by Chris Becker

Goldman Sachs has an interesting research note out going over the 2nd quarter Australian GDP data with a very positive spin:

While the 2Q2014 GDP data showed annual growth decelerating to 3.1% yoy from 3.4% yoy and domestic demand remaining subdued (1.4% yoy), we believe there were three positive undertones:

1) we estimate the non-mining economy to be now growing at 2.7% yoy – the fastest since 4Q2007;

2) labour productivity growth continues to improve, capping unit labour costs; and

3) there has been a modest lift in household income growth despite depressed wage growth.

It seems the meme of a “handoff” from the mining economy to the non-mining (mainly construction) remains the consensus view and on the face of it has worked so far.

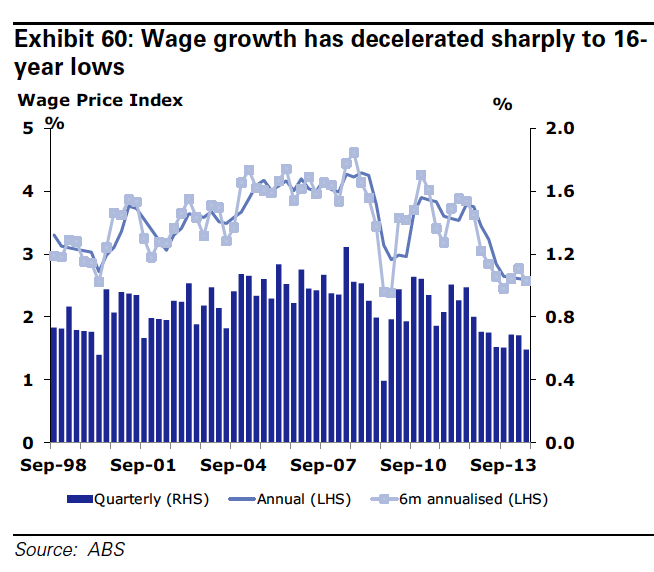

But let’s look a bit closer at these “positives”. First, the labour productivity growth is all due to lack of wage growth:

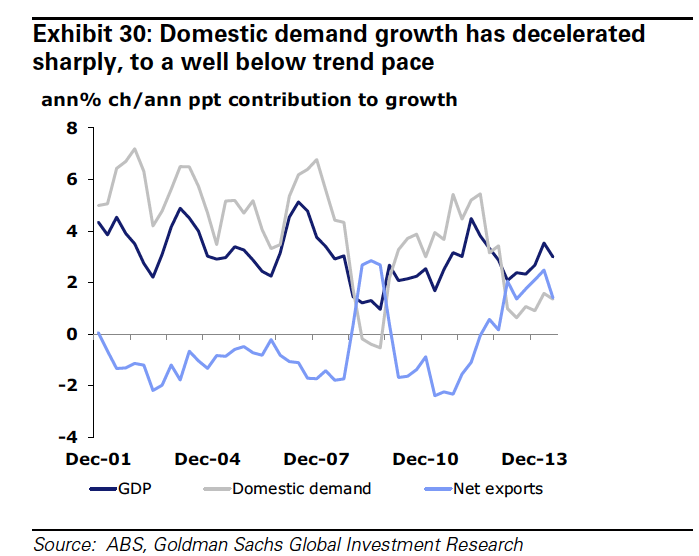

Which has translated directly into a fall in domestic demand growth – only exports are holding up GDP at the moment:

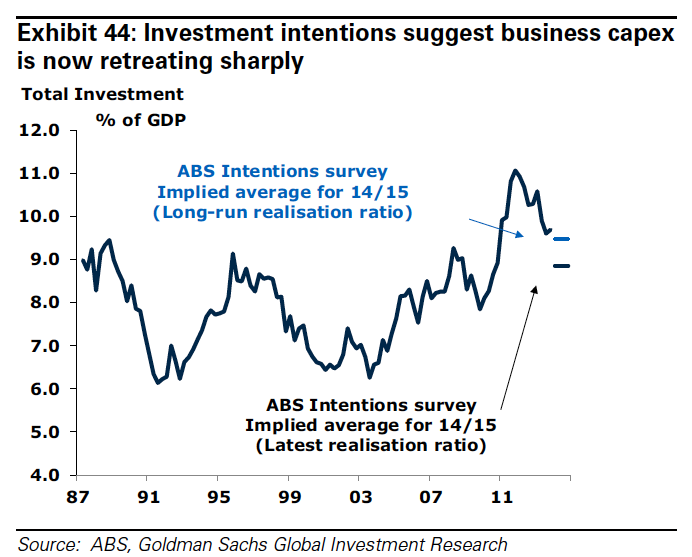

GS are right to point out the solid headwinds as the capex cliff comes closer:

…we continue to see the risks skewed towards a further deceleration in economic momentum over the coming months.

Commodity prices continue to fall, representing a considerable income shock, mining capex is now contracting and fiscal consolidation has begun.

2015 is shaping up to be an interesting year, to say the least.