The AFR’s Chris Joye posted a great article over the weekend explaining why he believes that Australian housing is now a bubble since values are between 20% and 30% above fair value:

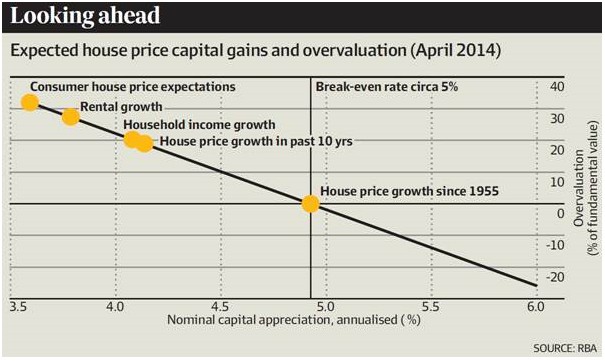

Australian homes are 19 per cent overvalued… if you compare the house price-to-income ratio to its average since 1993.

Other credible benchmarks on which to base future house price appreciation – including household income growth, the returns consumers think they will get and the rate at which rents rise – similarly imply that housing is overvalued by between 20 per cent and 30 per cent…

So what is a “bubble”? Simply put, it’s where prices materially exceed fair value. Speculative mania and/or rapid credit growth are only portents, not conditions, precedent to a bubble existing.

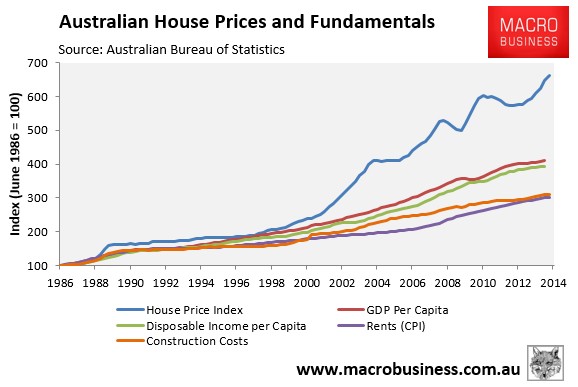

I obviously agree with Joye’s assessment. Based on any fair representation of fair value – e.g. incomes, GDP, rents, or construction costs – Australian housing long ago detached from their fundamental level (see next chart).

Advertisement

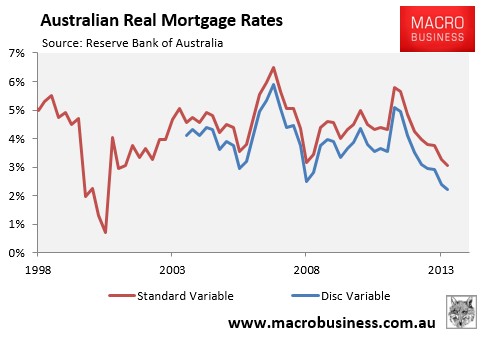

And while some of this overvaluation can be explained by lower real mortgage rates (see next chart).

Advertisement

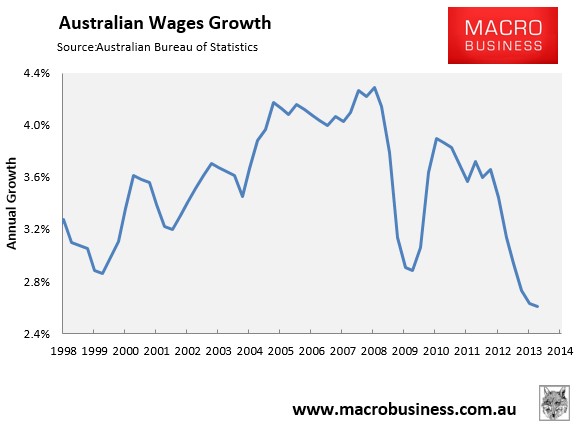

It is equally true that wages growth today is anaemic (negative in real terms), running at multi-decade lows (see next chart).

The fact that housing values in Australia have risen at around four times the pace of wages over the past year – on top of their already lofty valuations – is cause for serious concern and suggests that we are in the midst of a growing housing bubble.

Advertisement

Indeed, Australian housing valuations are likely to hit their highest level on record relative to both incomes and GDP later this year just as the economy embarks on its biggest adjustment since the early-1990s recession. Unemployment – already near 10 year highs – is destined to rise further over the next few years as large scale mining projects are completed and the Australian automotive industry shutters. Meanwhile, income growth is likely to continue to remain anaemic as the unwinding of the biggest commodity price boom in the nation’s history continues to drag on national incomes.

With Australian housing values rising briskly as the economy’s fundamentals deteriorate, the risk of correction sometime in the near future is arguably greater now than at any other time in living memory.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.