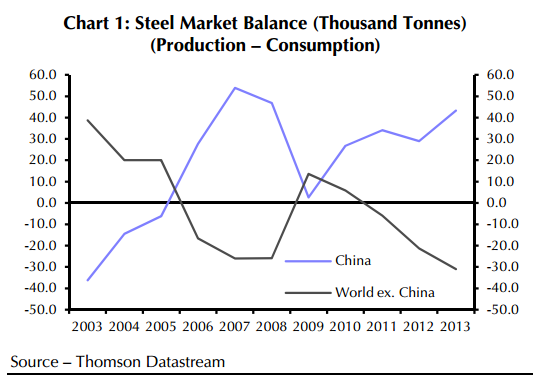

To pressures are coming to bear upon Chinese steel. The first is falling headline growth in China. The second is the changing composition of growth in China.

Capital Economics has a noted today on the first point and argues that surplus Chinese steel production is going to come under pressure in the second half of this year:

The struggle with profitability was thrown into relief this week by reports of a strike at the Xilin Iron & Steel Group, the largest (5m tonnes per year) private plant in Northeast China’s Heilongjiang province. Workers have not been paid for five months. Another privately-owned operation, Shanxi-based Haixin Iron and Steel Group, has suspended production and is expected to announce bankruptcy.

However, consolidation in the industry continues to be held back by local concerns over the negative impact of plant closures on tax revenues and employment.

All this is coming at a time of slowing Chinese demand growth. The CISA reported that consumption rose by a mere 0.1% y/y in January-May. There will be some support to demand from the government’s mini-stimulus spending on infrastructure, but the surplus in the market looks set to grow.

One option is for China to export its surplus steel…However, producers elsewhere, particularly in the US, are objecting to cheap Chinese imports and in June the US announced anti-dumping duties on Chinese high carbon steel wire.

In our view, the pressure for consolidation in China’s steel sector has risen and we expect lower output

growth in the second half of this year.

I could not agree more. Bloomberg has useful piece on the second pressure point, growth composition:

Advertisement

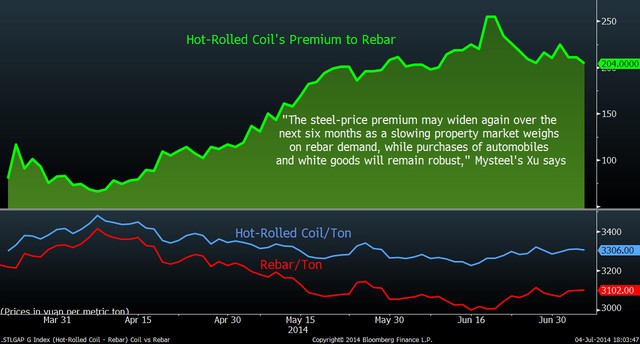

China’s demand growth for automotive steel sheets is trumping that for rebar, which is mainly used in construction, underscoring the nation’s efforts to “rebalance” its economy toward consumer spending.

The CHART OF THE DAY shows hot-rolled coil cost as much as 255 yuan ($41) more than rebar per metric ton last month, the widest spread since contracts for the automotive metal debuted on the Shanghai Futures Exchange in March. The gap almost quadrupled since early April. The lower panel tracks prices of the steel-product contracts, with coil at 3,306 yuan per ton, compared with 3,102 yuan for rebar.

What the article doesn’t tell you is that there is a shed load more rebar tonnage produced than there is hot-rolled sheets so output shrinks. And as mills go bust, more raw materials comes to market.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.