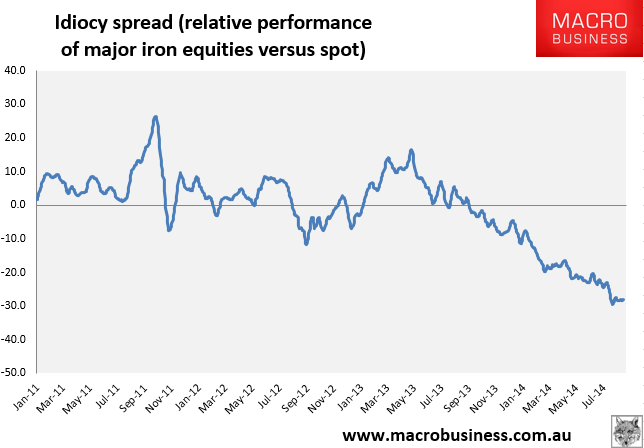

There’s no acknowledgement as usual but it’s clear from Roger Montogmery’s latest post that he is familiar with the “idiocy spread”:

We are following, with great interest, the discussion currently unfolding in the market about iron ore and the big miners.

On the one hand, we have the spriukers calling for a ‘rotation’ out of banks and into the big miners. The logic is no more sophisticated than saying: “You should sell the banks and buy the miners because the banks have gone up a lot and the miners have gone down a lot, so it’s now time for the miners to go up a lot”.

On the other hand, we have those that believe the risks for the iron ore price are to the downside because supply is building and demand growth is slowing. This latter view is also held by Montgomery. We note that tougher credit conditions continue to impact iron ore prices, with some trading firms discovering it’s increasingly difficult to secure letters of credit from banks. This comes as the government attempts to consolidate industries where overcapacity exists, by reining in lending and attempting to avoid future bad debts.

In any case, if there’s one type of business that we are loath to own at Montgomery, it is the one that cannot increase or even maintain the price of its product in the face of excess supply. By definition, mining companies are not the prized businesses that can take large amounts of equity capital on which they can subsequently generate high rates of return.

For now however, the band is playing, the music is loud and the cheap money is flowing. The party is in full swing. It is no surprise then that the shares of the big miners have not followed the iron ore price lower, but revelers would be wise to dance close to the exits.

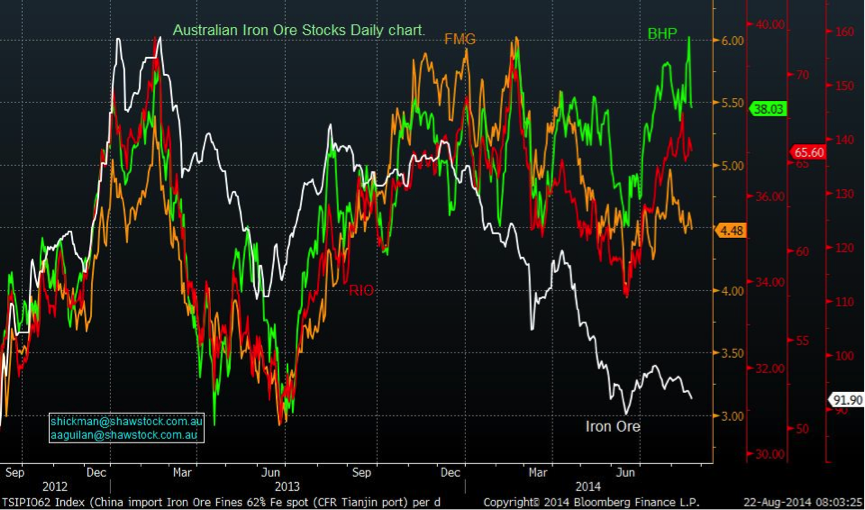

A Bloomberg chart doing the rounds at the moment is this one from our friends at Shaw Stockbroking.

But short-term factors are, by definition, ephemeral; and our long-term view of iron ore is that the prices obtained during the three decades prior to 2004 ($10–$20/t) are just as valid as the prices traded in the decade from 2004 to today ($20–$187/t). Of course, nobody is expecting prices to fall to anywhere near $20/t, last of all the chartists (but more about them in a moment). Humans however, are notoriously poor at doing anything other than expecting the future will look like the recent past. If the price of iron ore has been between $187/t and $87/t in the last few years, why should next year be any different?

The chartists believe that support for iron ore at $89–$90/t should hold. The only problem of course is Chinese steel mills and construction companies aren’t making their buying decisions based on the support line drawn on this chart.

As we have warned for some years, credit growth is slowing in China, and demand for iron ore is expected to do likewise.

Whether or not the price of BHP, RIO and FMG follow in the short-term is anyone’s guess, but the fundamentals don’t provide investors with the kind of risk profile we would be comfortable with. Those looking for reliable dividend yields should be looking elsewhere.

Here is the idiocy spread in all of its group think glory:

Good to see RM on board.