This morning The Australian is reporting (or thinks it is) that:

… in a declaration largely lost amid BHP’s plans for a $US14bn spin-out of non-core assets, the world’s biggest miner says it is looking to expand its Pilbara iron ore mines and ports to annual capacity of 290 million tonnes a year.

This is up from a previous target to grow to 270 million tonnes and at a forecast capital cost that is dramatically lower than guidance given to analysts a year ago.

“We would say it is quite unlikely that we would see prices north of $US100 a tonne, so our forecasts are obviously based on something below that,” Mr Mackenzie told British media when asked if there might be a price floor around current price levels.

This is not reporting anything new. In fact, it’s not really reporting at all. It’s channeling BHP’s PR strategy, which is an integral part of its business plan. BHP is furiously talking down the iron ore price to ensure all of its little competitors struggle to raise capital. It’s all a part of the big two’s plan to restore their supply share dominance.

Meanwhile, at the Australian Financial Review, which is part-owned by aspiring iron ore junior Gina Rinehart, neither the BHP story nor the collapsing iron ore price registers as newsworthy at all. Ain’t no iron ore problem here!

There need not be any conspiracy. The weight of ownership exercises its own moral suasion, as decades of Murdoch “non-interference has proven handsomely.

At Business Spectator, Alan Kohler sticks his hand in the PR blender and gets slashed to pieces:

BHP Billiton and Rio Tinto are in a fight to the death with Chinese iron ore producers, the latest manifestation of which is BHP chief executive Andrew Mackenzie’s weekend declaration that he will dramatically expand Pilbara production.

Growth in Chinese demand for iron ore is slowing — from 9 per cent last year to 5 per cent this year — and the profitability of China’s steel mills has collapsed. China’s iron ore miners are also underwater. Research house GaveKal Dragonomics estimates the average cost of production of the Chinese miners at $US125 per tonne. The spot import price is currently at $US91.90.

…Says Michael Komesaroff of GaveKal: “The basic reason seems to be that this time, Chinese mine-owners know that if they shut down, it will not be just for a few months but forever. With their backs to the wall, Chinese miners are looking for any way possible to keep operating for just a while longer.”

…But if, or perhaps when, they eventually close, the price will go well above $US100 a tonne and stay there.

Christ, where do I start:

- Chinese steel mills margins are very good right now but demand stinks

- the iron ore major’s war is with all other producers not just Chinese, most obviously Australia’s juniors

- the spot iron ore price is $90.10

- some Chinese mines will close but the protection will continue

- the price forecast is laughable, even if the major’s win, the best case outcome is $80 with the FMG the marginal cost producer

Meanwhile, as the iron ore price collapses once more, Fortescue is undertaking its own PR push to ensure it’s not seen as the next domino with Nev Power turning up at AFRTV and across the metros arguing higher prices are coming (with Godot). And Andrew Forrest scored himself another panegyric, this time at the usually more skeptical Financial Times.

These misinformation campaigns appear to be having some effect. Despite what is a patently weak iron ore price with much worse to come ($70 by this time next year I reckon), “analysts” are on the hustings looking to pick bottoms. At Seeking Alpha, one brave soul likes Atlas Iron:

Atlas Iron (OTC:ATLGF) has announced it is taking additional steps to reduce the outflowof cash from its treasury. Atlas is planning to sell some non-core tenements and to relinquish other tenements and the company expects this will save the company approximately $10M per year in annual expenditures which would have been needed to spend to keep those properties in good standing. Another good plan is to sub-lease office space, but this will obviously have a much lower impact than relinquishing some tenements.

This announcement comes shortly after a previous announcement whereby Atlas Iron announced it was selling its interest in Shaw River Manganese as Atlas Iron is falling back onto its core iron ore tenements. Additionally, the company is hinting at a $25M impairment charge on other investments as it is now planning to adopt a mark-to-market valuation for its interest in Centaurus Metals (OTC:CTTZF) which has iron ore operations in Brazil.

I think it’s good to see Atlas Iron is rationalizing its portfolio and it generally is a good idea to scrape some fat off the corporate structure, and giving up uninteresting tenements and sub-leasing office space is a good move. However, the company needs to make sure it doesn’t limit its options in the future. I can understand the need to sell its stake in Shaw River Manganese, but I would like the company to hold onto its stake in Centaurus Metals as it would diversify Atlas Iron’s country exposure. That being said, I would still prefer to hold Fortescue Metals (OTCPK:FSUMF) as exposure to lower-grade iron ore.

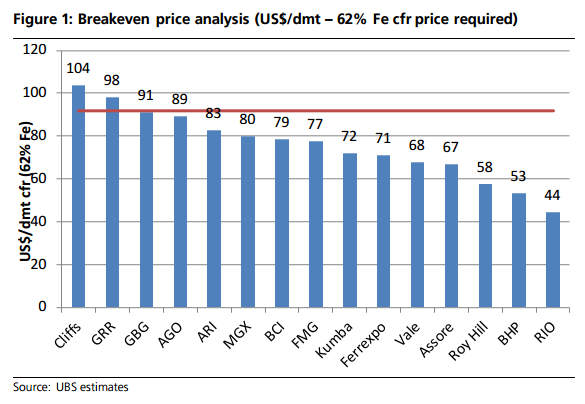

Limit its options in the future…jeez…it has no future. Here is the UBS grade discounted break even chart for miners:

AGO’s business model is caput. You prefer FMG? Try Motley Fool where apparently Fortescue is starting to look “interesting”. Sure it is, in-so-far-as it’s in the fight of its short life for survival.

FMG has got strengths and weaknesses. Management knows how precarious its position is which is why it’s racing to pay down debt and squeeze costs all over.

Against it is the forthcoming $70 iron ore price and a failing RBA which has propped up the dollar with its housing bubble ensuring that FMG can’t catch down to Kumba, Ferrexpo and Vale on the cost curve. Thanks Glenn!

PR or not, MMX of Brazil shows what is coming to the Pilbara in the next twelve months as it restructures into the abyss:

The Brazilian market reacted negatively to MMX’s decision to review its iron ore business plan and halt production at its Serra Azul unit.

The value of MMX’s common shares – called MMXM3 – fell by 8.5% on the São Paulo stock exchange on Tuesday August 20, before declining by a further 3.1% on Thursday August 21 to trade at 0.94 Reais ($0.41).

The Brazilian miner announced Tuesday that it will once again revise its iron ore business plan.

With this move, it aims to “prioritise the initiatives for cash generation, taking into account the current market conditions, the company’s short- and mid-term cash needs and the economic and financial perspective of its business model”.

But Goldman Sachs analyst Marcelo Aguiar believes that MMX’s balance sheet risk continues to get worse…

You may or may not agree that any of the Australian producers are going to go under but it’s clear that the press will be the last place to look to find out.