The Guardian’s Greg Jerico has done a nice job today highlighting the shallowness of Western Australian premier, Colin Barnett’s, bleating over rising iron ore supplies and falling prices:

[Colin Barnett] has accused the two big miners, BHP Billiton and Rio Tinto, of flooding the market with iron ore and thus bringing down the price. The collapsing iron ore prices are set to smash the WA and Australian government’s budgets. But the governments can’t blame the miners when both budgets anticipated much higher iron ore prices than we now have…

[Barnett] told the Western Australian parliament on 16 October: “The major companies are pushing increasing volumes on a month-to-month basis into the market very conscious that they are contributing to price falls in an already depressed market”…

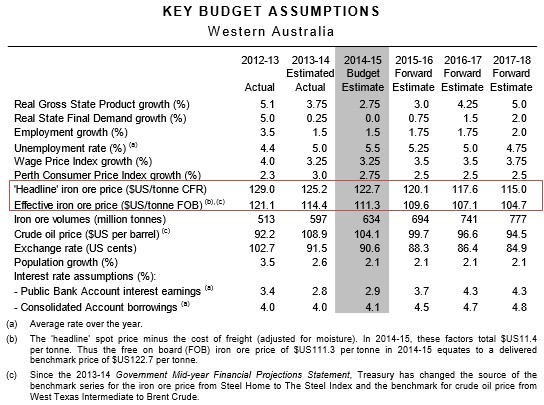

The Western Australian budget estimated iron prices to average US$122.70 in 2014-15. Currently, the spot iron price is around US$80 – 34% lower than forecast…

Western Australia was budgeting to take in $5.598bn in mining royalties from iron ore production this financial year…

The hit to revenue has been estimated… at $49m for every $1 drop below the estimated price. This financial year, the average price for iron ore has been around $86. At such a price, the hit to the WA budget would be around $1.7bn – a rather large amount given the forecast surplus for WA was just $175m.

No wonder Colin Barnett is looking for someone to blame.

The problem is, if he wanted to complain about increased production he also needs to target those medium to smaller mining companies he was so eager to defend…

In reality what is happening is increased competition. BHP Billiton and Rio Tinto are trying to gain advantage as any company would do in their position and FMG and other miners are doing their best to churn out as much iron ore as they can as well.

Welcome to capitalism, Premier Barnett.

It’s also a bit rich of Barnett to gloat over new mining operations and then complain about increased production. In April this year he was only too happy to open the new BHP Billiton Jimblebar iron ore mine and remark that it “demonstrates BHP Billiton’s ongoing confidence in the strength of WA’s iron ore industry”.

Gee, who would have thought increased investment in mining would lead to more mining?

Of course, Jericho’s thinking aligns with MB’s David Llewellyn-Smith, who a fortnight ago noted the following about Barnett’s whining:

Over the past year, BHP and RIO have increased iron ore output by roughly 40 million tonnes (mt) each. Fortescue has increased its output by 100 mt. The iron ore price is not falling owing to spooky collusion, it’s falling owing to the rise of competition. As I recall, a basic principle of increased competition is that prices fall. Ironically, it is Barnett who is openly campaigning for BHP and RIO to collude by agreeing to not respond to a competitive threat.

The reason why is obvious enough. His budget is a laughing stock having forecast iron ore prices of $120 forever. A resource producing state really aught to have someone in charge who has a clue about resources.

If Barnett should blame anyone, it’s his own Treasury department, whose forecasts of a permanent high plateau in iron ore prices were always hopelessly optimistic (see below table).

Brought about by bullish internal views about Chinese steel demand and that higher cost Chinese iron ore supply would cease placing a ‘floor’ under the iron ore price:

China’s iron ore demand is expected to grow by 3.2% per annum over the budget period, to reach 1.2 billion tonnes by 2017-18…

Growth in low-cost supply is anticipated to place downward pressure on price… [However] as [Chinese] supply is gradually withdrawn, this should provide a floor to the price.

Isn’t free market capitalism a bitch, Colin?