Find below Westpac’s preview of the September quarter consumer price index (CPI), which is due to be released by the ABS on Wednesday:

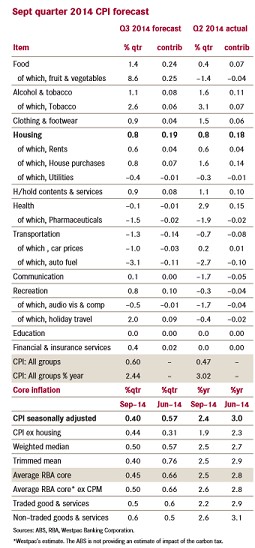

Westpac is forecasting a 0.6%qtr rise (2.4%yr) in the headline CPI in the September quarter.

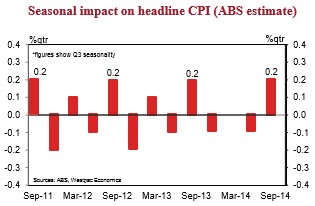

September is historically a seasonally strong quarter due, in part, to the annual price setting for administrated prices (such as utilities, property rates and charges). The ABS seasonal factors suggest that this positive seasonality is worth +0.2ppts with the seasonally adjusted CPI forecast to rise 0.4% in Q3.

The core measures, which are seasonally adjusted, are forecast to rise 0.5%qtr/2.5%yr (on average) which drops the 6mth annualised pulse to 2.2% from 2.5%.

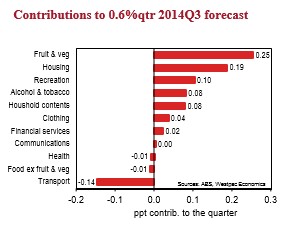

The removal of the carbon tax clearly has a meaningful impact on the September quarter CPI via its direct impact on power and utilities bills. However, the second round impact on broader prices is a key unknown. Westpac has assumed that the second round effects from the removal of the carbon tax will be marginal, at best. All up we estimate the removal of the carbon tax is worth –0.3ppts for the Q3 CPI.

Other key factors for the low CPI print are: falling crude oil prices which has resulted in auto fuel prices falling 3.1%qtr despite the weaker AUD; pharmaceuticals’ usual Q3 fall; and clothing & footwear prices held back by soft demand.

Offsetting the weaker prices are robust gains in food (which is mostly explained by strong price gains for fresh fruit & vegetables), housing (rents and house purchases) and tobacco (an increase in excise).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.