Standard & Poors (S&P) has released a new report warning of increasing risks for the Australian housing market due to rising investor participation, slowing income growth and softening employment prospects, which could create mortgage repayment pressures for recent, highly leveraged, purchasers:

All else being equal, falling interest rates have brought improvements to lending serviceability and, after a brief period of balance-sheet restoration, renewed lending demand, with Australian households–and investors especially–at the forefront. These easing conditions, coupled with seemingly unwavering confidence in Australian housing, have provided the backdrop for increased risk within Australia’s banking system, in our opinion…

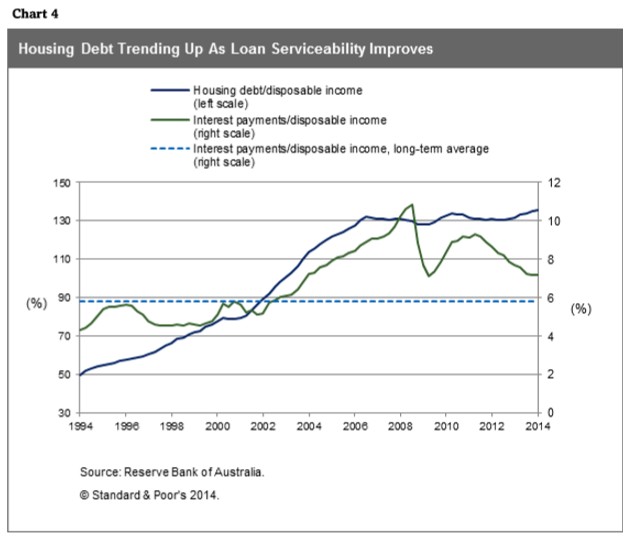

Loan serviceability has improved as a result of falling interest rates, yet remains some 20% above long-term averages (see chart 4)… At the same time, the number of those households entering the housing market with high levels of leverage (measured as a loan-to-valuation ratio of greater than 80%) remains reasonably high, at around 35%…

…we believe the strong residential property price inflation is likely to be translated by some households into a self-reinforcing feedback loop, pushing up demand on the back of increased leverage as a result of a cyclical low in interest rates–all against a backdrop of slower income growth. In our opinion, the risk is that mortgage repayments become an increasing problem for some households, particularly those recently entering the housing market, when interest rates begin to rise. A further shock to national income growth could also weigh on labour market conditions and add to the mortgage repayment pressures of some, in our opinion. We believe this could be transmitted through falling terms of trade, possibly bought about through a slowing China…

In our opinion, the more likely scenario involves a slowing in residential property price inflation as affordability pressures take hold, with something closer to national income growth. Even still, mortgage repayments for some recent market entrants will continue to absorb a significant proportion of disposable income, leaving them vulnerable to increased mortgage repayment pressures as a result of either rising interest rates or lower income growth…

Nevertheless, S&P believes that Australia’s banking system is well-placed to cope with any increase in mortgage defaults:

Advertisement

…we believe Australian banks are generally well placed to contend with higher risks, should they emerge, as they are well-capitalized by international standards, and, at present, enjoy a very good asset quality experience. Secondly, we expect these pressures that do emerge to be largely confined to recent market entrants… Further, Australian banks typically apply an interest rate buffer anywhere up to two percentage points as part of their underwriting, which should ensure many recent entrants are afforded some headroom to absorb a rising interest rate environment, although slowing income growth may negate this somewhat. Finally, loss given default levels are also expected to be tempered somewhat by mortgage insurance coverage, which is a common requirement for higher-leveraged exposures in Australia.

S&P do note, however, that any material increase in mortgage delinquencies, broad-based falls in property prices, and/or higher unemployment could result in negative ratings action for Australia’s banks.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.