by Chris Becker

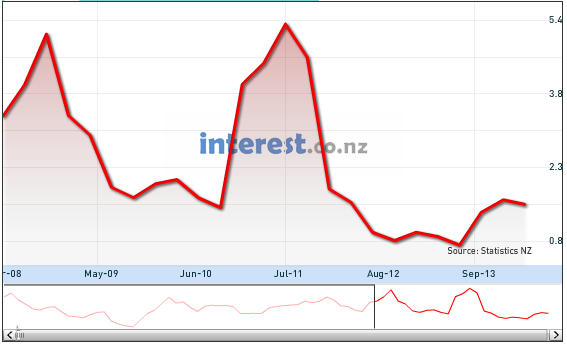

As reported earlier in Macro Morning, the Reserve Bank of New Zealand (RBNZ) has hiked its official cash rate 0.25% to 3.25%:

The main reasons indicated are house price inflation and very decent GDP prints (mainly due to reconstruction in Christchurch, not necessarily an indicator of a strong underlying economy)

Sound familiar?

Although inflation doesn’t seem to warrant that much concern – from interest.co.nz:

“Nevertheless, overall wage inflation remains moderate, reflecting recent low headline inflation, increased labour force participation and strong net immigration,” he said.

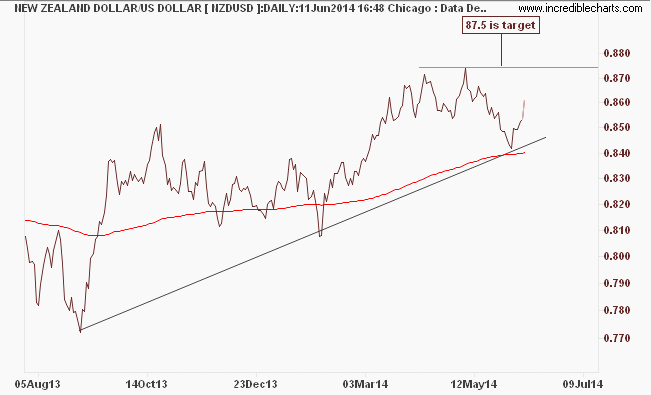

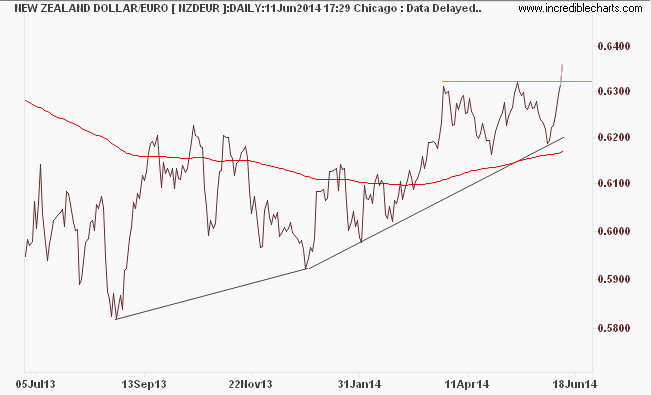

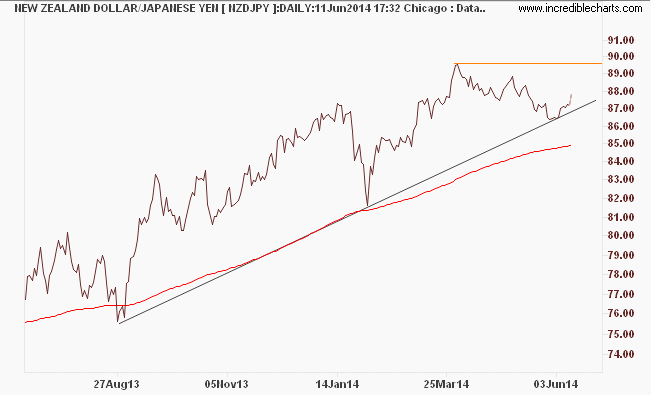

At least the RBNZ is trying – in vain – to jawbone its currency down – from Governor Graeme Wheeler:

The exchange rate has not yet adjusted to weakening commodity prices, but is expected to do so. The Bank does not believe the exchange rate is sustainable at current levels.

Sustainable for long only Kiwi carry traders, definitely:

And looks like more rate hikes on the way:

“Inflationary pressures are expected to increase. In this environment, it is important that inflation expectations remain contained and that interest rates return to a more neutral level.”

Wheeler repeated previous comments that the OCR needed to rise and its future rises would depend “on future economic and financial data, and its implications for inflationary pressures. ”

“By increasing the OCR as needed to keep future average inflation near the 2 percent target mid-point, the Bank is seeking to ensure that the economic expansion can be sustained,” Wheeler said.

Well done the RBNZ in trying to contain house price inflation, and it seems its attempts at macroprudential controls have had some success (and patently ignored by the RBA), but waging a currency war with effectively no army is a losing battle.

The statement in full:

The Reserve Bank today increased the Official Cash Rate (OCR) by 25 basis points to 3.25 percent. New Zealand’s economic expansion has considerable momentum, with GDP estimated to have grown by around 4 percent in the year to June. Global financial conditions remain very accommodative and are reflected in low long-term interest rates and narrow risk spreads.

Economic growth among New Zealand’s trading partners is gradually improving and global inflation remains low. Prices for New Zealand’s export commodities remain historically high, but their recent falls will reduce farm incomes over the coming year.

A continued acceleration in construction in Canterbury, and more broadly, is supporting growth, together with strong net immigration flows that are adding to housing and household demand. Business and consumer confidence remains buoyant, as do businesses’ reported intentions to invest and to hire.

While house price inflation remains high, the housing market has moderated since late last year when restrictions were applied to high loan-to-value ratio mortgage lending and when mortgage interest rates began rising. Fiscal consolidation continues to moderate demand growth, though by less than previously assumed.

The exchange rate has not yet adjusted to weakening commodity prices, but is expected to do so. The Bank does not believe the exchange rate is sustainable at current levels. Headline inflation remains moderate and tradables inflation is expected to be low for some time.

However, above-trend growth has been absorbing spare capacity and adding pressure to non-tradables inflation. These pressures are particularly evident in construction cost increases. Nevertheless, overall wage inflation remains moderate, reflecting recent low headline inflation, increased labour force participation and strong net immigration.

Inflationary pressures are expected to increase. In this environment, it is important that inflation expectations remain contained and that interest rates return to a more neutral level. The speed and extent to which the OCR will need to rise will depend on future economic and financial data, and its implications for inflationary pressures.

By increasing the OCR as needed to keep future average inflation near the 2 percent target mid-point, the Bank is seeking to ensure that the economic expansion can be sustained.