From Westpac’s Elliott Clarke comes a useful report analysing inflation and unemployment in the US, and its implications for Federal Reserve monetary policy:

Recently we delved into the CPI and PCE inflation detail to highlight that the recent uptick in inflation pressures looked to primarily be the result of transitory factors. The harsh winter weather caused stronger utilities inflation, which households felt directly (utility bills) and indirectly (food & accommodation services). And the US’ other major weather event (severe drought conditions on the West Coast and in Texas and Oklahoma) as well as a number of disease outbreaks also saw a noticeable jump in food price inflation.

Just as the FOMC saw through transitory disinflationary factors in 2013, arguably so too will they now look past current inflationary pressures. This is unless this stronger inflation leads to a successful attempt by workers to increase wages to compensate, giving higher inflation persistence and greater momentum. The degree of slack in the labour market is therefore critical to the outlook for inflation.

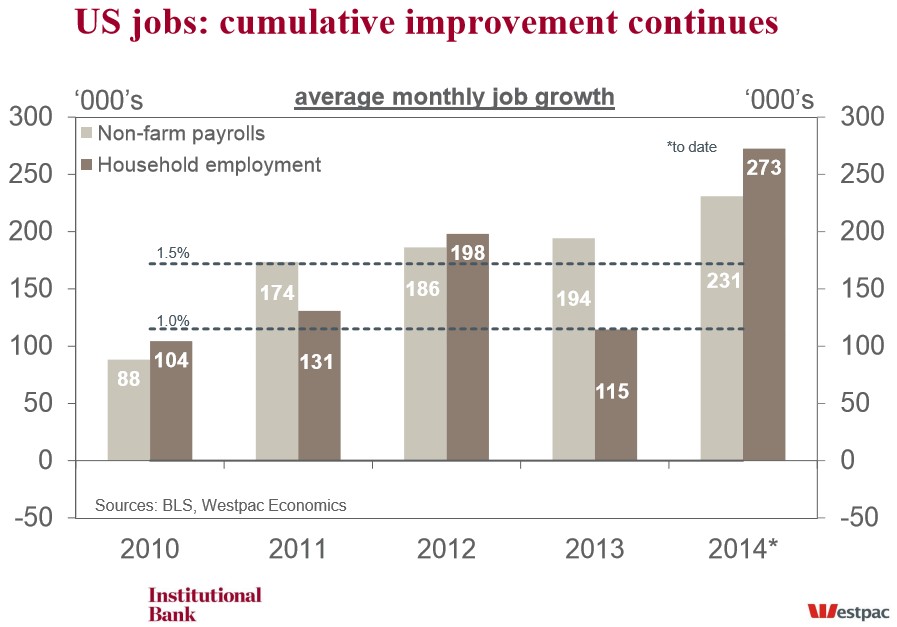

On many labour market metrics, one would be hard pressed to find evidence of slack. Nonfarm payrolls are averaging 231k in 2014 compared to 194k in 2013; that equates to a 2.0% annualised pace of employment growth, versus population growth of just 0.9%. For unemployment, the headline rate has now fallen to just 6.1%, with the unemployment rate for those unemployed for 14 weeks or less below its 20-year average.

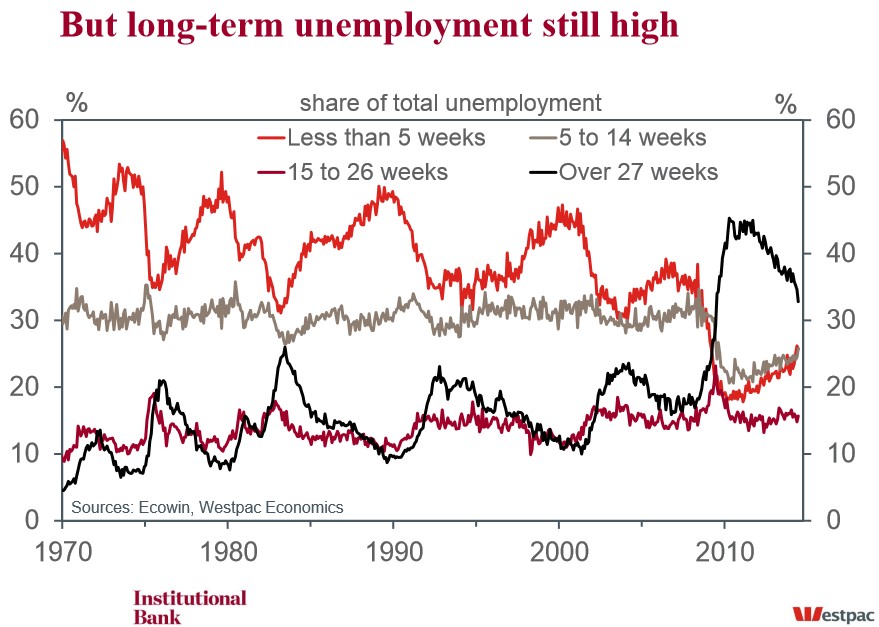

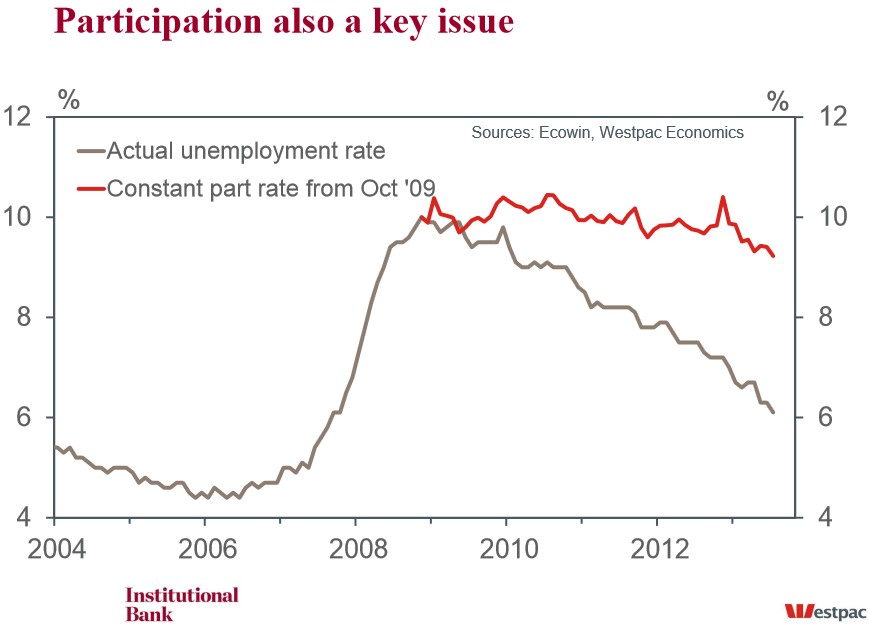

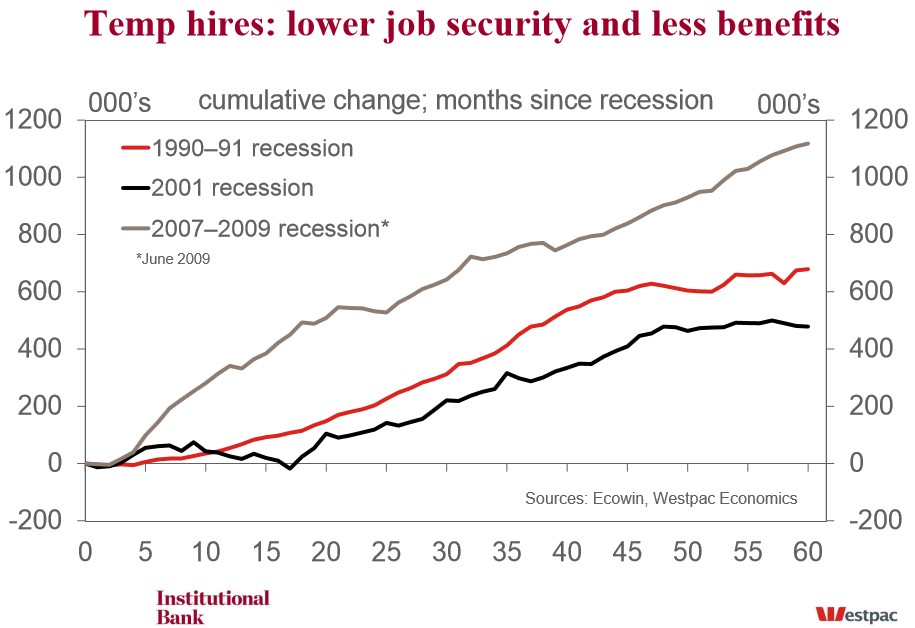

But these measures miss a number of critical nuances of the present situation which all still speak to substantial available slack. First, at 2.0%, long-term unemployment (27 weeks or more) remains twice as high as in the decade that proceeded the 2007–2009 recession. Second, of the long-term unemployed who subsequently find work, many must settle for temporary and/or part-time jobs, both of which remain elevated relative to history. Third, more often than not, the long-term unemployed give up looking for work regularly, leaving the labour force entirely. This has been a key factor behind the decline in the participation rate to near four-decade lows (and is certainly not restricted to older age groups).

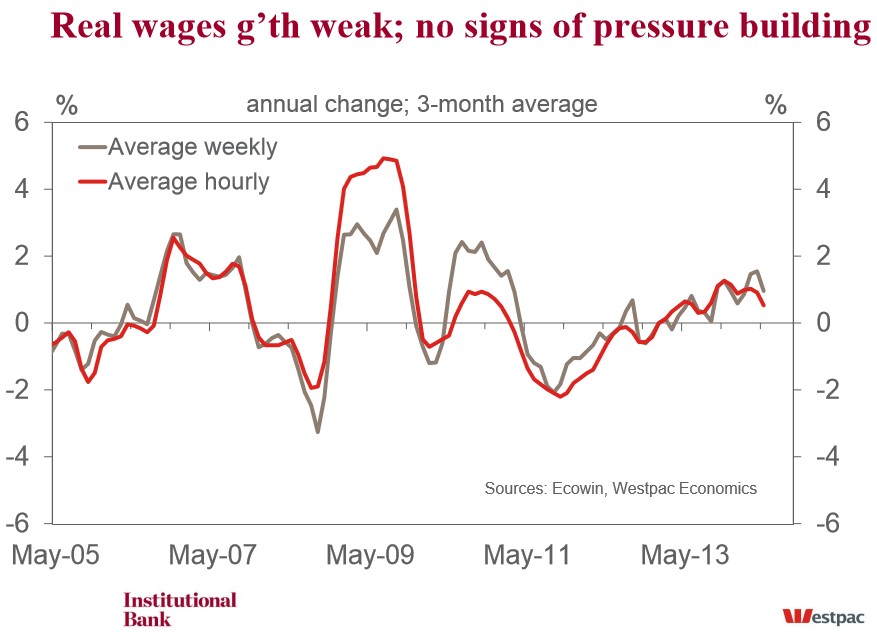

Together with the nominal rigidity of wages during the recession (employers being reluctant to reduce nominal pay rates; instead reducing the wage bill through headcount reduction), this labour market slack has kept wage inflation benign throughout the recovery. Indeed, as noted in the June FOMC minutes, in the year to May “hourly earnings for all employees increased around 2 percent”. Another measure of wages, the Employment Cost Index, only rose by 1.8% in the year to March. On both measures, real wages growth is negligable. A continuation of this trend is obviously not a threat to the Fed’s inflation mandate.

A critique of this expectation however is that, with short-term unemployment now so low, and given employment growth has strengthened, wage and inflation pressures are set to build. Implicit in this argument is that the long-term unemployed and those who have left the labour force are unlikely to return, restricting the supply of labour and stoking inflation pressures. The connection of these individuals to the labour market therefore matters a great deal. An often cited piece on this topic is Krueger et al (2014). Their analysis found that the long-term unemployed had become significantly detached following the GFC. Qualitatively, from 2008 to 2012, “only 11% of those who were long-term unemployed in a given month returned to steady, full-time employment a year later”.

However, not being able to find steady, full-time work does not necessarily mean that these individuals are lost to the workforce entirely. Indeed, if we look at the gross flow detail, we see that transition in and out of the labour market is becoming increasingly important to aggregate employment flows. The implication here is that there is a ready pool of workers available outside of those officially reported as unemployed. Unable to land jobs on strong enough terms to either remain permanently employed or qualify for another round of employment benefits (i.e. be counted as unemployed), their bargaining power is weak, putting downward pressure on wages.

From the FOMC’s central policy position (that, with activity and employment growth, inflation will return to target) it is clear that the FOMC remains optimistic on the impact of growth on labour force participation. That is, those on the fringes of the labour market could find their way back if cyclical conditions allow, adding to the productive capacity of the economy and restricting the inflationary consequences of a closing output gap. This position is backed up by research produced by Federal Reserve Board Economists. Analysing state and regional data, they found that not only were wages and inflation both historically impacted by short and long-term unemployment, but also that long-term unemployment and other measures of slack tend towards more normal rates as short-term unemployment falls.

It is clear that there remains a great deal of uncertainty over the outlook for labour market participation, not to mention the linkages between it and inflation. On this topic, a quote from Federal Reserve Governor Tarullo seems apt. In April, while discussing the “Long-Term Challenges for the American Economy” he noted that there was a need to remain vigilant on wages and inflation, but that “we should not rush to act pre-emptively in anticipation of such pressures based on arguments about the potential increase in structural employment”.

It is one thing to reduce liquidity accommodation through tapering as, abstracting from the potential impact on interest rates, it is neutral for policy. However, it is another thing entirely to begin to tighten policy through interest rates or balance sheet reduction. To do so before a threat to inflation became apparent would be contrary to the Fed’s maximum employment mandate, and potentially highly damaging to an economy still clearly struggling to return to normal. To us then, policy rate normalisation remains a long way off and will be a shallow and protracted affair, irrespective or where the unemployment rate may be.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.