Demand & Pricing: near-term strong Q4 restock upside

We believe that near term, a Q4 seasonal restock should still support prices for the rest of this year. Despite a gloomy longer-term price outlook, we still see several reasons why mills may pick up seaborne inventory in the fourth quarter:

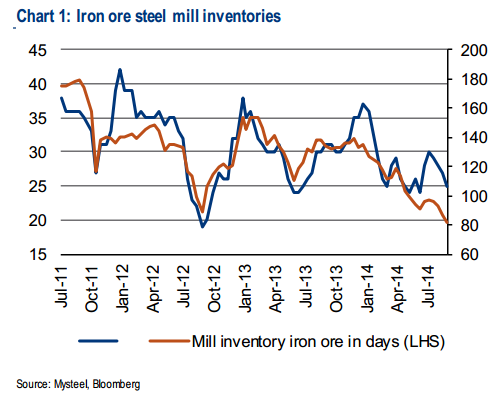

1) Inventories of 25 days are now closer to trough levels, and we believe mill/trader destocking activity will naturally fade at lower prices here.

2) Chinese domestic production usually dips in Jan/Feb during CNY and the Chinese winter, leading to restocking of imported ore in November/December. Over the past 3 years, mill inventories have risen +5, +12 and +11 days, respectively, from end November to the January peak.

3) The risk of weather disruptions in Australia and Brazil in Q1 also encourages mills to hold higher stocks, and provides the potential for prices to surprise to the upside in Q1. Q1 invariably marks the peak for iron ore prices each year. As chart bottom left shows, inventories at mills usually peak around January each year. The table on the bottom right outlines the potential positive impact to apparent demand from a restocking event even just to 35 days.

I am of the view that there is very little chance of a restock to 35 days inventory because:

although the seasonal factors are still there the economic context is terrible and getting worse;

25 days is not especially low when we add the large port stocks;

none of the past cycles had these factors nor did they transpire in a context of structural oversupply so assuming the same outcome is very hopeful analysis.

A better base case is 30 days and that is worth $10 to the price.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.