Despite the clear and present warning presented by Arrium today, the froth just won’t leave the iron ore market. From Fairfax:

Iron ore’s slump to a five-year low isn’t expected to prevent the world’s two biggest miners, BHP Billiton and Rio Tinto, returning cash to investors, a JPMorgan Chase fund manager said.

“You have to remember the very large operating margins which can still be achieved within iron ore,” James Sutton, a portfolio manager at JPMorgan’s $US1.6 billion ($1.78 billion) Natural Resources Fund in London, said. There’s “a lot of scope for shareholder returns,” as Rio and BHP are curbing investment in marginal projects, he said.

“Looking at the bigger picture, I think that the two things are not incompatible,” Sutton said. “These businesses will have to get used to a lower iron ore price environment. They may become more boring as a result and focus on those core assets and focus on getting more and more margin out of them. That will ultimately lead to higher dividends and buybacks.”

Mental note: sell JPMorgan. Why would I buy a miner with a collapsing underpinning price as an income stock? For that matter, why would I buy a highly cyclical and volatile miner as an income stock at all?

Meanwhile, at the AFR:

AngloAmerican chief Mark Cutifani says he expects metallurgical coal mines will be mothballed at a rate of one every two or three weeks until enough supply has fallen out of the beleaguered sector to drive a price recovery.

…The market is in oversupply and Mr Cutifani says, “if the price is not north of $US150, you’ve got stress right across the industry.”

… “We’ve been seeing some production come out of the market, 20 to 30 million tonnes,” Mr Cutifani says.

…He said more than 30 million tonnes would need to disappear from the global market “to have any sort of meaning”.

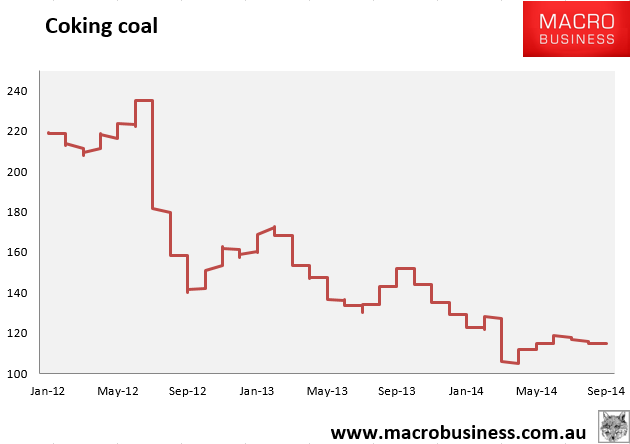

Mental note: sell Anglo American. What is going to happen is more of the same. As demand plateaus, every bump in the price is going to be met with an avalanche of renewed idle supply. Here’s the coking coal chart:

Unless supply is dramatically concentrated, it will never recover. Lowest marginal cost of production is back no matter how short the memories of miners.