Fairfax has today reported that mortgage competition is heating-up, with NAB offering new mortgage customers $1,000 to take-out a home loan from the bank in a bid to boost it’s market share:

Australia’s big banks have tried to entice borrowers with cash payments worth $1000 or more in the past 12 months in effort to grow market share.

But NAB says its latest strategy is different because it is not a rebate… Instead, it will give customers $1000 on an eftpos card to spend however they choose…

It comes after NAB tried to poach customers from its competitors last September when it offered $1000 if they switched their home loan to the bank by the end of that month.

Soon after, Westpac topped that offer, giving customers a $1500 cash rebate if they borrowed $500,000 or more.

A string of other offers followed, with Commonwealth Bank giving first home buyers a $1000 rebate and Westpac-owned St George, Bank of Melbourne and BankSA offering $1250 to new customers.

ANZ, meanwhile, said its branch managers had discretion to pay up to $1000 to customers who switched banks with a loan of more than $1 million to help them cover costs.

Saul Eslake’s 50 Years of Housing Policy Failure presentation showed clearly that cheaper and more readily available access to credit, along with other demand-side measures, have done absolutely nothing to improve access to housing. Despite the massive decline in interest rates and improved access to credit, as well as the myriad of subsidies to first home buyers, the home ownership rate has decreased over the past 50 years, despite favourable demographics (see next chart).

Under Australia’s constipated planning system, increased mortgage competition and the relaxation of lending standards would do what it has always done: raise household debt and bid-up house prices even further, while potentially also crimping lending to productive businesses.

It would also increase risks to the financial system, heightening the prospect that tax payers could be called upon to support the financial system in the event that the housing market experiences a significant correction.

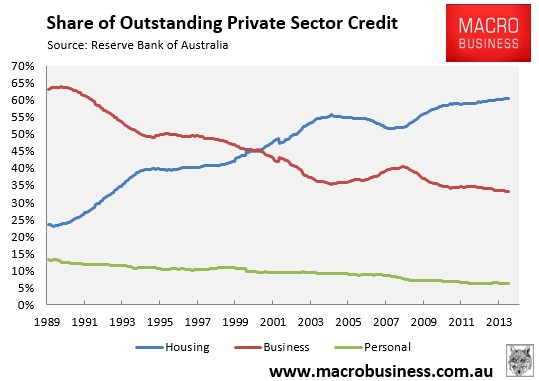

Already, the proportion of bank loans going housing has been rising and is currently at an historical high, whereas the share of loans to business is at an historic low (see next chart).

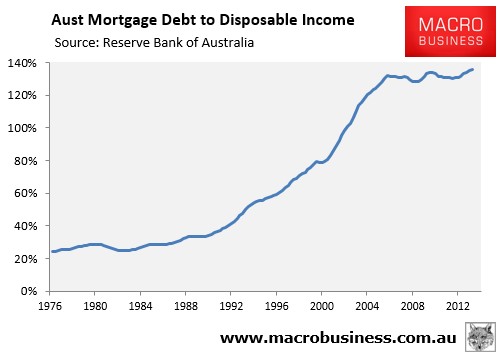

Moreover, the ratio of outstanding mortgage debt to household disposable income is at an historical high and rising fast as outstanding mortgage credit growth – 6.5% in the year July 2014 – far exceeds the growth in wages (2.6%):

Blind Freddy can see that Australia already has a mortgage problem, which makes the RBA’s/APRA’s opposition to macro-prudential controls of high risk mortgage lending – which Glenn Stevens has previously refered to as “dreaded macroprudential tools” and “the latest fad” – all the more delinquent.

The last time the banks offered these types of cash enticements to home loan customers, APRA sent a letter to all deposit-taking institutions warning them not to grow their home loan book above system.

Judging by NAB’s latest move, it obviously appears to have had little impact on bank behaviour.