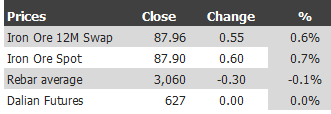

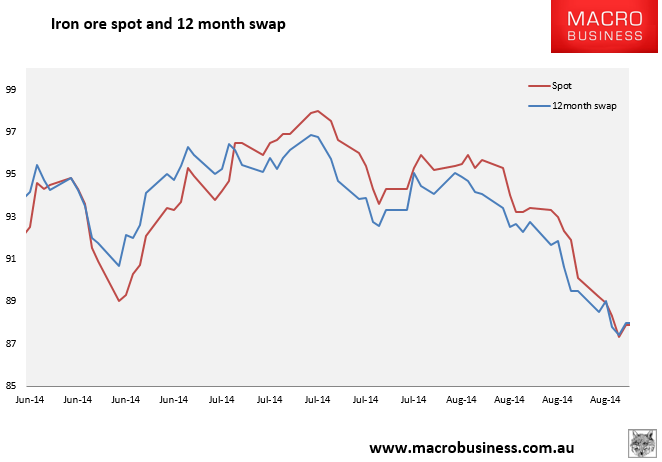

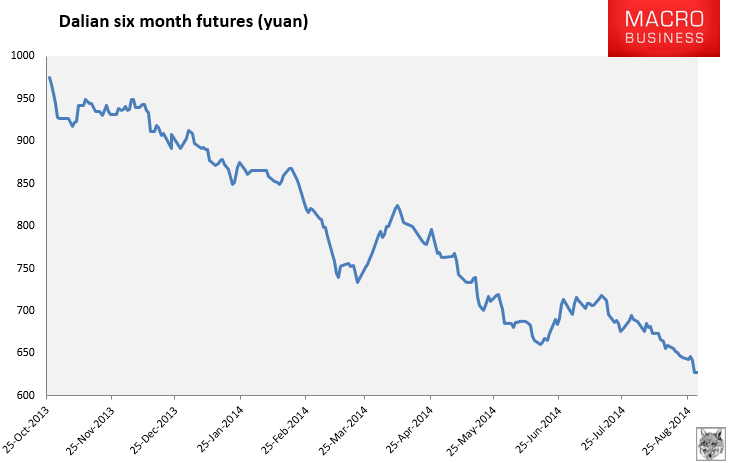

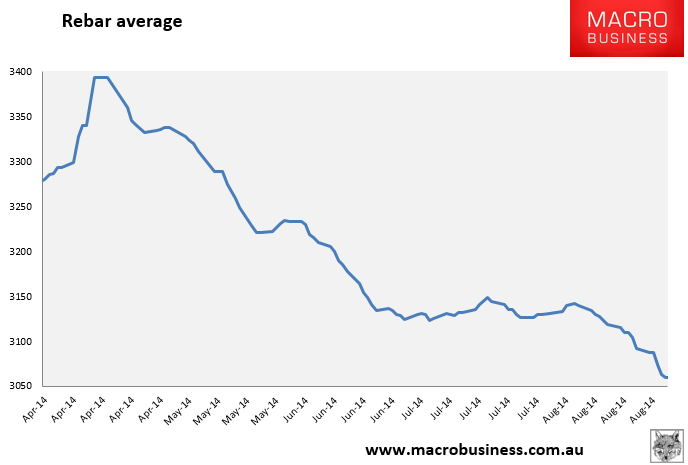

Find below the iron ore price charts for August 29, 2014:

Advertisement

Paper markets caught a break and stopped falling. The 12 month swap even managed a small rise. However, that’s closed the paltry contango with spot, which also firmed.

There are definitely punters on a bottom emerging, as seen in the big upwards reversal of miner equity prices on Friday.