The great corporate struggle of our time (totally unreported of course) has opened a new chapter. Nev Power has dropped the friendly demeanor and intimated at the Diggers and Dealers conference that the big miner is now if full controlled panic mode (if you’ll pardon the oxymoron) aiming to pay down debt “as fast as we can do it”. From the AFRand Creamer’s:

“Over the next couple of years we are looking at paying another $2 billion to $2.5 billion off our debt and taking our gearing below 40 per cent or, in net debt to market equity rate, from about 95 per cent where it is today to under 50 per cent.

“We are focused on that target of getting our gearing below 40 per cent and the speed at which we get there will be determined by free cash flow from operations and the factors that determine that are obviously the iron ore price and secondly our cost structure.

…“We will look at that aggressive ramp-up in dividends based on how quickly we pay down debt. We see it as bringing the dividend up when the debt levels come down.”

…“We have a lot of flexibility in our balance sheet, and we are under no time pressure whatsoever. So we can bring forward a lot of the repayments, and can start at any time.”

Warning on hoped for dividend rises is time pressure. Indeed, the sobriety of these statements probably contributed to the the junior miners all being crushed yesterday despite iron ore futures taking off.

FMG’s actions betray a very obvious concern that the iron ore price is not coming back and that the time for motherhood statements is passed. This is a very real shift into public survival mode by the big miner and it is tempting to say it has a chance with the change in attitude. Except for one problem. It’s the marginal producer on the seaborne cost curve.

Nev Power also implicitly acknowledged this reality in discussing his options to reduce costs. From The Australian:

“Our first priority will be switching our power stations over to gas,” he said. “Then from there it will be a progressive changeover to gas through our mining fleet. Some of it will be as we replace that gear, as we buy new trucks we will buy trucks that run on gas, some of it will be converting of existing equipment.

“Unfortunately it’s not a quick process but we’re looking at this for the very long term from both a cost of that energy but also the emission footprint we can reduce.”

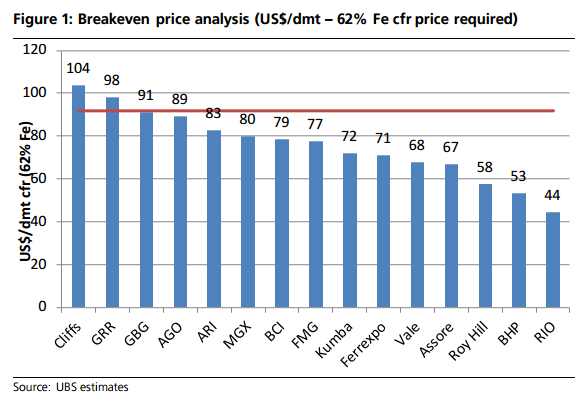

Our Nev reckons he can save $400 million by doing so. That’s $2.50 per tonne, more or less. Good work but still not enough. To survive, FMG not only needs to get its costs down, it needs to get them below 155 million tonnes per annum (mtpa) of production somewhere else. Here’s the cost curve courtesy of UBS:

The Australian juniors represent about 60mtpa between them. Kumba and Ferrexpo do roughly 40mtpa but they can also cut costs. Vale is beyond FMG’s reach unless the Aussie crashes against the real.

The coming capacity glut is 250-300mtpa for seaborne ore so that leaves Chinese mines to largely make up the 65% or more of of closures to bring the market into balance. Before that happens, all cost savings by FMG will simply get capitalised into lower prices.

It is right to be worried.