Some interesting speculation about corporate action is growing around the iron juniors. Last week, Cliffs’ Australian assets shifted into play. That’s 11-12 million tonnes per annum (mtpa) that’s on the market:

In a statement, 5.2 per cent shareholder Casablanca said all six of its nominees had been elected to Cliffs’ 11-member board at the company’s annual meeting in Cleveland. Casablanca based its victory declaration on an estimate by its proxy adviser, according to a Bloomberg report.

…Casablanca campaigned for Cliffs to sell its non-US assets, and players such as Mineral Resources are likely to express an interest in the Koolyanobbing operation. It remains unclear how quickly Casablanca would embark on a sales process given the depressed asset valuations in the iron ore space.

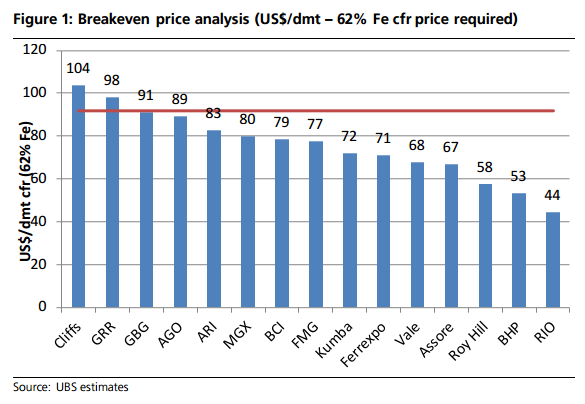

Here, again, is the UBS graded discounted break even chart:

We know as well that Gindalbie is being eaten by Ansteel owing to the specifics of their equity arrangement:

Gindalbie Metals (GBG) last night suspended trading in its shares as it awaits the outcome of a review of the value of its shareholding in the Karara iron ore project, which is a joint venture with China’s Ansteel.

…The Chinese company is already on track to earn more than a 60 per cent interest in the project, as Gindalbie has had to rely on the Chinese steel giant to offer further financial support to meet its share of debt repayments on the joint venture project.

Now, we get an interesting little article from Bloomie about Atlas:

“Someone could buy them for the port or someone could buy them for the assets,” James Wilson, an analyst at Morgans Financial Ltd…Atlas, based in Perth, may appeal to suitors including Chinese steelmakers prepared to build a more cost-efficient rail link to the port…

“Baosteel has gone and paid a lot of money for Aquila, for what looks to be a larger but less attractive iron ore deposit than that which Atlas Iron is busy uncovering at Corunna Downs,” Matthew Hope, an analyst at Credit Suisse in Sydney, said in a phone interview.

Any buyer of Atlas, which hauls its ore to the coast in trucks, could boost profitability by lowering transport costs, said Hope at Credit Suisse. Port and trucking charges are as much as five times higher than similar costs for larger producers, he said.

…Trent Barnett, head of research at Hartleys Ltd. in Perth, said by phone. “But you have to be pretty confident in iron ore prices.”

As I’ve noted before, the Baosteel West Pilbara play is nuts. But it’s timing is a salient lesson for other potential suitors. It’s moved far too early. The bottom of this cycle is 2-3 years away as the majors pour on the supply deluge. My advice to anyone looking at Pilbara assets of any sort is wait, wait then wait some more. They’re going to get a lot cheaper.