Prices cut as cost deflation and new supply outweigh healthy demand

We downgrade iron ore prices across our forecast horizon. Falling Chinese production costs, relentless growth in new cheap seaborne supply and slower growth in Chinese pig iron output relative to crude steel combine to weigh on the iron ore market even as Chinese and global steel demand is revised up. The supply curve is rationing expensive capacity out of the market, but new supply and falling costs mean iron ore prices will likely be lower than previously expected.

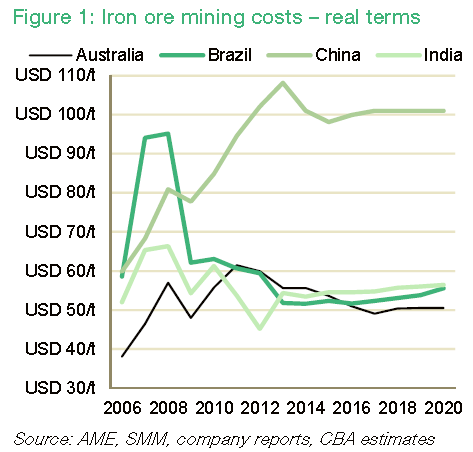

Chinese domestic (and Australian…) iron ore costs falling

Chinese domestic iron ore is the world’s marginal supplier, and therefore should be the marginal price-setter. We previously modelled China’s domestic iron ore sector as featuring median costs of ~USD105/t, with the marginal producer at around USD140-150/t and the cheapest Chinese supply around USD60-70/t (62% CFR China equivalent basis). We now understand Chinese iron ore mining costs are falling due to a range of factors. These cost cuts translate to a USD5-8/t reduction in costs and cost curve support for iron ore prices (Figure 1).

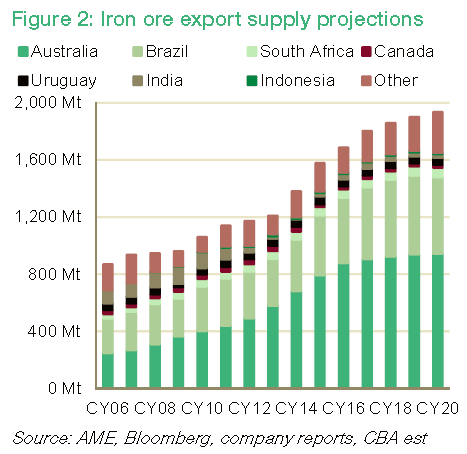

New cheap seaborne supply keeps commissioning

We update the timing and scale of supply in Australia and Brazil, including the start-up of Hancock Prospecting’s Roy Hill mine in 2H15, Anglo American’s Minas Rio project, and various excess run rates of the Rio Tinto, BHP Billiton and Fortescue Metals operations. There is plenty of new cheap seaborne supply arriving (Figure 2) that will likely displace expensive capacity and – as it happens – outweigh demand growth.

Pig iron output (and iron ore demand) lagging

China’s pig iron output has lagged crude steel output this year as diecast pig iron and some integrated steel mills in Hebei province shut on pollution concerns. Other provinces have increased output, but typically have fewer merchant pig iron mills and/or higher scrap ratios than the Hebei steel industry, resulting in weaker pig iron and iron ore demand. Chinese steel demand better despite property retrenchment

We upgrade 2014 China steel production growth to 4.7% (from 2%) and global crude steel output to 3.7% (from 2.5%), reflecting ongoing robust steel output driven by Chinese infrastructure investment and steel exports. Chinese property steel demand remains a risk for 2H14 but appears to be stabilising. We also upgrade medium-term world steel demand reflecting re-specification of our steel demand framework.

Implication: Cost deflation and new supply drag prices down

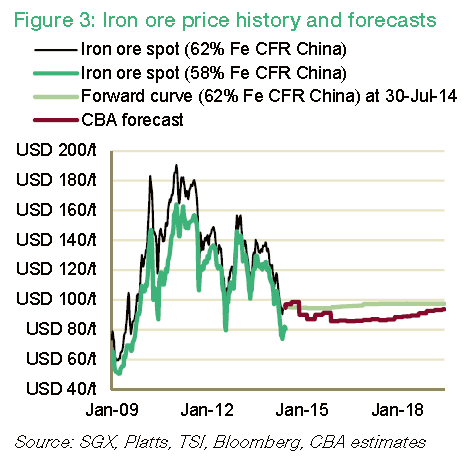

Miners around the world are commissioning new mines and reducing costs at existing mines. These forces should weigh more heavily on the market, leading to lower prices than previously anticipated, despite better demand. Prices are revised: -5% in FY15f, -12% in FY16f, -10% in FY17f and -4% in the long run to USD85/t CFR China, or USD73/t FOB Pilbara assuming USD2/t real freight costs (Figure 3, Tables 1-6).

Late to the party and still too far too bullish but a nice costs chart!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.