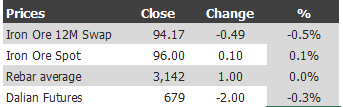

Here are the iron ore charts for August 7, 2014:

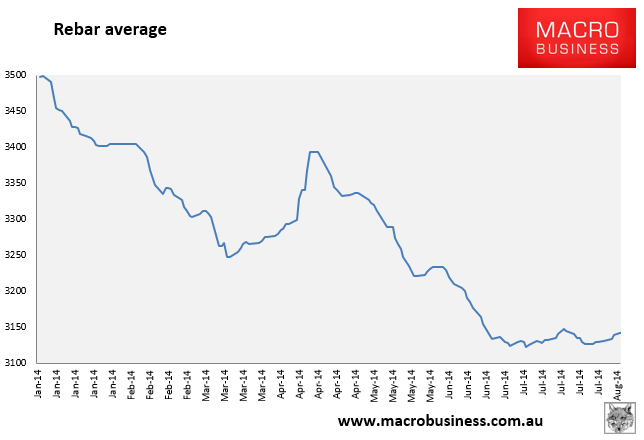

More dancing on the the pin head in paper and physical markets, including rebar futures and BDI cape.

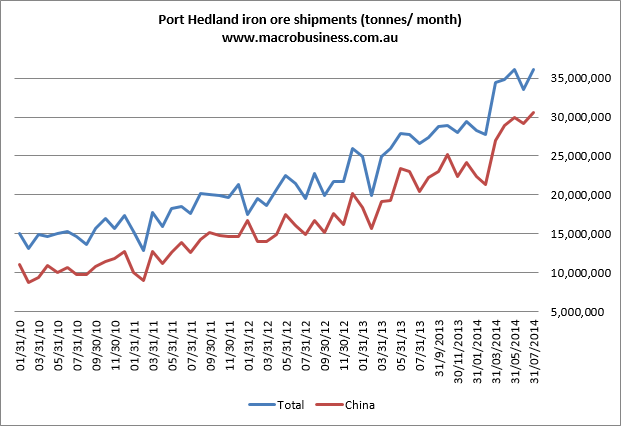

Port Headland shipments for July are out and rebounded to a record at 36.08 million tonnes:

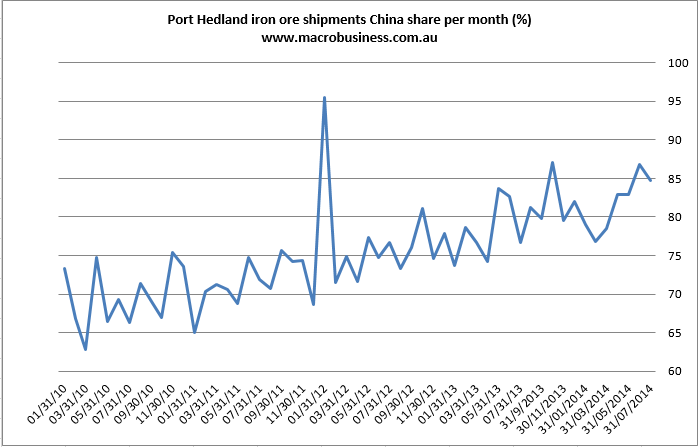

The China share fell slightly:

Capacity appears to be maxed out for now. In the wider markets Reuters has texture:

“I think the downside risk isn’t too much at this point. The market has a better chance to go to $100 than go back to $90,” said an iron ore trader in Shanghai whose company has 700,000 tonnes of Australian cargoes arriving from September to November.

“The challenge would be finding the right time to sell,” he said, acknowledging that supplies of immediate cargoes remain brisk.

Some Chinese mills still prefer to buy from iron ore stocks sitting at the ports that are $2-$3 a tonne cheaper versus fresh sea-borne cargoes, he said.

Sounds about right given the obvious equilibrium. Not long term, though, from Vale:

Brazilian mining company Vale SA plans to double its iron ore exports to China within five years, Jose Carlos Martins, the company’s head of ferrous metals, told reporters on Thursday.

Mid next year and then again at the end of the year are next two tidal waves of supply.