Find above an interesting video interview on The AFR with Lindsay David, author of the new book Australia Boom to Bust.

In the interview, David slams Australia’s record high mortgage debt (see next chart), claiming that “no one in the Western world has ever done what we are doing”.

He also claims The AFR article attached to the interview that the three pillars of the Australian economy: real estate, resources and the banks will eventually collapse:

He says that as Chinese authorities appreciate, they’ve built more houses and apartments than they need, demand for Australian ore will grind to a halt, triggering a weakness in the economy that will expose the banks.

“There are going to be more apartments than people in China and all of a sudden if [the construction] stops, then what is the floor on the spot price of iron ore? We don’t know what that is,” he said.

While I agree with David’s overall view on the Australian housing market – specifically concerns around its overvaluation and mortgage debt levels – as well as his view that the underlying pillars of the Australian economy are fragile, I strongly disagree with him that supply-side barriers have not played a role in increasing land/house prices, raising household debt, and increasing financial stability risks.

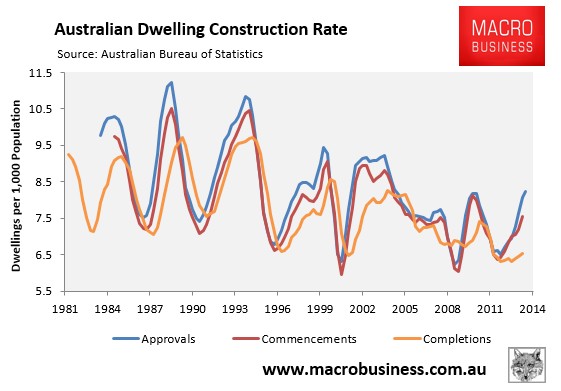

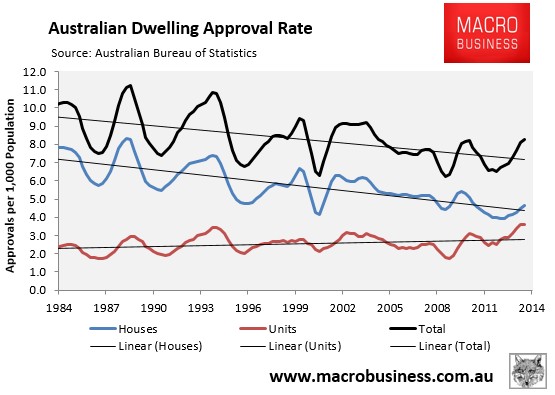

One only needs to look at the below charts showing the decline in housing construction rates over the past 20 years to see that housing supply has become less responsive to demand (price):

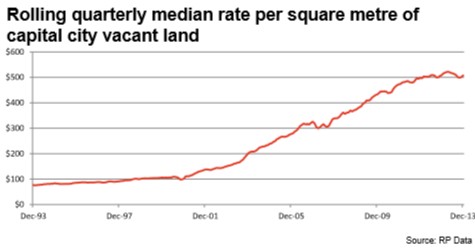

Alternatively, one could look at the huge escalation in fringe capital city land values, which is bona fide proof that supply-side barriers have become increasingly obstructive (see next chart).

Ultimately, however, unresponsive housing supply is a key determinant of price volatility, and tends to lead to bigger boom and bust cycles than in markets where land/housing supply is relatively responsive (elastic) to changes in price.

Miami, Florida, which David notes in the interview to debunk the whole supply-side argument, is a perfect case in point (see here).

unconventionaleconomist@hotmail.com