Don’t know if anyone is buying but roughly 12 million tonnes per annum of formerly profitable Australian iron ore mines is on the chopping block, the WSJ reports in an interview with Cliffs new CEO Lourenco Goncalves:

Iron ore is the main ingredient in the making of steel, and Cliffs’s U.S. mines have benefited from the resurgence of the Detroit auto industry, drill-pipe demand for natural gas wells, and their geographical advantage over iron ore superpowers Brazil and Australia.

Other Cliffs assets, such as coal mines in the U.S., iron ore assets in Australia and Canada and a suspended chromite project in Canada, have been less profitable.

…In an interview, Mr. Goncalves said he would treat those less-profitable assets as “noncore” and seek to turn them around while entertaining offers to sell.

“If somebody offered me a train of money for the U.S. iron ore assets, I would not sell, because that is core” he said. “But if an asset’s noncore and you want to monetize the asset by selling, we’d sell for the best bid as long as the best bid meets the criteria for what we think the asset is worth.” The first priority would be to make all divisions profitable, he added.

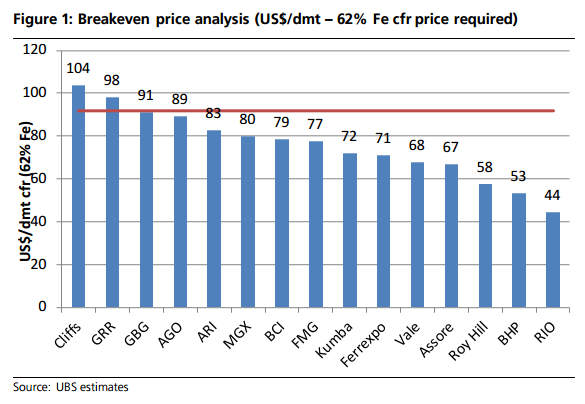

Let’s take that as a declaration of a fire sale and good luck because the assets are worthless. Here’s the UBS grade discounted break even chart:

Given Alan Kohler reckons iron ore will move back above $100 is due course, he should make an offer.