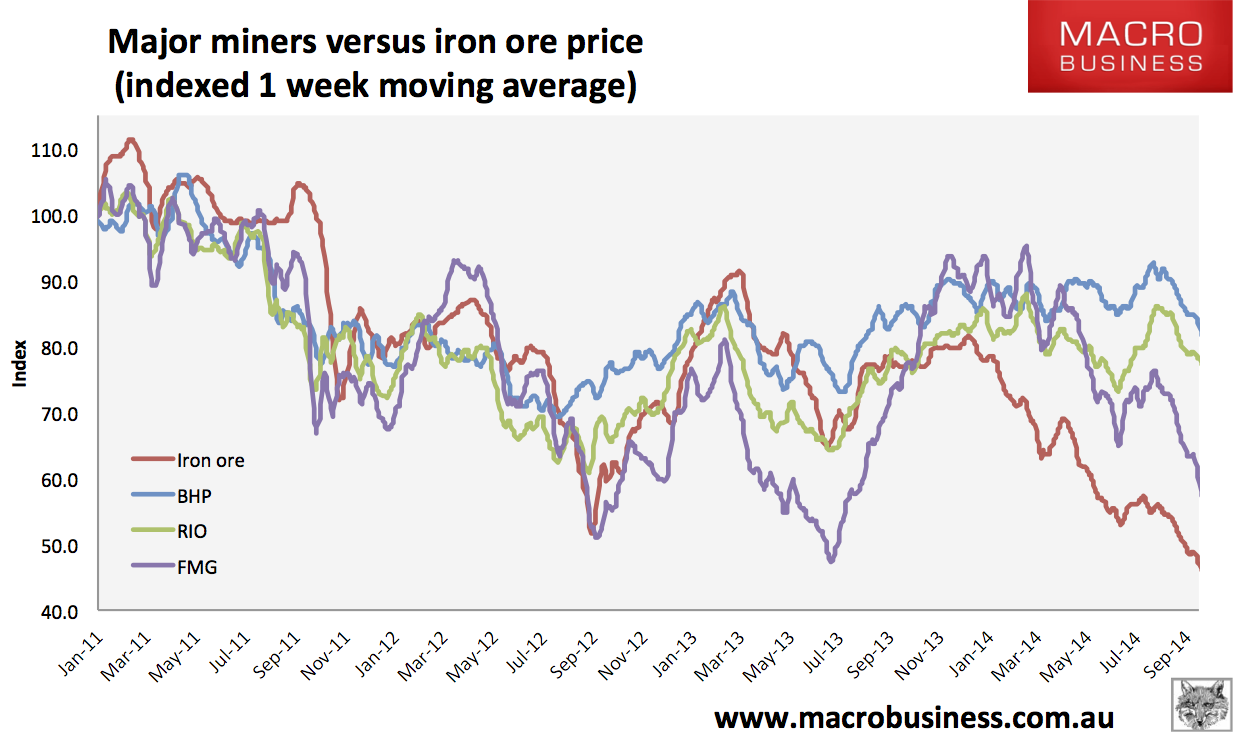

And the senior miners:

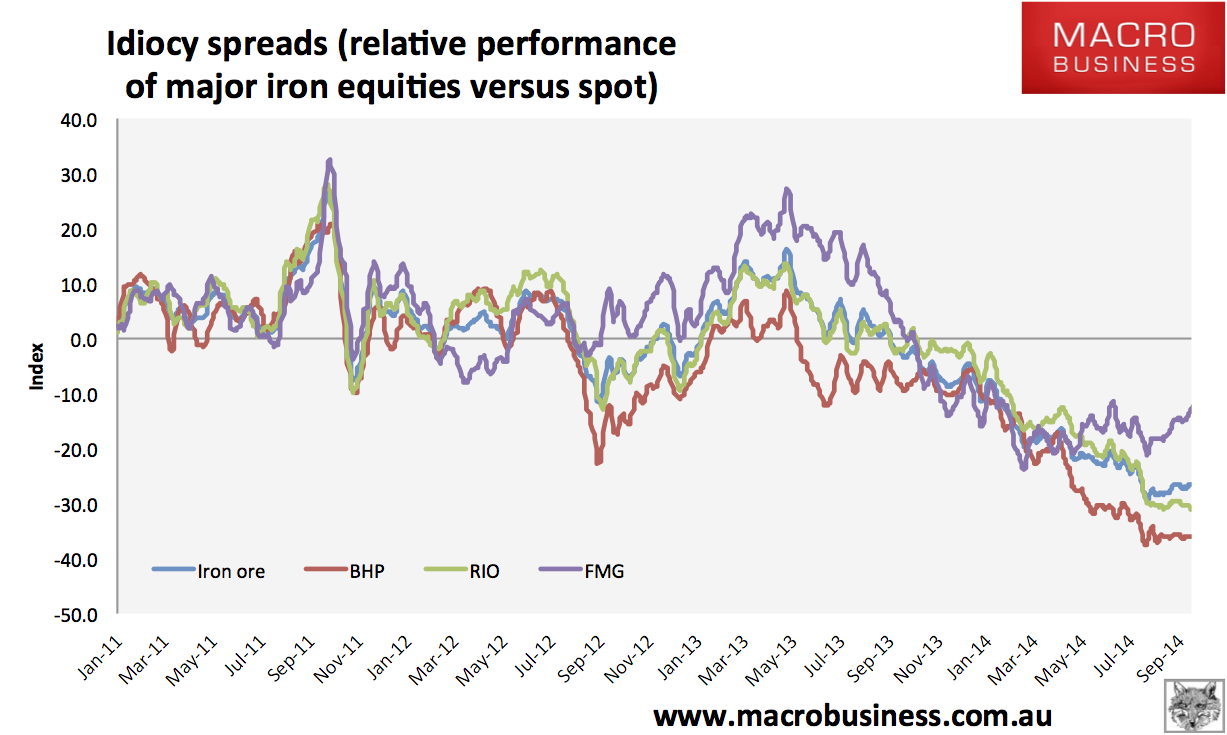

And the “idiot spread” where it looks like FMG still has some catching up to do:

Adding to RIO’s bravado over expanding its iron ore operations in the Pilbara, covered here yesterday, BHP is looking to ramp up its own supply glut, by some 65 million tonnes!

More from The Australian:

…the annual capacity of the Pilbara region iron ore mines, ports and railways could be expanded by 65 million tonnes, to as much as 290 million tonnes a year, at a cost of $US50 a tonne of annual capacity. That represents an expansion of as much as $US3.25bn, for 20 million tonnes more capacity than previously targeted at half the previous cost a tonne.

When [BHP Billiton’s iron ore president Jimmy Wilson] fronts investors and media on Monday, analysts are hoping for details on the timing of the expansion, costs and how BHP plans to extract an unaccounted 14 million tonnes of extra production beyond a flagged expansion of the new Jimblebar mine.

UBS has said the August revisions to the cost and size of the expansion could add $US10bn to BHP’s net present value.

This seems like a doubling down on the “lets divest and concentrate” strategy that BHP (ex Billiton) is employing – at potentially high risk. And it has some of its shareholders rightly worried:

While BHP and Rio can still make close to 50 per cent margins at prices of $US77 a tonne — down from $US135 at the start of the year — the rapid price decline is eating into cashflows and will impact on the miners’ ability to return cash to shareholders.

BHP’s biggest shareholder, the London-based BlackRock resources fund, this week indicated it was not completely happy with the BHP and Rio philosophy of pumping as much iron ore as possible onto an oversupplied market.

“The majors have been showing greater capital discipline but they need to keep on this path,” BlackRock head of resource equities Evy Hambro told London’s Financial Times yesterday.

“The iron ore market is already in surplus, so miners need to decide if it is wise to spend more money adding additional tonnes or not.”

Indeed. Although one thinks a potentially better choice, if the decision is to concentrate on iron ore, coal and copper, is to buy out some of the juniors – even FMG – at bargain prices with their large cash balance. Maybe wait til FMG is below $3 a share?