Business Spectator’s Adam Carr has fired another shot across the bow of us ‘doomsayers’ who believe that the unwinding of the biggest commodity price and mining investment booms in the nation’s history will cause income growth to decline and weigh on living standards. Instead Carr argues that recent weak wages growth is all because of a “crisis of confidence”:

According to the UN, Australia currently enjoys an extremely high standard of living…

On the income side, Australia actually scores very well… A decade ago 12 of the top countries’ GNI per capita was indistinguishable. Looked at that way, the fact is, Australia’s rank — just on income per capita — hasn’t really changed all that much over the past two decades. Nor has our overall score on the HDI I might add (at number 2).

That consistency is actually a very important point. If that ranking has been consistent over time — a few decades — then it can’t be true to say that the mining boom has been responsible for any significant lift in the nation’s standard of living. That being the case, it must hold that the end of the mining boom — if that even is a reasonable scenario — won’t bring with it any material decline.

Against that backdrop we shouldn’t worry about a modest decline in wage growth. Wage growth is not low because of weak economic growth, or because the mining boom is over, or that the labour market is weak…

Wage growth is soft because of Australia’s crisis of confidence… National income, and the outlook for, is otherwise very good.

Carr’s claim that “it can’t be true to say that the mining boom has been responsible for any significant lift in the nation’s standard of living” and that “it must hold that the end of the mining boom… won’t bring with it any material decline” is frankly ridiculous and not supported by the data.

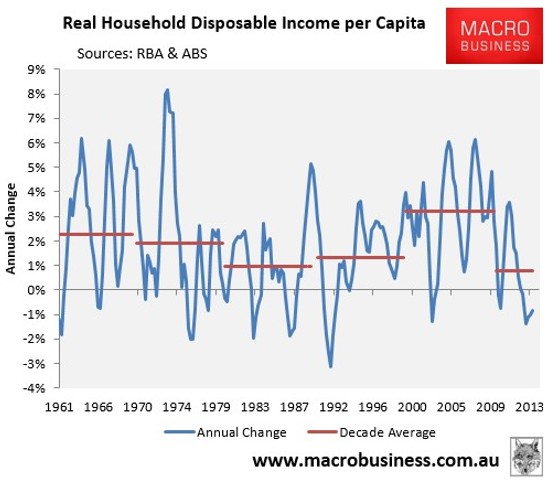

As shown in the next chart, the 2000s saw the highest growth in real per capita household disposable income (HDI) in at least 50 years, with household incomes growing by an extraordinary 3.2% average annual rate over the decade, well above the 2.3% average growth in household incomes experienced over the 1960s, the 1.9% average rate of the 1970s, the 1.0% average rate of the 1980s, or the 1.3% average growth rate experienced over the 1990s:

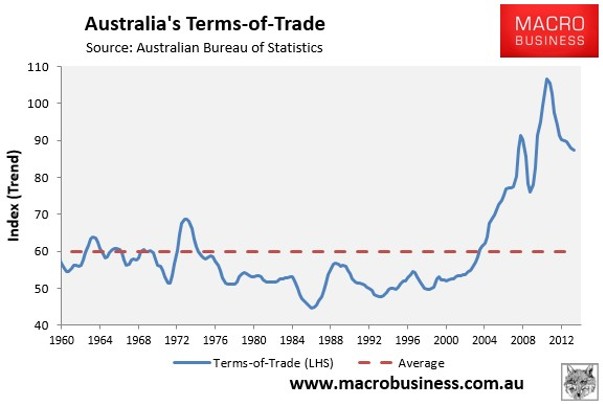

The key, of course, behind this rapid income growth was the extraordinary surge in the terms-of-trade between 2003 and 2011, shown in the next chart:

The terms-of-trade has been falling since 2011 on the back of falling commodity prices – particularly iron ore, coal and gold. Not surprisingly, the growth in real per capita (HDI) has also slowed to just 0.8% between March 2010 and March 2014, which if maintained for the remainder of this decade would result in the slowest growth in incomes in at least 50 years.

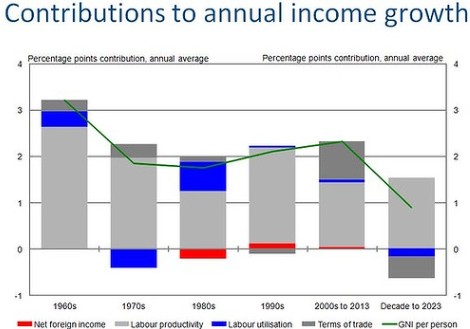

Indeed, the Australian Treasury expects such an outcome, forecasting that real per capita gross national income will slow to its slowest pace in at least 60 years in the decade to 2023, dragged down by the falling terms-of-trade (see next chart).

Only last night, Treasury Secretary, Martin Parkinson, said the following about the prospects for Australian income growth and living standards:

“If Australia gets the same productivity growth as its long-term average, then living standard growth will be about a third to a half of what the Australian public has gotten used to over the past 10 years”.

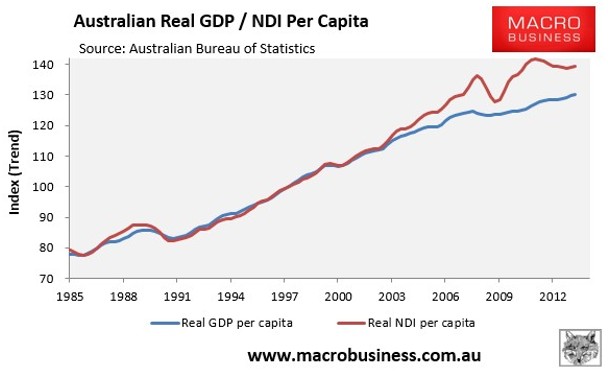

But the biggest condemnation of Carr’s arguments comes from the next chart showing how the epic terms-of-trade boom caused real per capita national disposable income (NDI) to grow by a whopping 26%, almost double that of real per capita GDP (+14%) between March 2003 and December 2011 (see next chart).

The simple truth is that these two lines need to, and will, reconnect. The process began after the terms-of-trade peaked in 2011 and has been declining ever since. This is now pulling down real per capita NDI, which has fallen by 1.9% since December 2011, versus growth in real per capita GDP of 2.4% over the same period.

Put simply, Australia’s standard of living was dramatically inflated by a huge ten year pay rise that was never earned. As commodity prices recede, so too will much of the income gains enjoyed over the 2000s along with the growth in living standards that we have all become accustomed to.