The price decline has come sooner than expected

We have consistently argued that, in an oversupplied iron ore market, low prices would be required to force the closure of marginal production both in China and overseas. Although sooner than anticipated, our expectations of lower prices have materialized, with the spot price down 38% ytd to US$84/t. The price decline has been dramatic, but a weak demand outlook in China and the structural nature of the surplus make a recovery unlikely. In our view, iron ore has already transitioned to an exploitation phase where the commodity prices are typically subject to the deflationary pressure of mining productivity and the depreciation of commodity currencies. We maintain our US$80/t forecast for 2015 and we apply our updated assumptions on cost deflation by lowering our 2016-17 forecasts to US$79/78/t (down 4%, 8% respectively).

When the irrational is rational: why prices undershoot

Prices in the year to date have underperformed relative to the consensus expectations of a soft landing. In our view, this illustrates the shortcomings of global cost curves as a tool to forecast iron ore prices. The lack of adequate data on Chinese supply is a well-known challenge, particularly now that NBS statistics on production volumes send confusing signals; on balance, we believe that Chinese supply on the upside on the back of ongoing expansions that will partly offset the loss of marginal mines. Moreover, prices tend to undershoot in oversupplied markets because marginal producers have a strong financial incentive to delay mine closures even when they operate at a loss. Far from being an irrational decision, we argue that this behavior simply reflects the costs associated with idling an asset and the associated loss of option value.

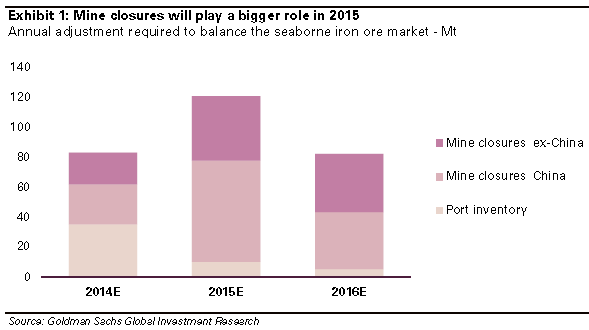

Chinese mines and stockyards not enough to balance market

As the market falls deeper into surplus, excess iron ore can only be absorbed via an increase in inventory and/or the displacement of marginal production. Since the start of the year, stockpiles at Chinese ports have seen a 23Mt increase, while low prices have forced the closure of c.48Mt in grade-adjusted Chinese and seaborne production capacity. Each of these safety valves will be tested further, in our view, but stockyard space is finite and port restocking should play a more modest role from 2015 onwards. We believe this will leave Tier 2 seaborne producers increasingly vulnerable, with up to 40Mtpa in seaborne capacity at risk of closure in both 2015 and 2016.

I personally think that the amount of seaborne supply in the gun is more like 150-200 million tonnes but what’s a few million tonnes between friends.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.