Aussie Home Loans founder, John Symonds, has lambasted the idea of the RBA/APRA introducing macro-prudential curbs on high risk mortgage lending, instead arguing that the solution to lower house prices and improved affordability is to increase housing supply. From The SMH:

“I think at the moment it [macro-prudential] is premature”…

Big house price rises in the past year in Sydney and Melbourne are simply a function of housing supply not keeping up with high demand from fast population growth allied with low interest rates, he said. This had driven investors to buy, adding to price rises and forcing out first-time buyers.

Even using targeted measures, he said, it was not easy for the RBA and the Australian Prudential Regulation Authority to deal with that. “I think it is very hard for the prudential bodies to target without having probably some unintended consequences”…

“The reality is governments have failed to address the orderly supply of housing. There are so many reasons first home buyers have been forced out: the cumbersome bureaucracy to get land releases, the cost per apartment or housing block is anything from $100,000 to $150,000.”

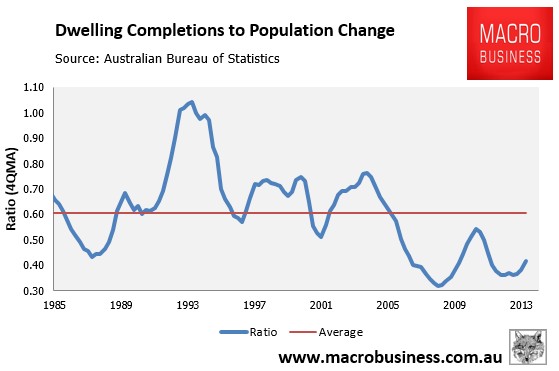

Symonds does make some valid points. As explained in detail earlier this month, the rate of dwelling construction has plummeted over the past decade despite the rapid surge in home prices, suggesting housing supply in Australia has become far less responsive (see next chart).

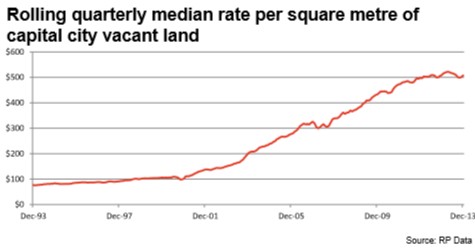

Moreover, the cost per square metre of vacant land across Australia’s capital cities has increased by around 500% over the past 15 years, with fewer lots produced in response to the rapidly rising prices (see next chart). This suggests massive interference in the land market by Australia’s governments, which has materially reduced (if not outright precluded) the supply of affordable land, contributing to the rise in home prices.

That said, Aussie John is clearly talking his own mortgage book. The RBA/APRA has sensibly flagged that it may increase the interest rate buffer on new mortgages – from say 2% to 3% – as part of its macro-prudential toolkit, which would obviously mean less housing lending and less profits for debt sellers like Aussie John.

A major benefit of such macro-prudential measures is that they could be introduced immediately. By contrast, fundamental reforms to the supply-side of the housing market, while clearly needed, are a longer-term reform, requiring agreement between federal, state and local governments. Hence, they would be too slow to dampen this housing cycle.

Finally, where is Aussie John’s discussion of Australia’s perverse tax incentives, such as negative gearing, which encourages too much housing speculation and crowds-out first home buyers? Late last year on ABC’s Q&A program, Aussie John agreed that negative gearing was inherently flawed:

“Negative gearing wasn’t designed for people who could afford to buy $1 million-plus houses or apartments to offset the bulk of their interest payments off their tax. So negative gearing does need to be looked at in the tax system because I don’t think it’s fair at the moment. I think it leans very heavily to the high income earners, and that needs to be brought into line…”

Back in January, Symonds also claimed that negative gearing “favoured investors and was distorting the property market”, and that it needed “a total overhaul to make it fairer… [because] first home buyers have no hope of getting into home ownership these days unless they’re helped by their families”.

Where is such logic now?

No Aussie John, it is defective government policy – on both the demand and supply-sides – that are the primary cause of Australia’s housing problems. It’s not that hard to acknowledge, is it?