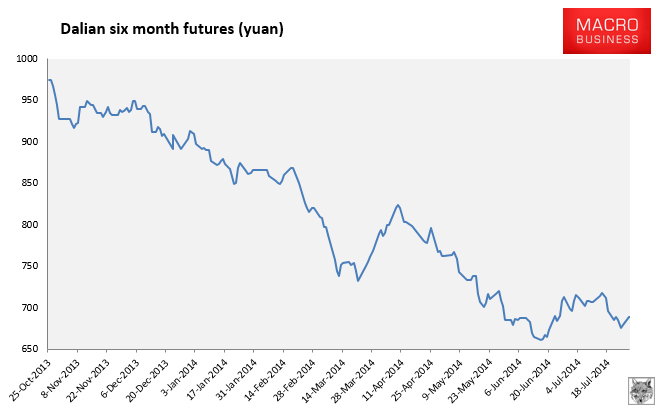

Singapore was closed yesterday so there is no spot or 12 month derivative prices. Dalian 6 month iron ore futures jumped 1.5% to 689 yuan:

The BDI cape fell a little more to near record lows and rebar futures didn’t do much. Stimulus hopes seem to be winning over fundamentals at the moment and there’s not much else one can say.

The often bullish Clyde Russell puts a brave face on things:

One thing has become clear from the latest production reports from the big three iron ore miners: They appear intent on ensuring their dominance by boosting low-cost output…The three global iron ore giants have effectively gambled that they can continue to boost production and grab bigger slices of global demand, given that they can withstand lower prices due to their low-cost mines and economies of scale.

So far it seems to be a winning strategy as they don’t appear to be battling to sell their output, and they are still likely to report strong profit growth as they reap the benefit of massive cost-cutting programmes over the previous two years.

The miners are apparently in a sweet spot. Staying there depends on iron ore prices not falling too much, which in turn is largely dependent on developments in China, buyer of about two-thirds of seaborne iron ore.

…The risk is that even a stronger economy won’t be able to soak up the flood of iron ore the global miners are producing.

BHP, Rio and Vale might be sitting pretty now, but the benefits of their cost-cutting won’t be repeated in future years, meaning their profit growth will be linked not just to volumes mined, but also to prices achieved.

Big risks there. Another Reuters piece talks it up too:

Exports from Iran – the world’s eighth-biggest supplier on the seaborne market – fell by a third in June from a year ago to just 1.2 million tonnes, according to Iranian industry data.

In Sweden, Northland Resources, whose long-term strategy was to develop its Kaunisvaara mine in Sweden to reach a yearly production rate of 4 million tonnes of iron ore concentrate, has been forced into a company-wide reorganisation.

Commissioning of a second processing line to produce a high-quality iron ore concentrate was placed on hold this month.

In Australia, the 1.7 million-tonnes-per-year Cairn Hill mine, started in 2010 when iron ore fetched twice today’s price, was shut after costs of $104 a tonne overran selling prices.

Around Australia other small miners once hoping to make inroads into the seaborne-traded market but now struggling include Pluton Resources, Sherwin Iron Ltd and Noble Group’s Frances Creek mine.

Kimberley Metals Group, an exporter of more than 150,000 tonnes a month to China, is cutting production by 25 percent at its Ridges mine in response to plunging ore prices.

Similarly, in Canada Labrador Iron Mines Holdings has come to a halt, warning it otherwise faced further losses.

Ever heard of those producers? Didn’t think so. That’s because so far this is very marginal production coming off.