Bank of America-Merrill Lynch chief economist, Saul Eslake, has produced a great new report explaining why Australian wages and spending growth will remain subdued, which translates into an expended period of low inflation and low interest rates:

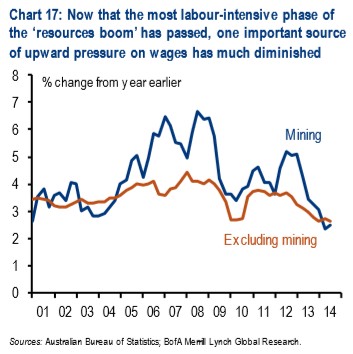

Australian wages growth has slowed markedly since mid-2013

Wages growth has slowed significantly in Australia over the past year. Growth in what is widely regarded as the ‘best’ measure of wage costs is now running at its lowest rate since the series began 16 years ago. Real wages are now falling for the first time since the recession of the early 1990s, apart from a brief interval during the global financial crisis…

‘Catching up’ with other ‘advanced’ economies

Unusually low nominal wages growth (and declining real wages) have been fairly commonplace in other ‘advanced’ economies since the global financial crisis. Australian workers had been insulated from this experience by the strong demand for labour associated with the ‘resources boom’. But now that the labour-intensive phase of the ‘boom’ has passed, on-going weakness in the demand for labour in other sectors is putting downward pressure on wages growth.

Low wages growth likely to be sustained

Wages growth is the ‘laggingest’ of lagging indicators. It lags unemployment, which in turn lags the broader business cycle. Since neither we nor (now) the RBA expect unemployment to begin falling until early 2016, low wages growth is likely to be a feature of the Australian economic landscape for the next two years.

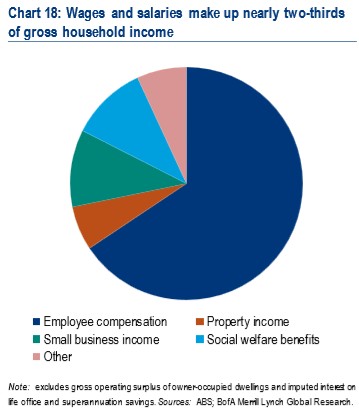

Low wages growth means weak household spending …

Wages account for almost two-thirds of household income. In the absence of any offsetting influences (and we don’t expect any), slow wages growth means slow growth in consumer spending – which in turn accounts for more than half of GDP.

… and lower inflation, especially in services

Wages represent just under one-third of total business costs, but over 40% of total costs in the services sector. Sustained slow wages growth should help to moderate inflationary pressures in the (largely non-trade exposed) services sector.

It all adds up to an extended period of low interest rates:

This combination of sluggish growth in household consumption spending and lower services sector inflation adds to the case for the RBA to keep interest rates at their current record low for an extended period. We don’t expect a monetary policy tightening cycle to commence until the first half of 2016.

Eslake is mostly correct in my view. Those expecting the domestic economy to fire on the back of the consumer are likely to be disappointed, as are those calling for interest rate hikes.

Advertisement

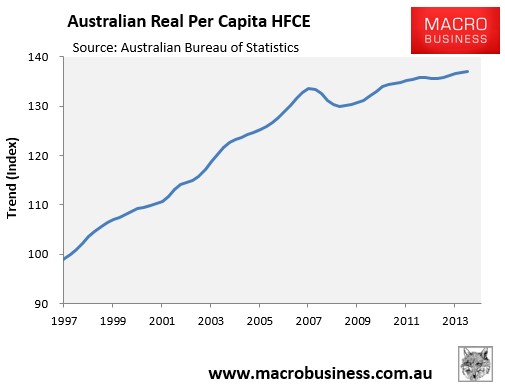

Per capita household financial consumption expenditure (HFCE) has slowed considerably since the GFC – increasing in total by only 4.5% since 2008 (see next chart) – and is highly unlikely to fire back up in light of the sluggish income growth and deteriorating employment situation arising from the unwinding of the mining investment boom, as well as the shuttering of the Australia car assembly industry.

My only minor disagreement with Eslake is that I believe the next move interest rates – whenever that is – is likely to be down. I just can’t see the RBA hiking rates in the first half of 2016 amid falling real incomes and rising unemployment.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.