Morgan Stanley slapped a short on FMG in late July which has worked quite well (it was $4.60 then versus $3.92 yesterday). Today they upgrade:

Fortescue has slipped below our target price so we are upgrading our rating to EW. Our house view that the iron ore index price will recover, and if it does recover, FMG can continue to reduce debt and lift dividends. We also see upside potential in expansion and gas conversion.

Price event is seasonal: Our Commodities team is of the view that the iron ore index price can rebound to the mid-US$90/t level. The current equity price has captured a flat spot price outlook limiting downside risk unless iron ore prices deteriorate further.

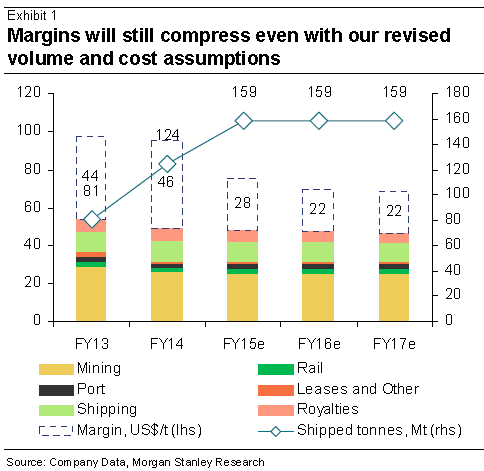

Increased sales volumes into the base case: We had applied conservative sales, but increase it 4Mt to 159Mt for FY15e after 15Mt were shipped in August. This and a revised cost assumption created the EPS uplift.

While August sales were likely bolstered by inventory sell down, the risk of underperformance is abating.

Upside scenarios not in the base case: We find that creeping expansion to 175Mtpa and converting the Truck fleet to gas could add A$1.50/sh to the valuation and US$800mn to EBITDA over the next four years. This isn’t in our base case, only in our bull case valuation.

This benefit was balanced by a revision of our Bull, Base & Bear case weightings from 20-60-20% to 15-60-25%. Price the greatest risk to the upgraded view: Volume and cost misses would needed to be ~30% to have the same impact as the index price staying below US$85/t. An index price of US$75/t is sufficient to cover all operating and corporate costs.

The amusing thing about this analysis is this: because FMG is the first large high cost producer on the cost curve it will set the marginal price as the great deflation continues. As such, any cost cuts it undertakes will simply flow back to China as cheaper iron ore, not helping the company at all.

FMG needs to lower its costs faster and below that of other producers to change this. But the next three substantive producers – Kumba, Ferrexpo and Vale – all have big leads on the break even front and will also be cutting costs like mad. What FMG really needs is a much lower dollar to help it close the competitiveness gap and why it hasn’t been agitating for it I’ll never know.

Advertisement

As for the upgrade, a very short term, very high risk, punt.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.