With some currency relief finally apparent for Australian tradables, Citi offers a timely take on how that might affect the miners:

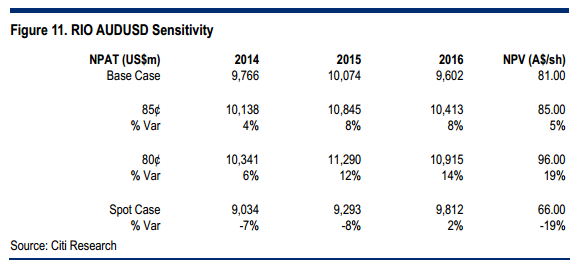

The A$ leverage is surprisingly similar for BHP and RIO, which comes as somewhat of a surprise given that RIO has historically been more levered to the A$ than BHP. This is due to the impact of the Alcan acquisition reducing the A$ exposure of the overall group and the still-high margins in iron ore (bigger exposure for RIO) being less sensitive to a lower A$ than the tighter margin coal businesses (larger exposure in BHP). Given we are bearish iron ore (US$80/t) and relatively bullish on the A$ in 2016, there is actually upside risk to our RIO estimates in 2016.

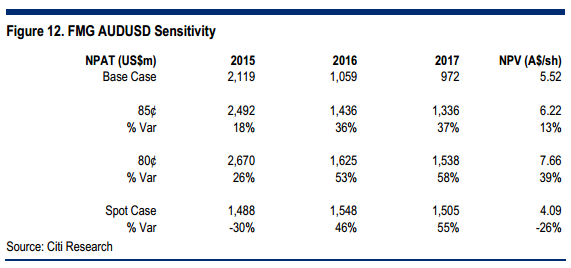

Citi’s bearish iron ore forecasts mean that the iron ore producers are highly sensitive to any movement in the A$. Aside from diesel that typically represents around a third of costs for iron ore, most other costs are in A$.

Some explaining is needed for the tables. The base case is Citi’s forecasts of an iron ore price at $105 this year, $90 next year and $80 in 2016 plus the dollar at 93 cents throughout. Deviations from forecast are from these base lines.

The diversified miners are about as expected. But FMG and the smaller miners are more sensitive to dollar movements than I thought (at least according to Citi and sell side research varies widely).

Advertisement

However, that is probably not terribly useful to them. The juniors will still make no money but they’ll go out of business more slowly. For FMG I’d make two points:

so long as FMG is the low cost marginal producer (once juniors die) amid an oversupply then the lower dollar does not help it greatly because every cost saving simply gets recycled as lower prices to China

for the dollar to help FMG it must enable it to move down the cost curve, below the break even prices of Vale and Kumba. That means the Aussie has to fall against the real and rand, which it is not. Whether it will in future is debatable given the great China adjustment will likely hammer all three currencies.

the yuan will rise with the US dollar peg and that will make domestic production more expensive but it’s still likely that the lion’s share will be supported for strategic reasons.

All of that assumes that the price of iron ore doesn’t fall to $70, in which case the dollar will have to fall further than 80 cents or everyone from FMG up won’t make a brass razoo.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.