Charlie Aitken reckons iron ore and oil have bottomed:

Importantly also for Australia, and I may well be on my own saying this, but I think the iron ore price has bottomed for the year and will track higher ($95t target) on seasonal restocking from China. It also appears spot Oil prices have bottomed and will also edge higher. Last night the base metal complex also bounced on Chinese GDP data and if I am right and our key commodity prices have stopped falling, and in fact start edging a little higher, you will see buying coming into the beaten up Australian resources sector.

You can ONLY make money in resources if the underlying commodities are rising. Probably more accurately, “not falling”, if the company in question has production growth. That is coming in Q4 for the Australian resource sector and I suspect we all need to be a touch braver and buy a beaten up resource name or two.

For private investors the best risk/reward/quality/diversity option remains BHP Billiton (BHP), which is effectively an ETF over iron ore, oil, copper and coal. BHP has fallen sharply due to a lack of capital management at the FY14 result, UK pension funds agitated that they won’t get a UK listing of spin-off co, and general weakness in commodity prices. However, those sentiment drives are now stabilising or reversing and you can see in the chart below that the knife has stuck in BHP. After an -18.5% peak to trough fall since August it’s time to buy a few more BHP.

BHP: knife sticks

For those wanting pure iron ore exposure the answer is Fortescue Metals Group (FMG). Again, this doesn’t require over-analysis. FMG trades like a listed spot iron ore ETF. The 12 month correlation below confirms that. I think both spot iron ore and FMG have bottomed. If I am right and iron ore recovers to $95t, then if this correlation holds, FMG would bounce back to $4.50 a share.

FMG vs. spot iron ore

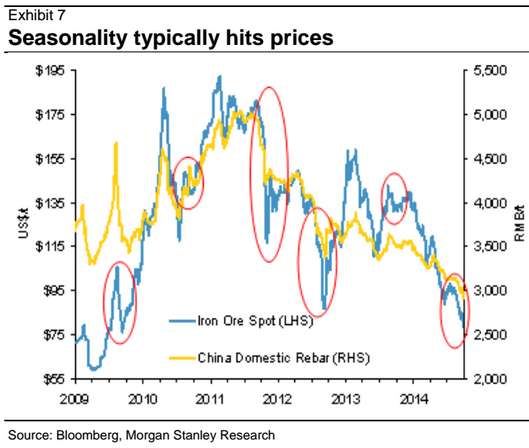

Whether you rate these calls really depends upon your time frame. Iron ore will go back to $95 if there is a year end restock in China (and Charlie does say “bottomed for the year”). This was the basis of the Morgan Stanley call yesterday as well, that seasonality will prevail:

The restock is driven by three factors, none of which is important alone but the combination has been enough to force quite large restocking Q4 pulses in previous years. First, steel traders have traditionally restocked in Q1. Second, the Pilbara cyclone season can disrupt supply. Third, Chinese holiday periods disrupt the supply chain and inventories offset the lumpiness.

Advertisement

Also in favour are the PBOC’s efforts to turn around Chinese property. The rocketing BDI shows many others are prepared to pile into this trade as well.

But, there are good reasons to doubt the restock this year. China’s steel traders have restricted access to credit to finance a rebuild of inventories. Worries about supply disruptions cease to matter in a structural oversupply. Inventories remain high for steel and iron ore across the complex and it appears the Chinese property resuscitation will be narrow. There is a bit of a head fake around recent more bullish action as well which has been juiced by the Hebei disruptions around APEC.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.