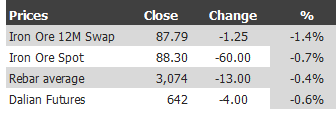

Here are the iron ore charts for August 27, 2014:

Paper market weakness returned with a vengeance with new lows on everything. Physical is worse. The iron ore contango is gone and steel prices are now in free fall. Fresh CISA fast data has large steel mills increasing production in the mid August period 0.5% to reach 1.83 million tonnes. It seems to be largely going towards increased inventories with CISA also reporting that mill stockpiles were at 15.25 million tonnes as of Aug. 20, up from 14.57 million tonnes ten days earlier. That’ll keep weighing on steel prices, thanks very much.

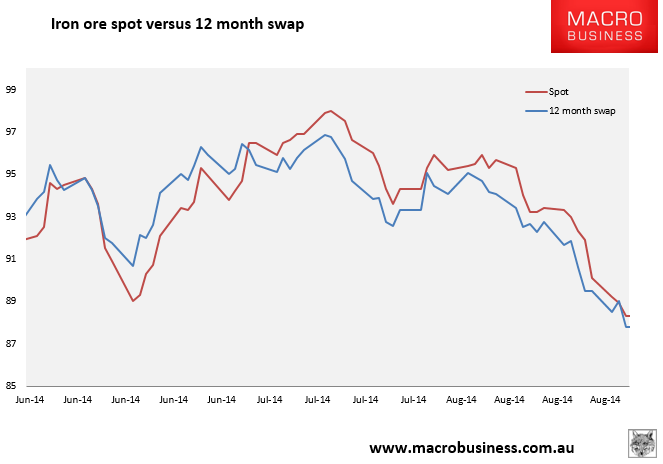

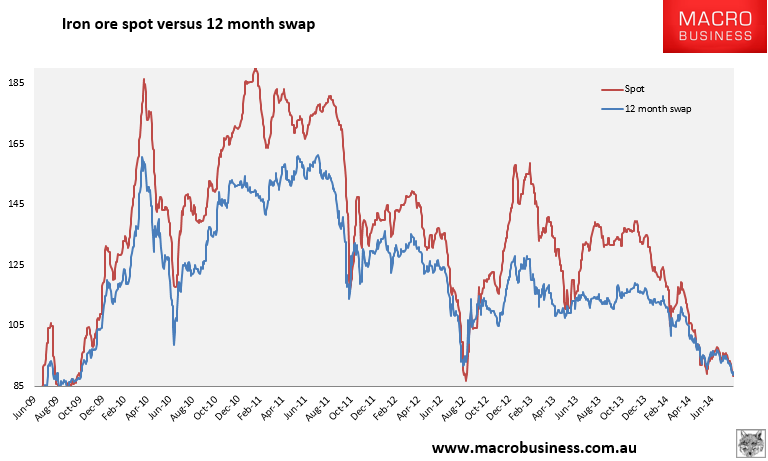

We could be clearing the decks for a capitulation in iron ore and look very likely to take out the post-GFC low of $86.70, hence the long term bonus chart above today. Texture from Reuters:

Many Chinese steel mills are buying iron ore only in small quantities to meet immediate needs and they prefer the cheaper stocks lying in China’s ports against fresh seaborne cargoes, said an iron ore trader in Tianjin.

“Mills and end-users are pushing prices down because the economic outlook is not optimistic. Credit is also tighter and I expect iron ore to drop further to between $80 and $85,” he said.

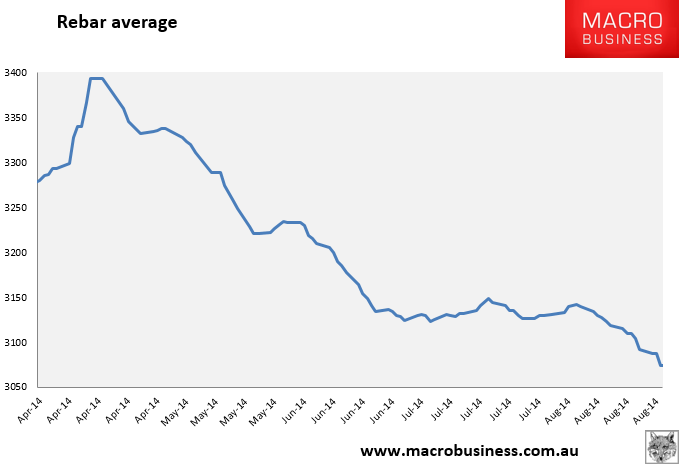

…Spot steel prices in China have also been declining, with billet in the key Tangshan area dropping by 70 yuan a tonne since the weekend to stand at 2,560 yuan on Tuesday, Standard Bank said in a note.

I can only repeat, this weakness no longer looks cyclical to me, it’s structural oversupply and, unless Chinese housing turns around fast, the restock when it comes will be weaker than hoped and hit lower peaks than previous rebounds. This appears to be the next shunt lower in the entire steel/iron ore price deck.

Some good news from India:

After losing its status as the third-largest exporter of iron orea couple of years ago, India is likely to turn a big importer of the key steel-making raw material by the end of this financial year. The country is likely to import 10 million tonnes (mt) in FY15, three times its previous record, 3 mt, in 2012-13.

Unstable domestic production, increase in royalty rates and lower prices in the global market would contribute towards increasing imports. Domestic production has been steadily declining from a high of 220 mt in 2009-10 to 150 mt in FY14.

That volume is roughly what I expect but does not appear to be a net figure. Goan iron ore is going to return to seaborne markets in 2015, some 10-20 million tonnes of it, so the net trade figure will be neutral or still positive.