Iron ore junior Arrium reported today and is soaring nearly 10%. From Mac Bank:

- ARI reported FY14 underlying NPAT of $296m (Macquarie at $285m). Reported NPAT was $205m. It declared a 2H14 unfranked dividend of 3cps (in line with our estimate of 3cps).

- Mining EBIT of $481m was slightly ahead of our forecast EBIT of $469m. ARI has indicated that it is operating at a ~13Mtpa sales rate from 1Q13.

- Mining Consumables EBIT of $140m, was also slightly ahead of our $136m forecast. FY14 Australasia rail wheel volumes were down 46% on pcp and grinding media down 9% due to the Indonesia export tax. ARI has reported that Indonesia production is now ramping up, and that over FY14 it reduced its Newcastle headcount by ~20% (120 people) to realise annualised cost savings of $15m.

- Steel FY14 EBIT was -$53m, down from -$44m in FY13 and slightly worse than our -$45m forecast. ARI maintains that the division remains positive on a cash flow basis, but that cost reductions were more than offset by a 5% YoY decline in volumes. Recycling EBIT of $1m was in line with our estimates.

- Balance sheet better than our estimates, largely due to working capital declines, good asset sales and capex rationing in Mining. Positively, ARI has reduced net debt to A$1.7b, down $268m HoH. ARI realised $240m in asset sale proceeds over FY14. Capex in FY14 was $435m, below Management’s original guidance of $470m – $510m, with the biggest savings made in its Mining division ($199m spent vs $245m – $270m guidance). Working capital movements: Inventory decreased to $1,235m (from $1,333m at 1H14 and $1,281m at 2H13), payables increased from $1,031m at 1H14 to $1,175m at 2H14 and 2H14 receivables were $627m (down from $721m at 2H13 and up from $594m at 1H14). The net HoH benefit in working capital movements was thus ~$208m.

- Outlook commentary. No quantitative earnings guidance has been provided. ARI has provided FY15 capex guidance of $390m – $450m, and is targeting additional FY15 asset sales of ~$100m. It states that it is on track to increase iron ore sales to a 13Mtpa run rate in 1Q15. FY15 mining consumables volumes are expected to increase due to a ramp-up in Indonesia sales.

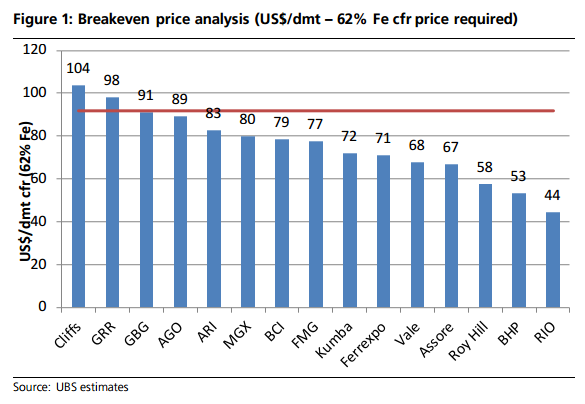

No guidance because, frankly, it’s the walking dead:

Advertisement

Having said that, it’s a much better buy for an enterprising Chinese or Korean steel mill than Atlas. Rebar futures are weak in China today. Iron ore futures flat.