Yesterday, I argued that commentators hailing this week’s stronger than expected March quarter GDP result needed a reality check, given that total expenditure in the economy (i.e. gross national expenditure or GNE) actually fell by a seasonally adjusted 0.3% in the March quarter, with annual growth clocking in at below 1% for the fifth consecutive quarter.

One flaw with this analysis – as is the case with most reporting of the national accounts – is that it did not adjust for Australia’s strongly growing population.

It is fair to say that a growing economic pie – as measured by GDP, GNE or some other measure – is not particularly relevant if everyone’s share of that pie actually shrinks due to population growth. Hence, per capita measures are a more accurate depiction of the economy’s underlying strength and are a truer reflection of the situation facing the average individual.

Accordingly, I have taken the time to deflate two measures of the domestic economy, as provided in the national accounts, by the ABS’ population data, in order to ascertain the underlying strength of the economy in per capita terms.

The two measures chosen are:

- Gross national expenditure (GNE), which is “the total expenditure within a given period by Australian residents on final goods and services (i.e. excluding goods and services used up during the period in the process of production). It is equivalent to gross domestic product plus imports of goods and services less exports of goods and services”.

- Domestic final demand (DFD), which is the sum of “government final consumption expenditure, household final consumption expenditure, private gross fixed capital formation and the gross fixed capital formation of public corporations and general government”.

As you can see, both measures exclude the growth impact from rising export volumes.

So what do these measures show when measured on a per capita basis?

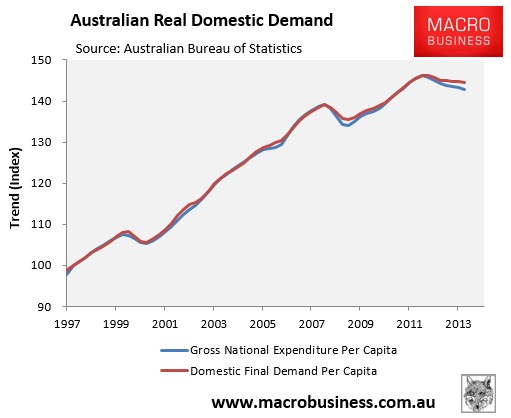

First, after rising solidly in the three years to September 2012, both GNE and DFD have been falling:

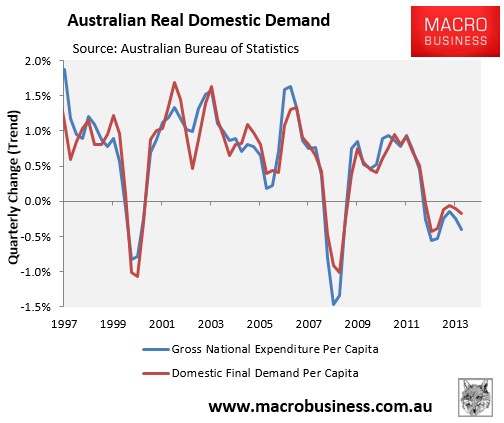

Moreover, both measures have fallen for two consecutive quarters and have been negative since September 2012:

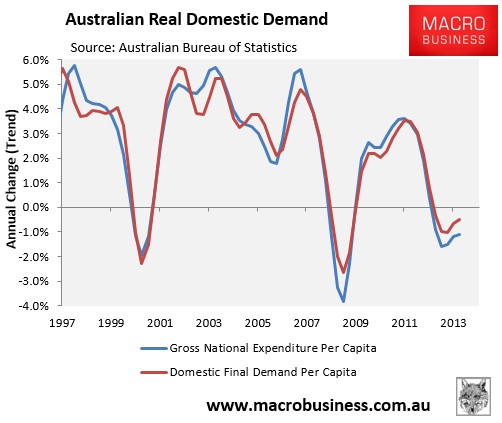

Finally, while annual growth in both measures has improved marginally over the past two quarters, it has remained negative since March 2013 and remains well below the 2.3% per capita average growth recorded under both measures in the decade to March 2014:

As noted yesterday, the big expansion in export volumes is a welcome development. However, it does hide the fact that the domestic economy remains weak, propped-up by strong immigration. And according to these measures, the domestic economy could even be experiencing a recession in per capita terms.

Further, given the big post-Budget fall in consumer sentiment, the potential slowing of the housing market (i.e. slowing price growth, approvals, and lower auction clearances), and the expected accelerated falls in mining investment, stiff headwinds are likely to continue, weighing on both incomes and jobs.

Hence, the euphoria over Wednesday’s strong headline GDP result, on the back of rising export volumes, needs a reality check.