A couple of interesting asset allocation pieces today from the sell side. Citi reckons:

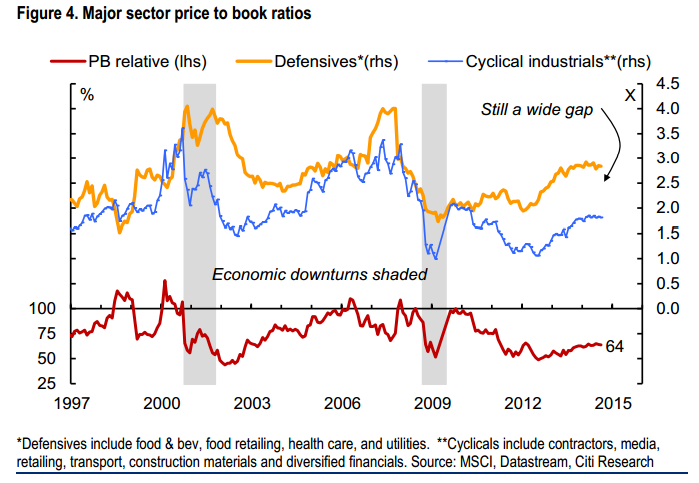

Mixed signals — With the economy having slowed to what seems only a moderate pace, but still hopes of a pick-up in the coming year or so, it’s challenging to identify the parts of the market that might do best. Adding to this is the narrow range of multiples across sectors, after the recovery in the market in recent years brought a convergence. Some valuation gap and scope for divergent performance seems possible between the banks and the miners, the former potentially lagging the latter now, but that doesn’t address the other half of the market, the industrials.

Wither growth? — Despite the patchy economy, the more cyclical industrial stocks have been the better performing in the past couple of years, at least until recent months. PE multiples are now closer to those of the defensive sectors, but price to book multiples are still more modest, and have commonly risen to much higher levels in previous cycles, as the stocks earned above average returns on equity in eventually buoyant conditions. But the uncertainty is how long it could take for growth to pick up to such extent and drive earnings and valuations up further.

Where’s resilience? — There have been a few more encouraging signs lately, with consumer sentiment and retail sales better, but subdued employment growth still leaves uncertain how well broader spending will offset the decline in resource investment. One response is to focus on industrial stocks in those areas where decent operating conditions are looking sustainable, which we see in residential property and capital markets in particular, and which should support stocks like FBU, BSL, HVN, and MGR, and AMP and MQG in our recommended portfolio.

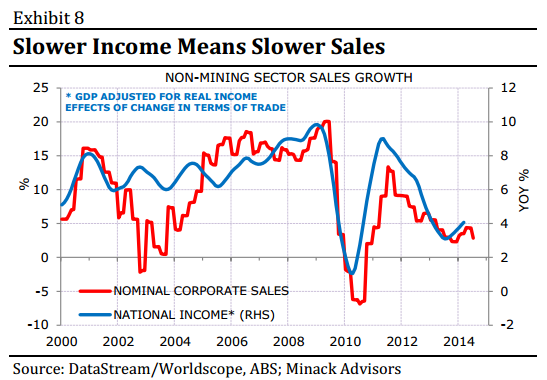

Any cycling back into resources will be temporary as firms and the market chew through super cycle excesses as well as the Chinese adjustment. There is no resilience in other cyclicals, either. As discussed many times already, income growth is lousy owing to the falling terms of trade so consumers are left hanging exclusively onto wealth effects, which they no longer fully believe in. Hence they are easily spooked.

This is why cyclicals are no place to be and will continue to fall short of previous cycle performances. The following chart from Gerard Minack says it all:

Advertisement

No sales, sorry! Citi’s rifle shot approach to housing-related stocks may work but that cycle is peaking and still pushing against one hell of a headwind.

Meanwhile, UBS sees the same landscape and concludes:

Advertisement

More Expensive Than It Looks?

The circa 17x industrial ex financial P/E multiple suggests the market at the stock level is more expensive than it appears at its headline overall valuation of 14.5x (due to lower P/Es for mining and financials). Low interest rates are likely buoying the valuation of the industrial portion of the market (as they are for financials) and in our view the prospect of a lower A$ also supports higher than average valuations. This note looks at the drivers of the high P/E by looking at stock level data.

Industrial Valuations Looking Full

Australian industrial valuations do look full in the context of history and versus global comps. Additionally, from a margin perspective there is not a clear case that industrial stocks are (on average) under-earning. This makes the market more reliant on the A$ coming down to help support some decent earnings growth. We retain our 5625 year end target and continue to favour beneficiaries of a lower A$. Favoured stocks include CSL and Resmed.

Yep, internationally exposed industrials, not resources, are still the only place to be. As the dollar falls, and it will, earnings will deliver.

Why will the dollar fall, I hear you ask? For that we turn to Credit Suisse via the SMH blog:

The recent pull-back provides an opportunity to cover your shorts in “higher beta stocks” like Bank of Queensland, write Credit Suisse strategists in their latest note which lists their best long and short ideas.

…“Our expectation of downside risk to Aussie bonds yields, even from here, also suggests it is prudent to tone down short positions in high yielding bond proxies like BOQ,” they write. They add in its place IAG.

That’s right – they reckon bond yields could continue to go down.

“Both our long and short positions have an average 2015 PE of 15x. However, our long positions provide a higher dividend yield (4.5% vs 3.9%) and free cash flow yield (6% vs 3.6%). In an environment of low or even falling bond yields we think our portfolio is well placed,” they write.

Below is their complete list of stocks they reckon will go up (long ideas) and stocks they think will go south (short ideas).

Advertisement

Their stock selection sucks, if I may say so, even though the framework is right. Bond rates will fall as domestic activity continues to disappoint and the RBA is forced to cut again, pushing down the dollar.

I’ve been explaining these asset allocation ideas since late 2011. All of this was spelled out again in February this year in the members special report Asset allocation in era of Dutch disease. It is going exactly to script.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

The recent pull-back provides an opportunity to cover your shorts in “higher beta stocks” like Bank of Queensland, write Credit Suisse strategists in their latest note which lists their best long and short ideas.