Business Spectator’s Alan Kohler has continued his schizophrenic take on Australia’s housing market, today arguing that concerns about excessive speculative activity in the housing market are not warranted because credit growth is so low:

There’s talk of macroprudential policies to limit investment lending, but no one is rushing into this, and for good reason: there isn’t really a problem.

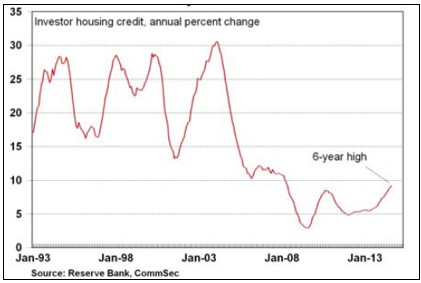

There were three booms in property investment during the 1990s, when investor housing credit grew at between 25 and 30 per cent per annum. The current growth rate is anaemic by comparison.

This argument is trotted-out regularly as a defence to the claim that Australian housing is a bubble. But it is also faulty logic and is a very poor way to measure risks.

Advertisement

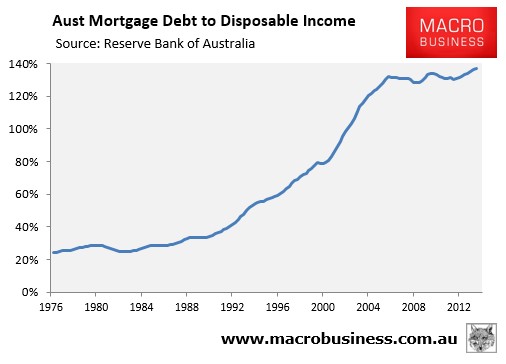

On Friday the RBA revealed that the ratio of outstanding mortgages to household disposable income hit a record high 137.1% in the June quarter (see next chart).

Moreover, yesterday’s credit data from the RBA revealed that mortgage credit growth – 6.7% in the year to August – is growing at well over twice the pace of wages (2.6% YoY).

Advertisement

Essentially what Kohler is arguing is that present credit growth is not a concern because the outstanding amount of debt is huge. But this is precisely why mortgage growth at more than twice the pace of incomes is a concern. Mortgages are rising from an already highly elevated level, thereby increasing risks to the economy and financial system.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.