This morning our magnificent business daily ran with the headline that “coal always wins” delivered directly from Peabody Coal:

Peabody Energy chief executive Greg Boyce is calling on coal producers to spend more time and money fighting “symbolic” movements against the industry and is confident China will not adopt a cap on carbon emissions.

As the anti-coal collective gathers more mainstream backers, St Louis-based Mr Boyce says the industry needs to do more to counter the attacks, particularly the global fossil fuels divestment campaign.

But he is confident that “coal always wins out”…Mr Boyce is bullish on the future for coal exports, saying China will not adopt a carbon emissions cap, despite growing speculation that Beijing could enforce one.

…But Mr Boyce said that though China was working to reduce its carbon intensity per unit of GDP, a cap on carbon emissions was “just not on the cards”.

Asked to comment on the Boyce remarks, Garnaut replied to MB:

Advertisement

“I recognize that my published analysis since 2011 has not been welcomed by corporate leaders in the coal industry. Regrettably, in economics as in physics, facts do not go away simply because corporate leaders don’t like them. I have simply been working through the changes that have been occurring in Chinese economic policy and structure since 2011. Shareholders in coal companies whose leaders have taken this work seriously are now richer than shareholders in coal businesses whose leaders have closed their eyes”.

Mr Boyce might also like to refer to a note by Citi today:

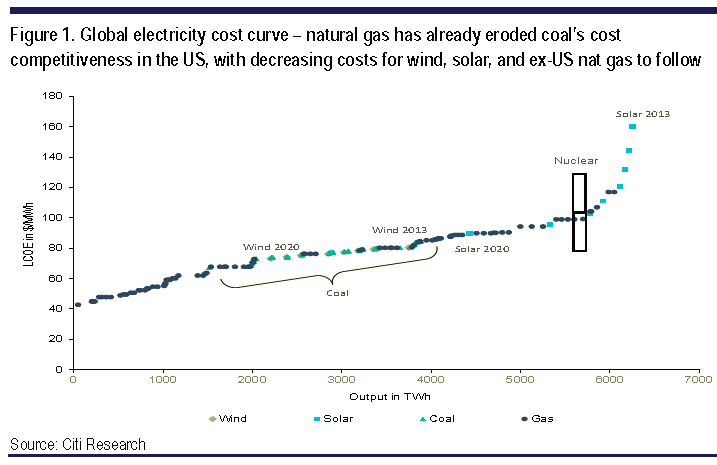

A key development with significant implications for Australia is the structural decline in coal demand growth. According to our commodity analysts, this structural shift is being driven by two main factors: environmental regulation, and increasing cost competitiveness of alternate resources.

Citi analyst Ivan Szpakowski, notes that “environmental pressures on coal consumption are rising not only in Europe and North America, but also in China and other emerging markets. The most significant change has been in China, where increasing regulations and the establishment of carbon markets promise to limit the attractiveness of coal power. Moreover, the country is aggressively pursuing an “everything but coal” development plan for the power sector, with rapid growth in capacity for alternative energy sources.

In North America and the European Union, the trend of increasing environmental restrictions is clear and the coming decade should see closures of coal power plants vastly exceed new builds.

The most significant blow so far to coal’s price competitiveness has been the shale revolution’s impact on US natural gas prices, which served to increase natural gas’s share of US power generation from 17% in 2003 to 27% in 2013. However, global power markets are likely to be increasingly impacted, first from US natural gas exports, and then by the growth of indigenous shale gas production overseas, with China, UK, Australia, Russia and Argentina the most promising markets.

Advertisement

I’d have been quite happy to have written off the lion’s share of Australia $70 billion in planned coal projects at this juncture were it not for the marked persistence of the massive Galilee Basin Adani project which is still lining up partners to go ahead. Even so, if it can raise the dough I’ll be very surprised. The project is immensely expensive and high on the cost curve and will add 60 million tonnes per annum to an already oversupplied seaborne market. Even the perennially optimistic Bureau of Resource and Energy Economics (BREE) can’t find enthusiasm for thermal coal prices, and it still expects Chinese demand to continue to grow at 2% per annum, and Indian at 4%. As the RBA noted just this week, we’re at the wrong end of the cost curve and mines will have to close:

The last word should perhaps go to Citi:

Advertisement

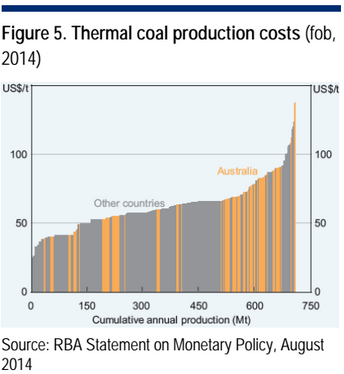

Our ESG analyst Elaine Prior (Global Energy Trends and ESG Implications) has observed that “the ‘rhetoric’ in Australia, and by the coal mining industry more broadly, tends to underestimate the pace of change (in energy markets).”…Australian producers enjoy relatively high quality thermal coal, but labour and production costs are high (Figure 5) and the infrastructure requirements (port andrail) associated with touted projects would be significant. Many of these projects would only be economic in our opinion if there were to be the very favourable combination of higher prices, cost containment and a lower AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.