“Mad” Adam Carr has once again entered bizarro world today with another post lashing “doomsayers”for being concerned about Australia’s falling national income growth and soggy outlook:

What could drive such an emotionally charged dystopian view of the economy? The main culprit is the mistaken view that national income is falling, driven by the slump in the terms of trade. It lies at the heart of this doomsday cult that seems to be running Australia and it stands behind the constant call to slash wages and cut the exchange rate. Presumably because the only way to lift national income is by cutting it!

Some of the confusion has arisen because of a debate that has been raging for many years about how we actually measure national income.

Many economists were rightly critical of the standard approach, GDP, because it fails to capture movements in the terms of trade. So they augmented it with another, real gross disposable income RGDI, which simply adjusts GDP according to movements in the terms of trade.

By this measure, real incomes fell by about 0.33 per cent in the June quarter — only a little over 1 per cent higher for the year. This well below average and, on the face of it, cause for great alarm.

Now this call is very intuitive. If the price of what we sell goes up , then we must be better off. If it goes down, then we must be worse off. Except that this doesn’t necessarily have to be the case…

And this is where I think economists are getting it wrong…

National income is so much more than the terms of trade — indeed roughly 90 per cent of our national income is household salaries and non-mining corporate profits. Moreover, the mining sector is a comparatively small employer — 1-2 per cent of the labour force only.

This is why other measures of the country’s real income, GDP for instance, show quite solid growth. This concept measures what companies and household actually earn: profits, wages, returns to investment and the like. On this basis, real incomes were up 3.5 per cent over the last year – a rate well above trend and markedly higher than the terms-of-trade adjusted figure.

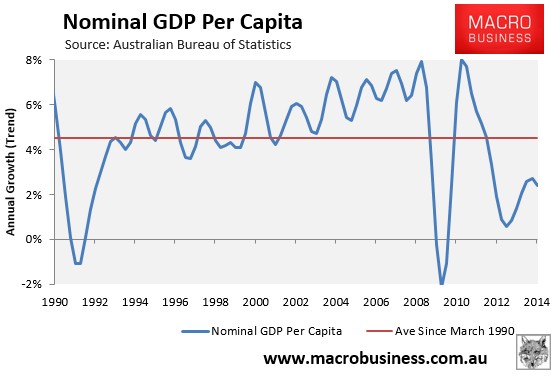

To call bullshit on Carr’s claims is an understatement. Nominal GDP is the dollar value of what’s produced and earned. And this is what it looks like when adjusted for population:

In the year to June 2014, nominal GDP per capita clocked in at only 2.4%, which is just over half the average growth rate recorded since March 1990 (4.5%).

Why is it so low? Because the ongoing falls in commodity prices an the terms-of-trade has more than offset the increase in export volumes. So in effect, Australia is producing more, but receiving far less in return – exactly what us doomsayers have been warning about for several years now.

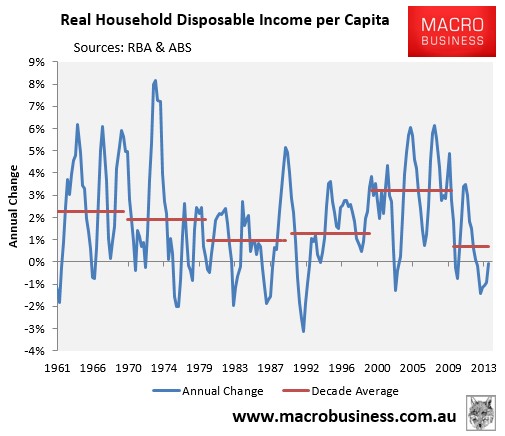

It also helps to explain why per capita household disposable incomes so far this decade have growth at a slower rate (0.7% per annum) than was recorded over the 1960s (2.3% p.a.), 1970s (1.9% p.a.), 1980s (1.0% p.a.), 1990s (1.3% p.a.), and the 2000s (3.2% p.a.):

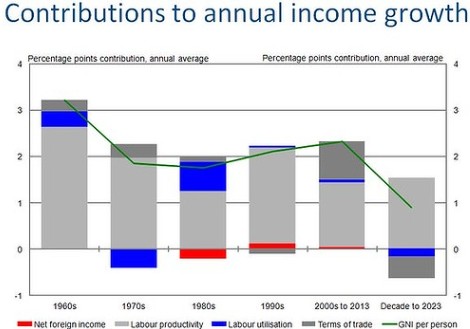

And why the Australian Treasury has forecast the slowest real per capita income growth in at least 60 years over the coming decade, again dragged down by the falling terms-of-trade:

But hey, I guess the Australian Treasury are part of the “doomsday cult” as well, according to Carr.

The funny thing in all this is that Carr has now become the ultimate contrary indicator on the Australian economy as the economy moves sharply against his every utterance.