The founder of Platinum Asset Management, billionaire investor Kerr Neilson, has released an interesting report warning about Australia’s frothy house price valuations and the risks of a correction once “conditions change, [and] a lot of the assumptions are found wanting”.

The report highlights four “facts” about Australian housing:

Advertisement

1. Returns from housing investment are often exaggerated and flattered by inflation.

2. Holding costs of rates, local taxes and repairs are estimated to absorb about half of current rental yields.

3. Long-term values are determined by affordability (wages + interest rates).

4. To be optimistic about residential property prices rising in general much faster than inflation is a supreme act of faith.

It then goes on to examine each of these facts.

On returns, the report notes that “the rise in the price of an average home in Australia…[has] been about 7% a year since 1986. In dollar terms, the average existing house has risen in value by 6.3 times over the last 27 years. No wonder most people love the housing market!”

But rental returns have gotten progressively poor:

Advertisement

…we earn a starting yield of say 4% on a rented-out home or if you live in it, the equivalent to what you do not have to pay in rent. But again, looking at the Bureau of Statistics numbers, they calculate that your annual outgoings on a property are around 2%. This takes the shape of repairs and maintenance, rates and taxes, and other fees. This therefore reduces your rental return to 2%, and what if it is vacant from time to time?

And the prospect for future solid capital growth is low due to poor affordability:

…the last 20 or so years has been exceptional. Australian wages have grown pretty consistently at just under 3% a year since 1994 – that is an increase of about 1% a year in real terms.

Affordability is what sets house prices and this has two components: what you earn and the cost of the monthly mortgage payment (interest rates).

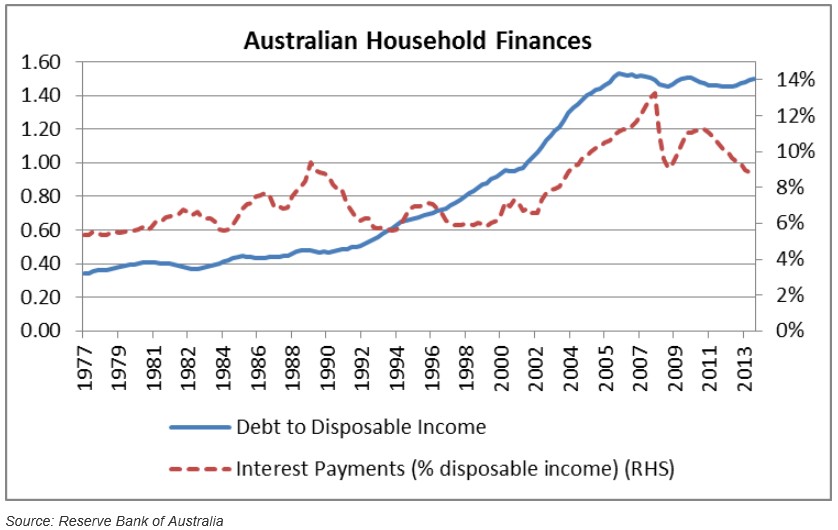

…even though interest rates have progressively dropped, interest payments today absorb 9% of the average income, having earlier been only 6% of disposable income.

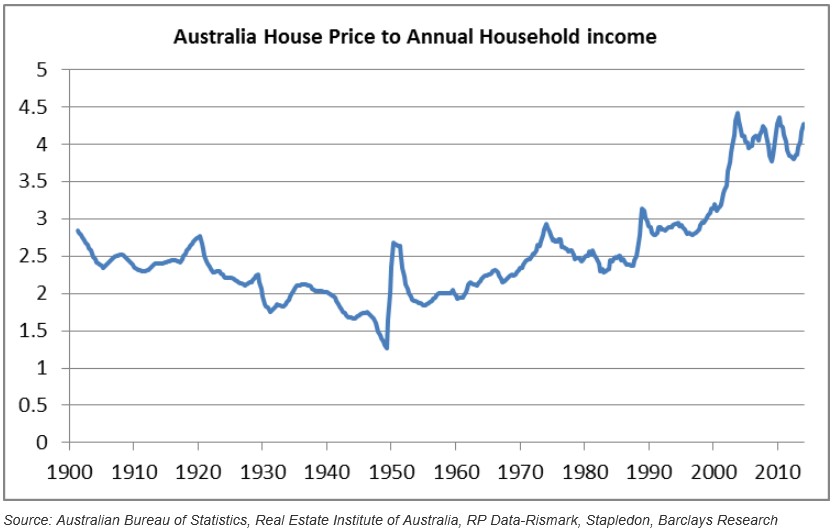

Today, houses cost over four times the average household’s yearly disposable income. At the beginning of the 1990s, this ratio was only about three times household incomes. As the chart over shows, this looks like the peak.

Finally, the report argues that for Australian home prices to significantly outpace inflation over the next ten years, as they have in the past, “would require a remarkable set of circumstances”, namely a combination of:

1. Continuing low or lower interest rates.

2. Willingness to live with more debt.

3. Household income being bolstered by greater participation in the income earning workforce.

4. Average wages growing faster than the CPI.

The last point is improbable seeing that wages and the CPI have a very stable relationship, while the other points are not very likely.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.