Repeat a lie often enough and it becomes true. This appears to be the approach taken by the Real Estate Institute of Australia (REIA), which has issued yet another warning that the removal of negative gearing would adversely harm Australia’s renters by creating rental shortages and driving-up rents. From Residential Property Manager:

REIA chief executive Amanda Lynch said the federal Treasury is again pushing for the removal of negative gearing and the rumour is that modelling will be done on retaining it for new housing only.

“This is a serious threat not only for our profession and geared investors but potentially for all property owners,” she said.

“Negative gearing increases investment supply with almost 1.9 million of Australians investing in the residential property market.

“The arrangement keeps rents lower than they otherwise would be,” she added.

The Hawke government abolished negative gearing for property in 1985, only to have it reinstated in 1987.

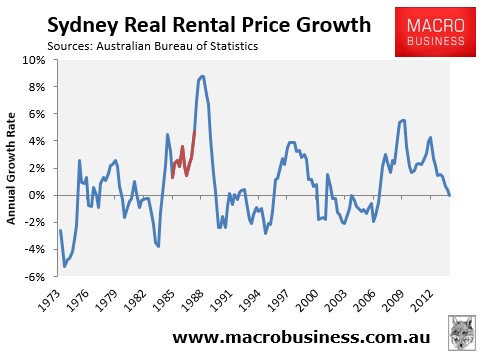

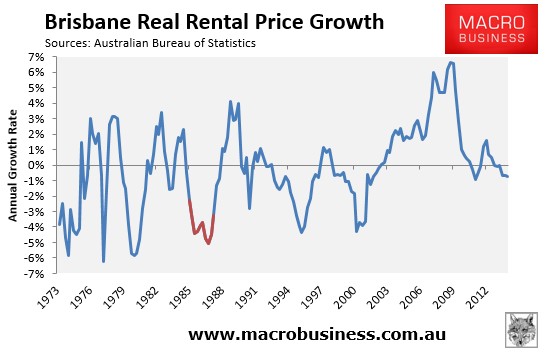

According to the REIA, during that period rents increased by 57.5 per cent in Sydney, by 38.2 per cent in Perth and by 32.0 per cent in Brisbane, highlighting the importance of upholding the arrangement…

“In the current tight rental market expectations are for outcomes similar to the mid-1980s,” Ms Lynch said

“The removal of negative gearing would increase demand for social housing, an area that governments have been struggling to address.”

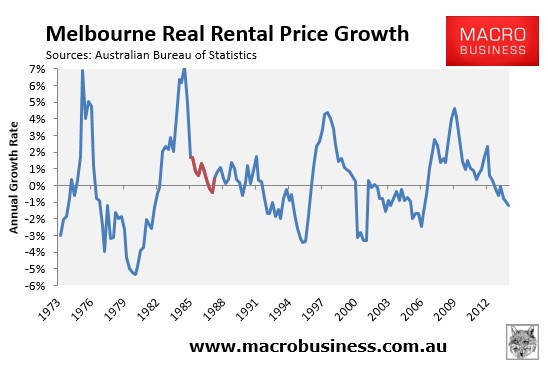

Once again, let’s use something called “evidence” to debunk the REIA’s claims that the quarantining of negative gearing between 1985 and 1987 pushed-up rents.

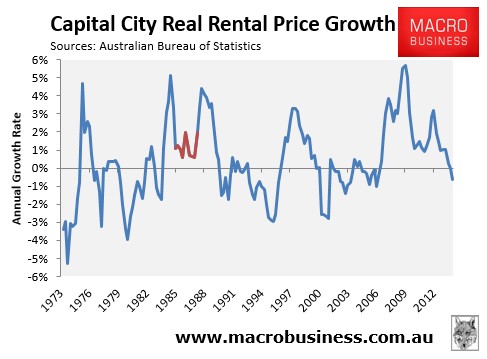

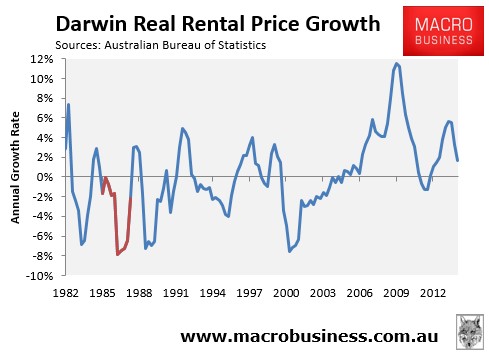

First, consider the below chart plotting the Australian Bureau of Statistics (ABS) rental series from 1972 in real (inflation-adjusted) terms, with the period where negative gearing losses were quarantined (i.e between June 1985 and September 1987) shown in red.

As you can see, there was nothing spectacular about this period, with periods of higher rental growth recorded both prior and subsequently.

Now let’s examine each capital city housing market to see whether the quarantining of negative gearing had any discernible impact on rents.

Now Melbourne:

Brisbane:

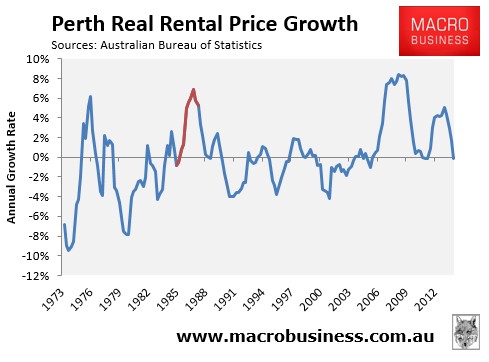

Perth:

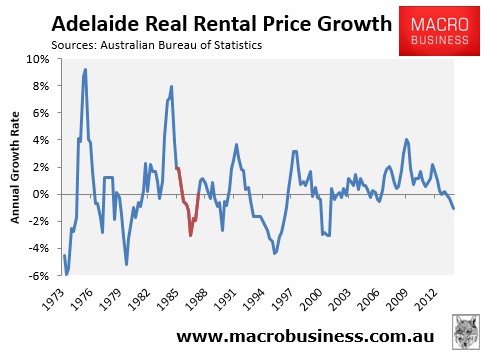

Adelaide:

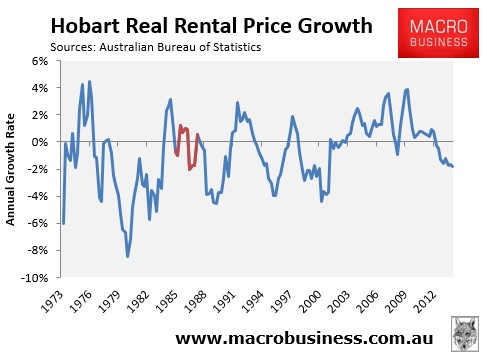

Hobart:

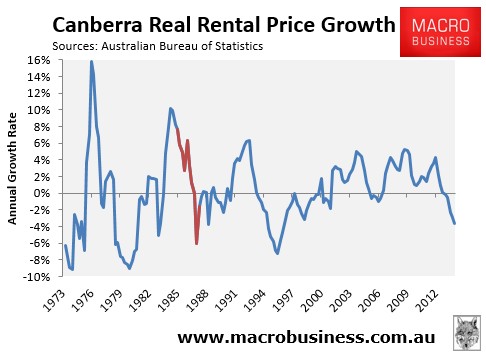

Canberra:

Darwin:

Again, anyone that claims that the quarantining of negative gearing between 1985 and 1987 pushed-up rents either doesn’t know what they are talking about, or is lying. The above charts illustrate, without a shadow of a doubt, that the Hawke Government’s decision to quarantine negative gearing had no discernible impact on rental growth, period.

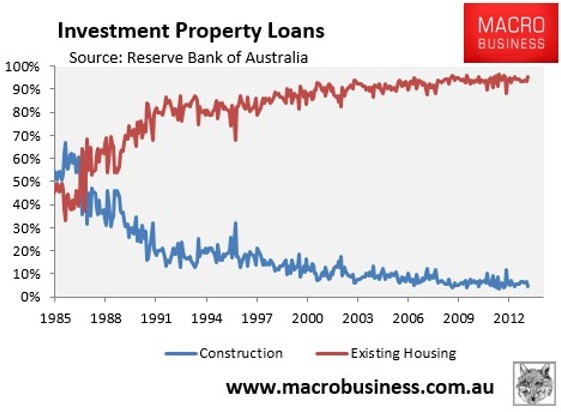

The REIA’s tacit assertion that negative gearing assists in the provision of rental accommodation is also highly spurious. An examination of of the RBA statistics shows that the overwhelming majority of investors – over 90% – invest in existing dwellings rather than construction, and that the proportion of investors constructing dwellings has fallen spectacularly since negative gearing was re-introduced in September 1987 (see next chart).

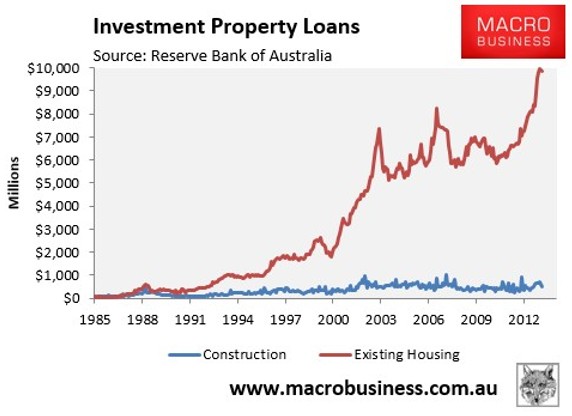

Moreover, the amount of investor funds going into new construction has barely shifted in 25 years:

Because investors primarily purchase existing dwellings, negative gearing in its current form simply substitutes homes for sale into homes for let. As such, negative gearing has done little to boost the overall supply of housing or improve rental supply or rental affordability.

In the event that negative gearing was quarantined so that losses could no longer be claimed against wage or salary income (as occurred between 1985 and 1987) and a proportion of investment properties were sold, who does the REIA think they would sell to? That’s right, renters (or other investors). In turn, those renters would be turned into owner-occupiers, thereby reducing the demand for rental properties, leaving the rental supply-demand balance unchanged.

Let’s also not forget that Australia is one of only a few nations that allow investors to deduct property losses against unrelated income. And yet we have one of the most unaffordable housing markets in the world and chronic supply problems (despite a massive land mass). What does this tell you about the efficacy of retaining negative gearing?

The evidence shows that negative gearing does little to boost supply, yet the additional demand from tax subsidised investors places upward pressure on home prices, locking-out first time buyers. This might help to explain why most other nations – many with more affordable rental accommodation than Australia – do not allow negative gearing.

Negative gearing also costs the government billions in lost tax revenue, which could be used to fund schools, hospitals, housing-related infrastructure, or any number of other worthwhile endeavours. It is pure and simple rent-seeking.