A general restriction which applies to all coal limits ash content to 40% and sulphur to 3%, with more rigorous conditions according to energy content and coals which travel beyond 600km from either port or mine. Lignite consumed within the 600km threshold will need to have ash below 30% and sulphur below 1.5%. The document also spells out limits on other chemical content such as mercury, arsenic, and chlorine.

Coal which travels beyond 600km across the mainland will need to meet more stringentconditions – ash content can be no greater than

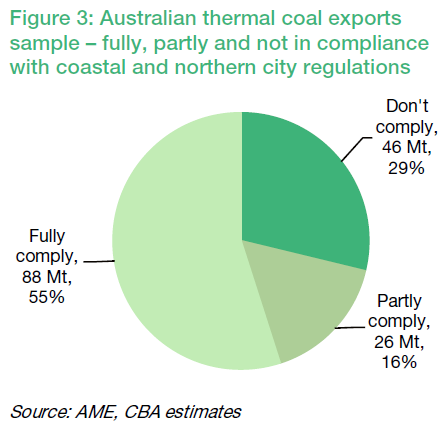

20% and sulphur no more than 1%. On face value, Australian exports aren’t likely to be impacted, with typical 5,500kc NAR Australian material containing ash content between 23-25% and sulphur between 0.8%-1%. Equally, Indonesian lignite is renowned for low impurity and would likely fall under the lignite ash and sulphur specifications.

However, tighter restrictions for coal consumed in key population centres including Beijing, Tianjin, Hebei, Shanghai, Jiangsu, Zhejiang, and Guangdong may indeed impact seaborne material. Coal consumed (not produced/stored) in these regions will need to have ash content below 16% and sulphur below 1%, which means most imports into these regions will need to be washed/blended.

These regions account for roughly half of China’s annual thermal imports, or 100mt. Australia suppliesthe whole of China with close to 60mtpa (Figure 1); half of this (30mt) could potentially be affected. Chinese domestic material is perhaps even more impacted – particularly high impurity coal produced in the northern part of the country which carries ash content up to 40% and sulphur up to 4%. This material will meet neither the general restriction nor the more stringent major city restriction.

CBA concludes:

The impacts on coal producers are likely negative overall. Any noncompliant coals currently sold into China could be re-directed to other markets, if those markets have capacity to absorb lower quality coal. Producers could wash higher ash coals more in order to meet the new guidelines or blend higher ash with lower ash coals – but both options involve higher costs for the Australian mining sector, already under siege from low prices, high costs and a strong Australian dollar. We are not convinced demand (and pricing) of higher quality coals will rise as a consequence. Ultimately, we believe China is trying to slow or reduce coal consumption and that cannot be positive for overall seaborne trade or pricing over the medium term.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.