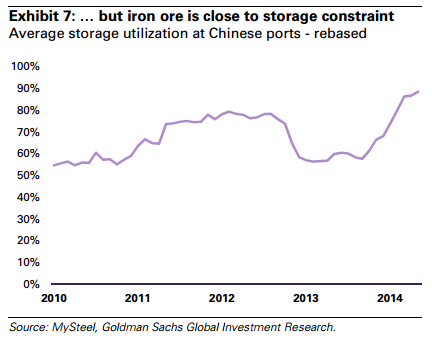

Stockyards in Chinese terminals have provided a useful buffer to absorb excess seaborne iron during the early stages of structural oversupply; inventories have increased by 39Mt since October 2013. With iron ore port stocks at record levels, could stockpiles be near saturation? Based on a sample of 15 large bulk terminals, our analysis suggests that Chinese port stocks are currently using 89% of available storage capacity. On that basis, Chinese port stocks could be c.14Mt away from hitting a physical constraint on storage space. This would imply that further port restocking can only absorb a limited amount of additional ore, and Chinese ports will no longer act as a safety valve in an oversupplied market. In other words, the ability to cushion the impact of structural oversupply via inventory build-up is now quite limited, so marginal producers are now fully exposed to the structural oversupply in the market. Our 2015 price forecast remains unchanged at US$80/t.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.