The inaugural Melbourne Economic Forum was held yesterday, which brought together a wide range of economists to discuss the Australian macroeconomic outlook and policy choices following the end of the mining boom.

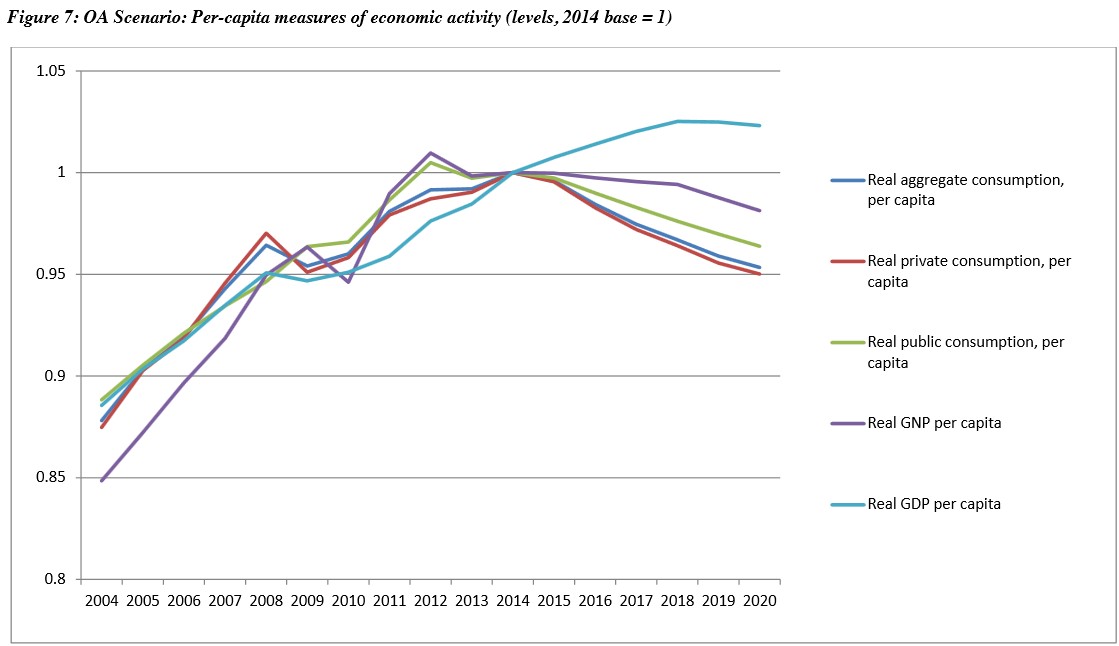

The discussion was centered around new modelling by the Centre of Policy Studies at Victoria University, which found that real per capita incomes and consumption will continue to slide for the rest of the decade and beyond as the fallout from falling commodity prices and the terms-of-trade takes hold, with real income per Australian forecast to be around 2% lower in 2020 than it is now:

The assumptions underpinning the modelling paper are as follows:

Key elements of our input assumptions, particularly as they relate to our forecast for per capita national income, are: a return of the terms of the trade to its 2005/06 level by 2019/20, a halving in mining investment from its peak 2012/13 level by 2019/20, a gap between the forecast annual growth rates for population and employment, and a high rate of foreign ownership of the mining sector.

But not all of our input assumptions are pessimistic. In forming a view on future multifactor productivity growth, we assume a continuation of the 0.3% p.a. rate of productivity growth experienced by the non-mining market sector over 2003/04 – 2012/13… Furthermore, in the labour market, our orderly adjustment scenario maintains the unemployment rate at its average 2013/14 level, via an assumption of sufficient wage flexibility to keep the unemployment rate unchanged over the forecast period.

And the results are summarised as follows:

With these assumptions in place under our orderly adjustment scenario, we forecast aggregate real GDP growth of approximately 2.1% p.a… leaving real GDP per capita rising by just under 0.4% p.a.. However, the forecast decline in the terms of trade, and the high level of foreign ownership of the rapidly expanding mining sector, together damp forecast real GNP growth relative to real GDP growth. With little growth forecast for real GDP per capita, this leaves our forecast for real GNP per capita negative, at approximately – 0.3% per annum. With forecasts for slow growth in public consumption spending and a rise in direct taxation, our forecast for annual average growth in per-capita real consumption spending is lower still, at -0.8%. With growth rates in these ranges, we forecast under our orderly scenario that important measures of economic welfare, such as the real wage, real GNP per capita, and real consumption per-capita, will return to the levels of the late-2000s by the end of the decade.

If anything, the modelling assumptions could prove to be too optimistic, heightening the risks that incomes and consumption spending could fall further than forecast.

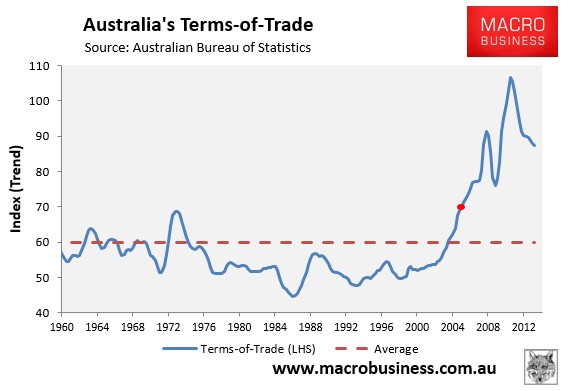

While the assumed return of the terms-of-trade to its 2005-06 level looks reasonable – denoted in the next chart by the red dot:

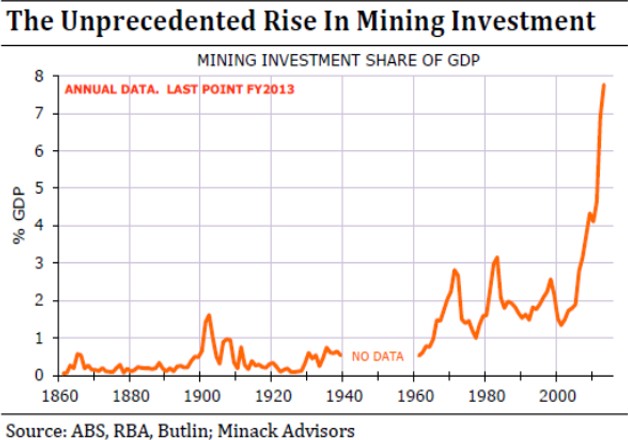

The suggestion that mining investment would only fall to around half of its 2012-13 peak – to around 4% – looks highly optimistic given this would still represent a level of mining investment that is more than twice the long-run average (see next chart).

If anything, there is the high likelihood that mining investment will overshoot on the downside to between 1% and 2% of GDP, dampening both employment and growth.

With this in mind, as well as the shuttering of the local car industry, the model’s assumption that the unemployment rate will hold at its average 2013-14 level also looks optimistic.

Overall, the modeling does a good job of highlighting the likely hit to living standards over the remainder of this decade; although there is a good chance that the situation could get worse as underlying drivers deteriorate more than expected.

Full report here.