The one question that nobody in the iron ore sector (or Australia more generally for that matter) dare ask is what if Chinese iron ore production does not close as Australian miners ramp up output. The reason nobody asks it is that the outcome will be calamitous. But it’s a very real question to pose, especially since the evidence too date supports that very outcome.

We should all recall that throughout the last few years every miner and his dog has argued that Chinese production will close down on mass from $120 downwards, giving birth the so-called “$120 price floor” notion. Well, we’re sub-$90 now and not only is iron ore production not not coming off, it’s still growing. From ANZ:

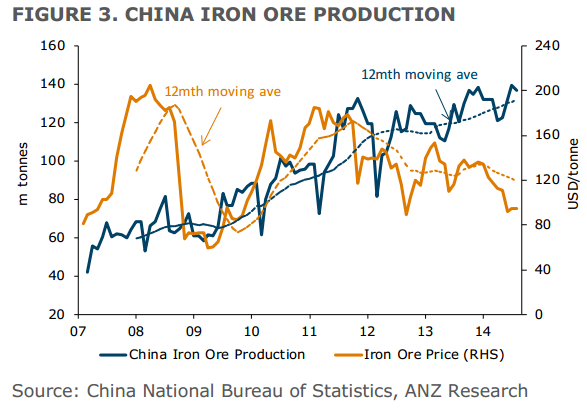

The supply-side factor that has surprised us the most has been the inelasticity of high cost Chinese iron ore supply to falling prices (Figure 3). Chinese iron ore production is up 10.4% year-to-date despite the weak price environment. This normally high cost price sensitive supply creates a high floor price for iron ore at around USD120/tonne.

Although there can be a 1-2 month lag in response, China iron ore supply has been stubbornly high all year, and combined with rising Australian iron ore exports, has created a major headwind for prices.

We think there are two structural issues at play which have driven this outcome and pushed the floor-price lower towards USD95-100/tonne:

1. Chinese producers appear to have lowered operating costs. The domestic coal industry has been actively consolidating in the past 3-4 years, generating increased supply and economies-of-scale cost savings. This directive is now being rolled out in the iron ore industry, which appears to be delivering similar cost savings in the order of 10-15%.

2. A good proportion of Chinese iron ore supply could indeed be unprofitable at current price levels, but remains open because of the vertically integrated structure of Chinese steel output. As much as 60-65% of iron ore supply is owned by steel mills that are currently operating at full capacity to generate enough cash flow to repay revolving credit lines and stay in business.

This looks unsustainable if credit conditions in the sector remain tight, and should usher in a supply closure of both high cost steel and iron ore supply in the coming months.

We think the current low price level around USD90/tonne is starting to bite. The recent preference for lump iron ore could be indicating an emerging shortage of domestic iron ore concentrate (effectively sintered low-value-in-use high cost iron ore supply).

That said, Chinese iron supply tends to peak in the third quarter, with much cooler weather in the fourth quarter inhibiting mining activity. As a result, prices are likely to stage a more visible recovery towards USD100/tonne later in the year, when seasonally lower domestic iron ore supply and high iron ore imports emerge.

The Chinese have long memories and plenty of reasons to hold a grudge against large Australian miners. Protection is easy, manifold in form and easy to hide. There is every reason to think that the Chinese will pursue it at length.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.