by Chris Becker

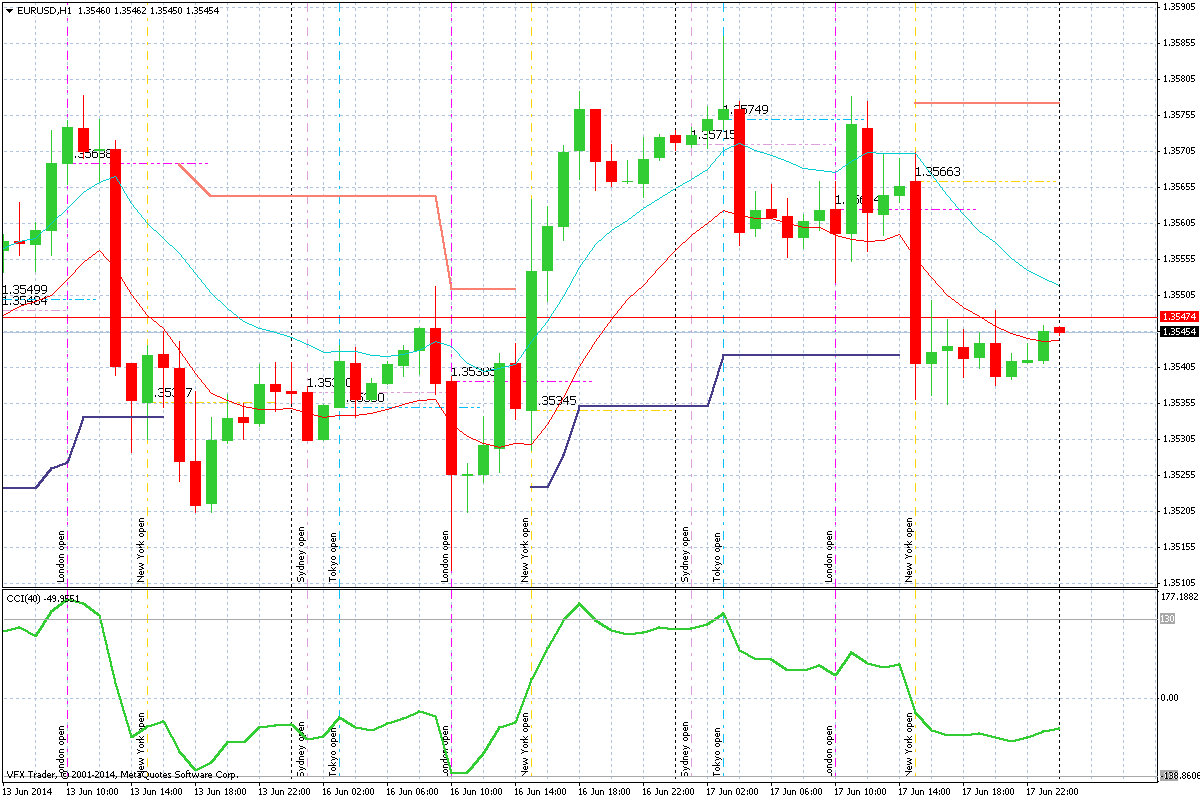

An extremely event driven night on world markets which started after the Asian session closed with a series of European based releases – British CPI and German/EZ sentiment surveys – first played havoc on European stocks, pound sterling and the Euro, the latter reinforced by USD strength coming into the NY open as their CPI results filtered through:

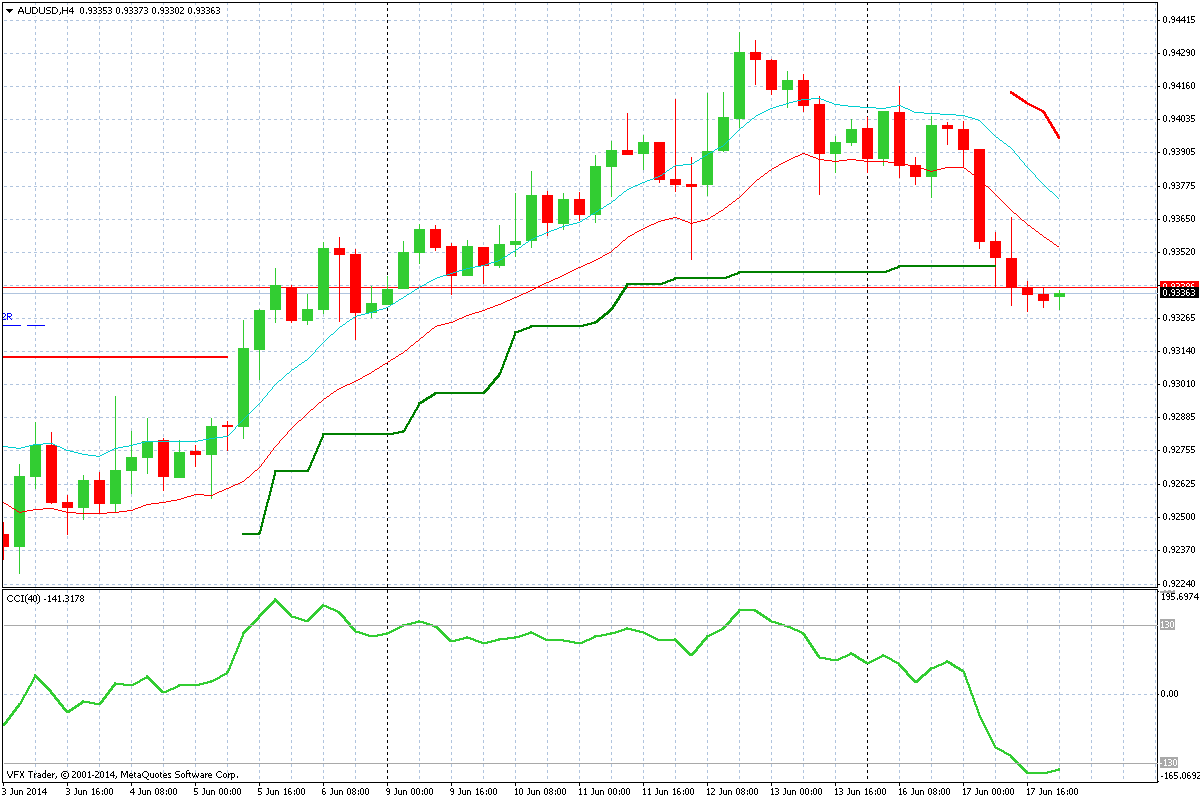

Aussie dollar continued its downfall with longs suckered in at the London open as traders reacted to yesterdays dovish RBA minutes and then further smacked on the NY open as USD surged. Looking at the 4 hourly chart though, I sense a deceleration in selling on oversold conditions, but this could easily trip itself and fall below the 93 handle:

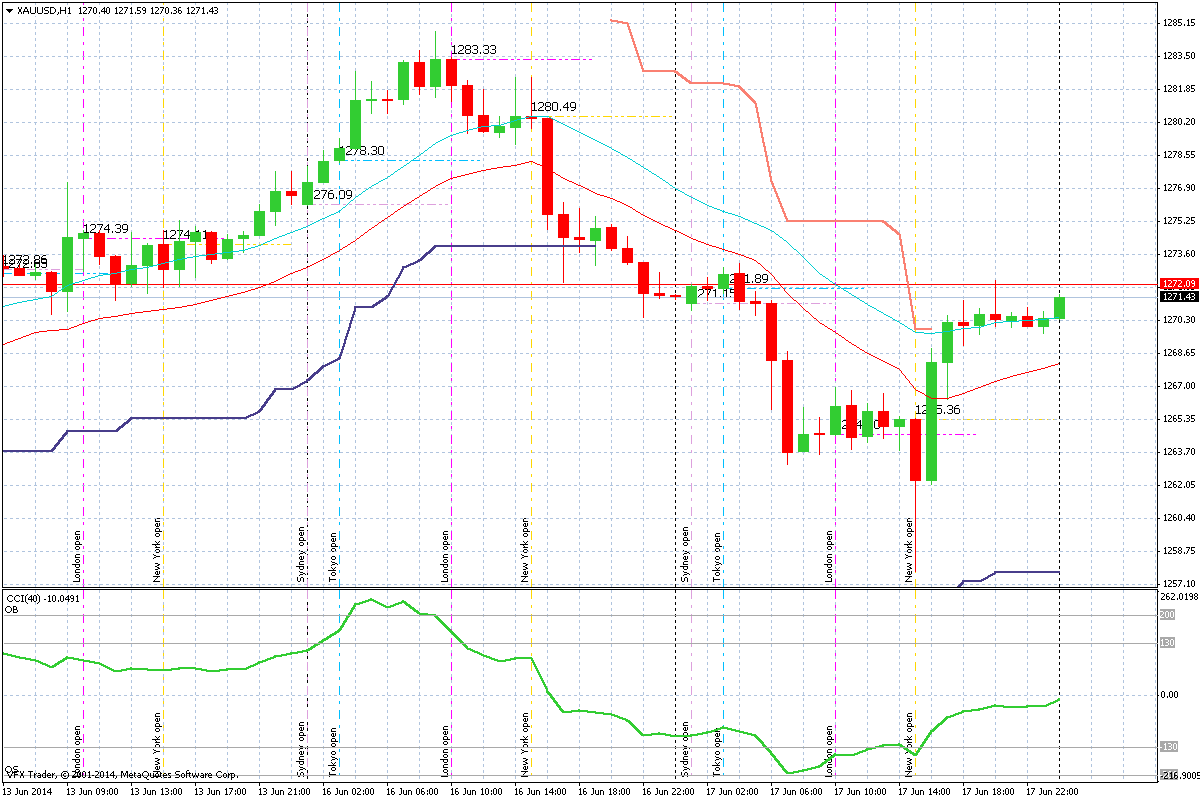

There was an interesting divergence in precious metals – silver (XAGUSD) held up on the hourlies while gold tripped and followed the AUD demise until extremely heavily bid on the US CPI result – however it ended the last 24 hours were it started:

Can you see why I love trading gold? On any timeframe (weekly to 1 minute) it offers opportunities – just watch the spread.

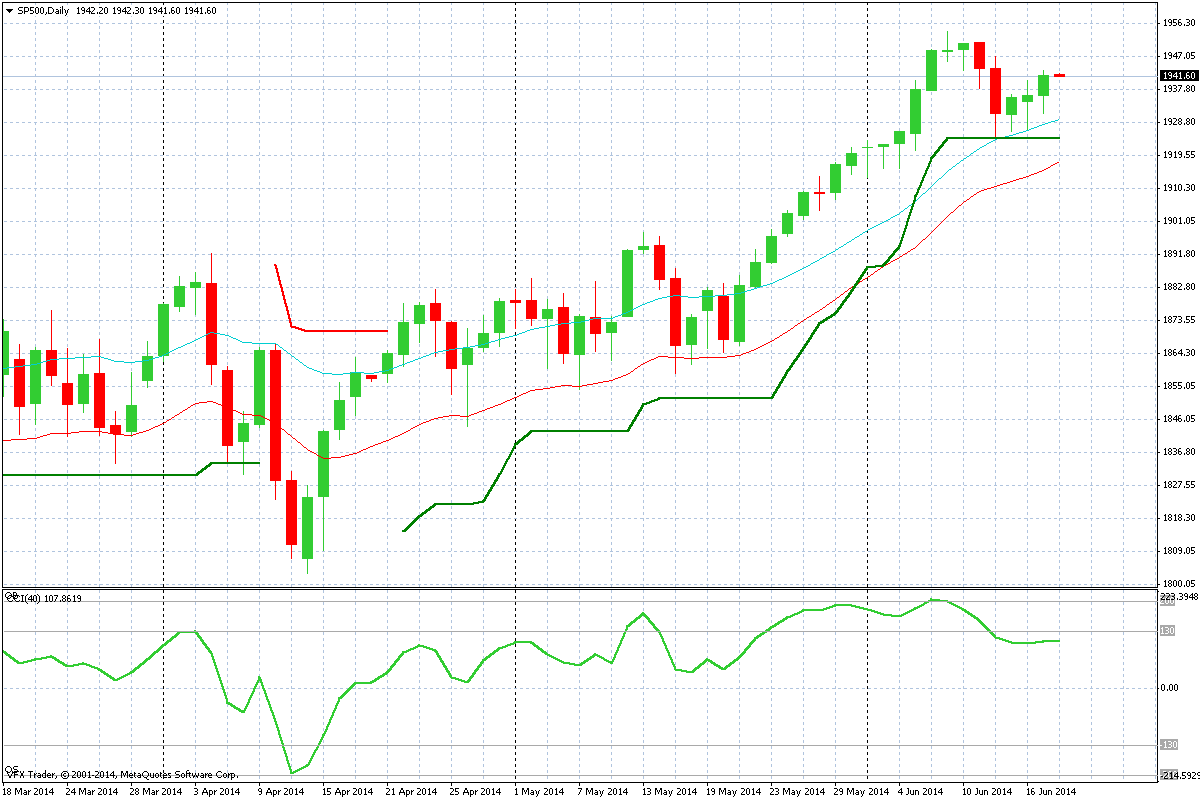

US stocks finished up after a whipsaw ride around the European and US economic releases, as “buy the dip” continues for the S&P500 at least on daily charts:

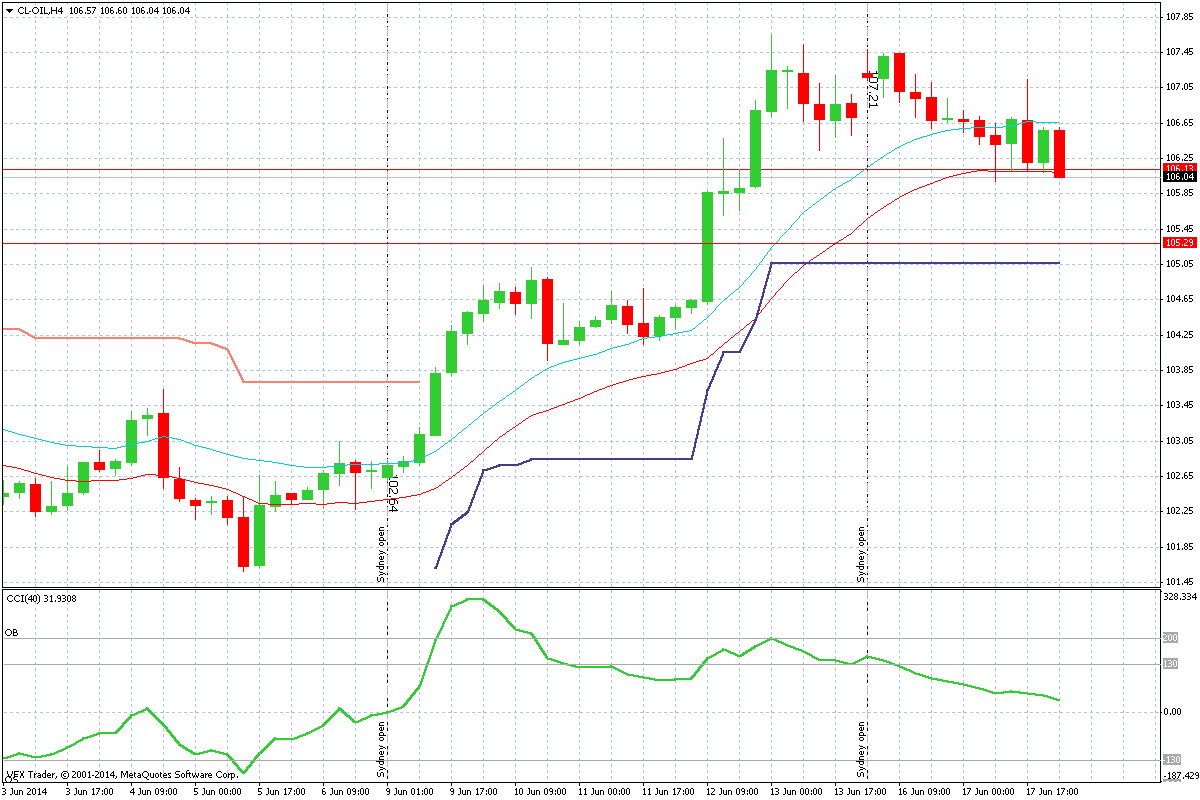

Oil continued to slide as chaos rained through the Middle East (when doesn’t it) and Ukraine but it seems the speculative flavor of oil is waning as potential other macro factors weigh – solid gas reserves in Europe, higher US oil production (and higher prices at the pump coming in the US)

I’m watching a fairly bearish engulfing candle on the hourly charts of the WTI futures, which sets up for a second short swing on the 4 hourly as the moving averages roll over on capitulation, but strong support at 105 barrel mark could see a bounce again soon:

Its going to be a busy morning here in Asia – reacting to overnight and absorbing quite a solid front of semi-important economic releases.

Here’s a summary of what we will watch closely at MB:

- 8:45 am NZ Current Account Balance

- 9:50 am Bank of Japan Minutes, Trade Balance

- 10:00 am Conference Board Leading Index

- 10:30 am Westpac Leading Index

- 11:30 am China May property prices